Among other things, he promoted stock-flow consistent modeling. He had a bookReconstructing Macroeconomics.

I hold dear the review of Lance Taylor of Wynne Godley’s work, titled: A Foxy Hedgehog: Wynne Godley And Macroeconomic Modelling.

The article starts:

The fox knows many things, but the hedgehog knows one big thing (Archilochus, seventh century BCE).

Lance Taylor clearly understood the importance of accounting. In the paperA Simple Model Of Three Economies With Two Currencies, Wynne Godley and Marc Lavoie quote him:

As pointed out by Taylor (2004, p. 206), ‘the best way to attack a problem in economics is to make sure the accounting is right’.

…

Bibliography

…

Taylor, L. 2004. Exchange rate interderminacy in portfolio balance, Mundell–Fleming and uncovered interest rate parity models, Cambridge Journal of Economics, vol. 28, no. 2, 205–27

You may have noticed the expression (G + X)∕(θ + μ), where G is government expenditure, X is exports, θ is the tax rate, and μ is the propensity to import in stock-flow consistent (SFC) models.

In the bookA Biographical Dictionary of Dissenting Economists, Wynne Godley (pages 232-240) says:

… As a result of this apprenticeship at the ‘sharp end’ of economic policymaking, I had formed by the late 1960s a system of views about how the economy works which corresponded roughly to what people now call ‘crude’ Keynesianism. That is, I thought real output and employment were determined by the exogenous variables of the model – government expenditure and exports – interacting sequentially through the combined effects of the multiplier and accelerator, while inflation was a largely contingent process (which, as stated by the OED, ‘may or may not happen’) only weakly related to the pressure of demand (1974a). But I recognized early on that performance in foreign trade was an abiding constraint on growth. In no sense did this set of views make me into a ‘dissenting’ economist. The same opinions were held by virtually all my colleagues in the Civil Service and, so far as I could discern, in comparable institutions in foreign countries. I had, for instance, no sense of any difference in Weltanschauung when discussing any aspect of economics with Arthur Okun.

(The entry seems to have been first published in the year 2000).

I thought if you’re writing on economics, you should say that frequently and especially when you’re introducing the subject to someone.

That the worldview was widely held seems surprising to me though.

In mainstream economics, the Mundell-Fleming model is central. It’s however wrong to the core!

As early as 1978, Wynne Godley in a paper“New Cambridge” Macroeconomics And Global Monetarism: Some Issues In The Conduct Of U.K. Economic Policy (with Martin Fetherston) had a model with the compensation thesis which is contrary to the neoclassical model. As per Marc Lavoie’s paperWynne Godley’s Monetary Circuit, where he also refers to the paper, according to the compensation thesis:

central banks set a target interest rate and supply bank reserves and cash on demand. Thus, if there is an increase in the amount of foreign reserves held by the central bank on the asset side of its balance sheet, so as to keep the overnight interbank rate on target this will be compensated on the asset side of the balance sheet of the central bank by either a decrease in the size of the advances provided to domestic banks or a decrease in the amount of government securities held by the central bank. As a third possible compensatory mechanism, the central bank may instead issue central bank bills on its liability side.

Marc Lavoie and Wynne Godley, Levy Institute, 2002. Picture via Marc Lavoie’s site.

There’s an interesting review of Jagdish Bhagwati’s book Protectionism published in the year 1988 by Wynne Godley in the journal Economica, year 1993. Without going into the review, I wanted to highlight how Wynne Godley’s views were quite similar to Nicholas Kaldor’s and Godley proposals such as planned trade and international cooperation of a new kind:

… Kaldor’s chapter, ‘The Foundations of Free Trade Theory and Their Implications for the Current World Recession’ (in E. Malinvaud and J. P. Fitoussi (eds.), Unemployment in Western Countries, 1980), which, in the context of a fundamental critique of the abstract theory of international trade, suggests that, because of the scope for dynamic economies of scale, free trade in manufactured goods leads to the concentration of manufacturing production in certain areas, what Kaldor called ‘a polarisation process’. ‘In principle such trade is of great practical benefit since specialisation between industries of different areas should enable the benefits of the economies of scale to be realised more fully. However … this … depends on the trade being balanced in both directions … But as past experience … has shown this does not come about naturally.’

