Wynne Godley wrote an article in the London Review of Books in 1992 commenting on how and why the idea of a European Monetary Union is doomed to fail. LRB today removed the “paywall” so that the article is accessible to everyone.

If you read my posts or look at the “Tag Cloud” on the right, you will recognize what a big fan of Wynne Godley I am :-).

Above is an Observer article from 1991. Click the newspaper clip to enlarge.

Quoting from the end of the article:

If we are to proceed creatively towards EMU, it is essential to break out of the vicious circle of ‘negative integration’— the process by which power is progressively removed from individual governments without there being any positive, organic, all-European alternative to transcend it. The nightmare is that the whole country, not just the countryside becomes at best a prairie, at worst a derelict area.

The International Monetary Fund, IMF has one full chapter devoted to the subject of “twin deficits” in their latest issue of World Economic Outlook. The subject of “twin deficits” is full of complications and can invoke the deepest emotions from economists. Naively, the argument goes as follows: The “three financial balances” identity can be written as

NAFA = DEF + BP

where NAFA, DEF and BP stand for the Net Acquisition of Financial Assets of the private sector, Government Deficit, and the current Balance of International Payments. From the above, if the government deficit increases, for a constant NAFA (rather a constant NAFA/GDP), an increase in DEF causes BP to reduce, i.e., reduces the current account balance or causes the current account deficit to increase.

Now, this is hardly the best way to put it – because it is mistaking an accounting identity for a behavioural relationship. For example, in conjecturing, one is implicitly assuming that the budget deficit is exogenous or fixed by the government. It is then argued that to reduce the current account deficit (or BP with a minus sign), the government should cut its budget deficit.

There is some truth to “twin deficits”, in my opinion. A lot actually! However, conclusions from any analysis need to be studied in a proper framework and stock-flow coherent macroeconomics is the only way to do this. Money is automatically endogenous in “SFC” models – it cannot be otherwise.

The government sets its fiscal policy or fiscal stance. This can be approximated to be G/θ, where G is for government expenditures and θ is the tax rate (as opposed to total taxes). The budget deficit is out of the control of the government and is dependent among other things, the private sector propensity to consume, the exports and imports. Assuming exports remain constant, relaxing the fiscal stance (i.e., an increase of G/θ) leads to an increase in domestic demand, ceteris paribus. An increase in demand leads to an increase in imports. (If people have higher incomes, they will purchase more imported products). This leads to the widening of the current account deficit and hence through the sectoral balances identity a widening of the budget deficit.

Various things can be said about what is written in the last paragraph. Take the case when ceteris is not paribus. An increase in the propensity to save (i.e., a decrease in propensity to consume) can lead to a higher NAFA and DEF and increasing BP (as a result of lower domestic demand and hence lower imports).

Come back to ceteris paribus: assume that demand abroad has increased for some reason. This could be due to an increase in the fiscal stance of the foreign government or a private sector led credit expansion abroad. This will lead to an increase in exports for the country we are discussing. So in such a scenario, an increase in the fiscal stance – up to some limit – will not lead to a widening of CAD, i.e., decrease in BP.

Wynne Godley put it best in a Levy article in 1995 (always perfect with his wording):

Refuting the “Saving is Too Low” Argument

It is sometimes held that, in the words of the Economist (May 27. 1995, p. 18), “America’s current account deficit is enormous because its citizens save so little and its government spends too much.” The basis for this proposition is the accounting identity that says that the private sector’s surplus of saving over investment is always equal to the government’s deficit plus (or minus) the current account surplus (or deficit). As this relationship invariably holds by the laws of logic, it can be said with certainty that if private saving were to increase given the budget deficit or if the budget deficit were to be reduced given private saving, the current account balance would be found to have improved by an exactly equal amount. But an accounting identity, though useful as a basis for consistent thinking about the problem can tell us nothing about why anything happens. In my view, while it is true by the laws of logic that the current balance of payments always equals the public deficit less the private financial surplus, the only causal relationship linking the balances (given trade propensities) operates through changes in the level of output at home and abroad. Thus a spontaneous increase in household saving or a spontaneous reduction in the budget deficit (say, as a result of cuts in public expenditure) would bring about an improvement in the external deficit only because either would induce a fall in total demand and output, with lower imports as a consequence.

How is protectionism related to all this? When nations face severe balance of payments issues, they are forced to deflate demand in order to bring the balance of payments at sustainable levels. If that doesn’t work either, nations may try to directly reduce imports. This works via reducing the propensity to import and hence imports. However, it is difficult to take such a step because it can lead to retaliation. As John Maynard Keynes once put it:

During most of the period in which the modern world has been evolved … the failure to solve this problem has been a major cause of impoverishment and social discontent and even of wars and revolutions.

i.e., the failure to resolve the balance of payments problem. The only way to peacefully resolve this issue is by working toward a solution which is good for all. Even the Bank of England (and Mervyn King) has realized this. Else we will just have a long period of low demand and high unemployment, leading to social unrest. More on that some other time.