These ideas were further developed in Kaldor’s 1981 article in Economie Appliquee, ‘The Role of Increasing Returns, Technical Progress and Cumulative Causation in the Theory of International Trade and Economic Growth’, where he related his concern about dynamic imbalances in trade to the ideas of Roy Harrod (himself a strong advocate of protection as a way of improving Britain’s economic performance throughout the postwar period), who had put forward the theory of the foreign trade multiplier in his International Economics (1933). As the trade imbalances constituted a growing threat to the continued expansion of the world economy, Kaldor concluded that we should not ‘stick to free trade (whatever the cost) but introduce a system of planned trade between the industrially developed countries on a multilateral basis’.

Also in an interview to the magazine Marxism Today in 1981, Wynne Godley says how he is openly opposed to free trade and the destructive aspect of it:

Let’s turn to some international questions. How do the problems of the UK economy — and your solutions to them — tie in with problems in the world economy?

Well, the general answer is that I don’t think that free trade is the best way of organising international trade. The classical theory of international trade, which appears in text books and which is extremely influential in peoples’ minds, is based on a postulate of full employment. If you assume full employment you can easily prove that free trade is mutually advantageous. But if you think, as I do, that full employment cannot be assumed, then it’s easy to make out a realistic case that free trade is extremely destructive to economies that are relatively unsuccessful. Instead of making them more prosperous and better-off, it destroys them. I think this is a general proposition; it applies to the United Kingdom at the moment because it’s a relatively unsuccessful country, and I think it is beginning to apply to the United States, which is also becoming a relatively unsuccessful country.

When you say that you think that the free trade system is a bad system, how do you think it should be changed? It’s easy enough to say Britain should have import controls, but how do you see this in international terms?

Well, the logical answer to the question which, as an academic, is what I am primarily called on to give, is quite clear to me. If all relatively unsuccessful countries protect in the way we suggest — using import controls to raise domestic output and not to strengthen their balance of payments — the system of protection can be generalised advantageously. But that assumes a high degree of international co-operation, and international co-operation of a new kind.

The fourth Godley-Tobin lecture was by Marc Lavoie on February 2021. The video of the talk is on YouTube.

There is now a paper by the same title published with ROKE (Review Of Keynesian Economics).

It’s interesting how James Tobin had a lot of things right but yet his model has a lot of neoclassical economics.

In the paper Marc Lavoie argues how Tobin seems to get a lot of things right but those were just weapons for criticisms of extreme views such as of Friedman. Tobin didn’t actually believe in them. Wynne Godley’s models are quite successful in escaping old ideas, if you remember the ending line of the preface of the GT.

I was rereading the articleKeynes And The Management Of Real National Income And Expenditure by Wynne Godley from 1983 (page 157 in that book, footnote 20) and he reminds us of this letter from JMK published in The Collected Writings Of John Maynard Keynes, Volume XXVI, pages 287-289, that he thought that import controls work much better than movements in the exchange rates.

To J. M. FLEMING, 13 March 1944

Dear Fleming,

Your paper on quotas versus depreciation, sent me with your letter of February 14th, raises a very interesting question. But, for my own part, I am not one of the’ most economists’, to whom in paragraph 2 you attribute the view that disequilibrium ought, so far as possible, to be corrected by movements in the rate of exchange rather than by controls over commodity trade.

There is, first of all, to the contrary the simple-minded argument that, after all, restriction of imports does do the trick, whereas movements in the rate of exchange do not necessarily do so.

Senate Poised To Pass Huge Industrial Policy Bill To Counter China is the headline of a recent news item from The New York Times.

US politicians have come to realise—especially after the rise of Trump—that free trade and globalisation is a major cause of damage to the US economy. The purpose of industrial policy is to make US producers more competitive. This results in increase of exports and fall in imports, relative to gdp.

Wynne Godley had been warning for quite some time on how the US government should address the trade imbalance instead of leaving it to market forces. In March 2003, in an articleThe U.S. Economy: A Changing Strategic Predicament he said:

The default conclusion is that the U.S. economy will not recover properly in the medium term, but rather will enter a prolonged period of “growth recession.” The only lasting solution will be to get U.S. exports to rise much faster than imports over a prolonged period.

And also suggested non-selected protectionism for the short term.

Another recent news article from NYT is about a global tax coordination. Globalisation has led to a race to the bottom. To raise price competitiveness, countries have been wrongly incentivised to reduce tax rates on firms and this led to some competition between countries to keep reducing tax rates on corporations. And this has led to lot of economic damage.

The Democratic Party of the US has learned from mistakes in the past and is trying to correct them but the Dems are total corporatists and these measures are just for elite preservation. For example, they were talking of reversing Trump’s tax cuts for corporations but the party is a champion in performative politics: it seems they’re not reversing it now.

As Joseph Stiglitz points out, the problem with this 15% tax rate is that it become the de facto the maximum tax rate.

In his last paper, Wynne Godley said on rebalancing:

It is inconceivable that such a large rebalancing could occur without a drastic change in the institutions responsible for running the world economy—a change that would involve placing far less than total reliance on market forces.

Although the steps taken by the US government looks in the right direction, there’s still a large way to go, especially considering how the Democrats pretend to do all sorts of good things. Still far from a Keynes like plan to fine surplus countries and to remove imbalances in balance of payments and international investment position.

There was a conference on the 10th death anniversary of Wynne Godley last year. If you haven’t seen it, the video recordings/presentation/remarks are in that link.

Now, there’s a special issue by the JPKE about the conference with papers as in the cover:

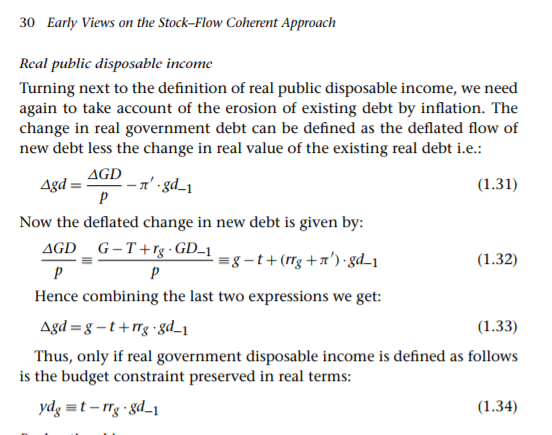

A good macroeconomic model would use national accounts and the flow of funds with behavioural hypotheses. It’s complicated by the fact that prices of goods and services change. It’s not just that if prices of goods and services change, you’re consumption would change in response to that, but also because say the deposits you hold in the bank is worth less.

So your behavioural equations need to be modified. It’s not easy. Wynne Godley recalls in his book Monetary Economics:

And no lesser authority than Richard Stone (1973) made the same mistake because in his definition of real income he did not deduct the erosion, due to inflation, of the real value of household wealth.

…

References

…

Stone, R. (1973) ‘Personal spending and saving in post war Britain’ in H.C. Bos, H. Linneman and P. de Wolff (eds), Economic Structure and Development: Essays in Honour of Jan Tinbergen (Amsterdam: North Holland), pp. 75–98.

The system of national accounts does recognise the importance of this but there aren’t any real variables defined. Real as opposed to nominal. Instead holding gains (formal phrase for “capital gains”) is divided into two parts: real holding gains and neutral holding gains. So,

Assets prices can rise differently than prices of goods and services. Para 12.89 says:

The real holding gain on an asset is defined as the difference between the nominal and the neutral holding gain on that asset. The values of the real holding gains on assets thus depend on the movements of their prices over the period in question, relative to movements of other prices, on average, as measured by the general price index. An increase in the relative price of an asset leads to a positive real holding gain and a decrease in the relative price of an asset leads to a negative real gain, whether the general price level is rising, falling or stationary.

Of course we should consider holding gains and losses on liabilities as well.

This is anyway complicated practically. I haven’t yet seen national accounts of any country producing such tables. But the SNA—including the 2008 SNA—doesn’t have any framework beyond this. This is because it considers that economic behaviour would be different for real holding gains or losses, as opposed to just the flow aspect.

In other words, if your (nominal) income is $100 and there’s a 10% inflation, your consumption would fall. But you might not react the same if you have a real holding loss of $10.

But to a first approximation you could simplify and bring real holding gains into real income. I have simplified quite a bit and these are quite challenging things, so I refer you to Wynne Godley and Marc Lavoie’s (G&L)’s book Monetary Economics.

I wrote this post after an online discussion about the government “inflating away the nominal debt”. Although such claims are loaded, there is some logic to it. In inflation accounting, holding gains/losses appear in incomes. Modeling involves going back and forth between real and nominal variables.

An original writing is that of Wynne Godley (and Ken Coutts and Graham Gudgin)—a 1985 paper titled Inflation Accounting Of Whole Economic Systems. In that you see the equation:

So the government disposable income (in addition to taxes and central bank profits, also has the holding losses due to the fact that prices of goods and services has increased in the period, not just because of changes in prices of government bonds).

Of course, there’s also the loadedness of the phrase “inflating away the debt”. That’s a different matter, my point here is to address the intuition of why inflation can be thought of as bringing revenue to the government and reducing its debt.