Wynne Godley used to say that fiscal transfers happen without anyone really noticing. From The Economist, fiscal transfers in the US (finally gets noticed!):

It is frequently asserted by some economists and even some Post-Keynesians that as long as the effective interest rate paid on stocks of debt is less than the growth rate, stock-flow-norms do not keep rising forever. That is, ratios such as public debt/gdp, external debt/gdp do not rise forever at full employment if this condition is maintained, implying thereby that fiscal policy can be used to achieve a higher output and there is nothing one needs to do about the external sector.

It is the purpose of this post to clear such misconceptions.

Fiscal Policy

What can fiscal policy achieve and what are its limitations? In an essay from the centenary conference of 1983, Wynne Godley wrote [1]:

How did Keynes think the economy worked? Any time between 1950 and 1970 1 would have confidently attributed to Keynes, as preeminently important, the following views about economic policy:

(a) Real demand, output and employment are determined via a multiplier process by the fiscal and monetary operations or the government and by foreign trade performance.

(b) Inflation, though influenced by the pressure of demand, is largely indeterminate in terms or economic variables and therefore, if it is to be controlled, requires some kind of direct political intervention.

(c) Fiscal and monetary policies in any one country are potentially subject to important external constraints.

While there is reasonable support for these views about economic policy in Keynes’s writings, there is no warrant for them at all in the General Theory. Indeed it is strange, seeing how commonly the view is attributed to Keynes that fiscal policy is crucial to real output determination, that the General Theory is concerned with an economy in which neither a government nor for that matter a foreign sector exist at all.

Notwithstanding this I still think, not only that the propositions can be correctly attributed to Keynes, but that they are, themselves, essentially correct. I have however been forced to the conclusion that Keynes was a long way from achieving a coherent theoretical basis for maintaining them, and largely for this reason, his ideas have proved very vulnerable to the attacks from many different directions to which they have been subjected, particularly in the last fifteen years.

To points (a), (b) & (c) above, let me add

(a(i)) Higher output is also possible when the private sector expenditure is higher than private sector income.

This was highlighted by Godley himself in the late 90s, when the US economy expanded in spite of a tight fiscal stance and he was the first to write that this process is unsustainable!

Debt Convergence Analysis

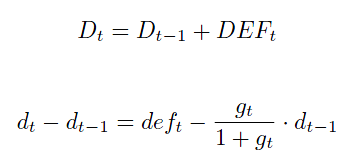

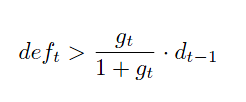

Let us now turn to the question on convergence/divergence of stock-flow norms. In what follows, I simply use debt to denote the public debt or the external debt. Assuming away complications arising from revaluations, we have the identities [2]

Uppercase is for stock of debts, and lower case for debt-to-gdp ratio and g is the growth rate. Note: DEF is primary deficit and excludes interest payments. We will turn to complications added by interest payments soon. Whenever

the stock of debt keeps rising.

Note, when the debt-to-gdp ratio is less than 1 (100%), the sustainability condition is strong on the deficit. The condition DEF < g is at at a debt-to-gdp ratio is 1. Beyond 100%, the condition on the deficit is a bit weaker than DEF < g because the deficit can be between g and g·d.

This argument is sometimes presented differently by some Post Keynesians by including the effective interest rate r. The equation looks like the following when it is included:

It is argued that the third term on the right hand side can be set to be greater than the second term (which is to say that r < g is sufficient to ensure sustainability).

This argument (r < g guaranteeing problems are solved) has no substance. This is because rearranging the terms in the way done above, shows more clearly that the stock-flow ratio rises faster than the case where the analysis was done without the interest rate term!

There is one more complication. It may be argued that growth can only bring down the deficit (the deficit here being the public sector deficit). This is true for the case of a closed economy. The convergence of the public debt-to-gdp ratio is also achieved in the case of a closed economy because interest payments by the government is income for the private sector and they will consume it (although the capitalist class’s propensity to consume is less than that of the worker class). Higher consumption leads to higher national income and hence higher taxes, bringing down the deficit.

Wynne Godley and Marc Lavoie [3] showed how this happens precisely in the case of a closed economy:

This paper deploys a simple stock-flow consistent (SFC) model in order to examine various contentions regarding fiscal and monetary policy. It follows from the model that if the fiscal stance is not set in the appropriate fashion—that is, at a well-defined level and growth rate—then full employment and low inflation will not be achieved in a sustainable way. We also show that fiscal policy on its own could achieve both full employment and a target rate of inflation. Finally, we arrive at two unconventional conclusions: (1) that an economy (described within an SFC framework) with a real rate of interest net of taxes that exceeds the real growth rate will not generate explosive interest flows, even when the government is not targeting primary surpluses, and (2) that it cannot be assumed that a debtor country requires a trade surplus if interest payments on debt are not to explode.

Also, they create some very special scenarios, where the external debt stays sustainable.

However, making the above work is difficult for the case of an open economy in general. This was what the essential argument of the New Cambridge School.

So is there a way to achieve convergence of the stock-flow norm? To achieve that, the external sector deficit (more precisely, the primary balance in the current balance of payments) should be less than the growth rate times the external debt. This creates tensions for demand-management because if the external deficit grows higher than the growth rate, it is usually brought back to a sustainable path by deflating demand. This is because the balance of payments deficit itself will grow if growth is high! (unless exports improve).

There are of course some scenarios which can lead to the convergence of the external debt (if the markets allow it). A more careful treatment will always lead one to studying income and price elasticities of imports, growth in the rest of the world etc.

Other scenarios which could lead to the improvement of the external sector are: promotion of exports leading to more success abroad and luck – market forces miraculously achieving the required depreciation to improve the external sector. Since the latter is mere wishful thinking, we see nations trying to depreciate their currencies because it makes their exports more competitive.

To bring the balance of payments deficit back into balance, there is also the option of restricting imports but in the world of “free trade”, it can create tensions between nations.

There are two more options. The first is to ask your trading partners to appreciate their currencies if they have pegged them but this has to go through negotiations because they want you to do the same! The second (which includes the previous option) is what this blog is about. Since, the external sector creates problems for demand management, one can only think of coordinated efforts by institutions running the world economy, working to achieve higher world demand instead of contracting it.

References

Wynne Godley, Keynes And The Management Of Real Income And Expenditure, p135, Keynes And The Modern World: Proceedings Of The Keynes Centenary Conference, ed. David Worswick and James Trevithick, Cambridge University Press, 1983.

Wynne Godley and Marc Lavoie, Fiscal Policy In A Stock-Flow Consistent Model, p 79, Journal of Post Keynesian Economics / Fall 2007, Vol. 30, No. 1. Draft version available at http://www.levyinstitute.org/publications/?docid=911

Too excited to get my blog going, I finished my first post midway.

Sectoral Imbalances are of many kinds. The US private sector ran deficits for a long time and this lead to the financial crisis and the Great Recession. Frequently, you hear about the shift in the distribution of income and this can also be studied with the Sectoral Balances Approach. Central bankers and policy makers have also realized that global imbalances are unsustainable.

This blog is about how to achieve sustainable growth in the short, medium and the long run and in the author’s opinion can come about only if international policies are coordinated. Policy coordination is not a new concept but for many years before the crisis, imbalances were allowed to continue even though many policy makers took notice of this. In my opinion, these were allowed to continue because the implicit assumption was that “market forces” will work toward resolving the imbalances.

When the world entered a period of catastrophe, governments took action and turned Keynesians overnight. So the G-20 made this statement in the Summit on Financial Markets and the World Economy in 2008:

Use fiscal measures to stimulate domestic demand to rapid effect, as appropriate, while maintaining a policy framework conducive to fiscal sustainability.

to prevent a bigger implosion and later in the 2011 summit

Our aim is to promote external sustainability and ensure that G20 members pursue the full range of policies required to reduce excessive imbalances and maintain current account imbalances at sustainable levels.

However, the G-20 summit participants and the IMF seem to bring about the reversal of imbalances via fiscal contraction – as if there is no negative effect of the latter on domestic and world demand!

Wynne Godley and Francis Cripps [1] described confusions in the policy makers’ minds wonderfully in the Introduction of their 1983 book Macroeconomics

Our objective is most emphatically a practical one. To put it crudely, economics has got into an infernal muddle. This would be deplorable enough if the disorder was simply an academic matter. Unfortunately the confusion extends into the formation of economic policy itself. It has become pretty obvious that the governments of many countries, whatever their moral or political priorities, have no valid scientific rationale for their policies. Despite emphatic rhetoric they do not know what the consequences of their actions are going to be. Moreover, in a highly interdependent world system this confusion extends to the dealings of governments with one another who now have no rational basis for negotiation.

To conclude, the muddle in describing how economies work in Economics has been terrible for world demand (except periods of expansion through unsustainable private sector deficits which end in crises). My blog aims to bring forward ideas in Monetary Economics and how it can be used to achieve active management of economies rather than leaving the task to “market forces”.

References

Wynne Godley and Francis Cripps, p13, Macroeconomics, Oxford University Press, 1983.

This blog post is about the Great Recession, the imbalances which led to it, the use of Keynesian principles by governments of all nations to prevent a deep implosion and how and why the Keynesian mini-revolution didn’t last long. Suddenly, nobody is asking Are We Keynesians Now? and the economics profession has lost lines of communications with governments. Like a Guns ‘N Roses song that goes

What we’ve got here is failure to communicate, some men you just can’t reach.

Will it take another crisis to revive Keynesianism? While, the author is a die-hard Keynesian, he believes that fiscal policy alone cannot resolve the crisis. Governments are aware of this but government officials give only vague replies when taken to task.

The blog in general is/will be about an approach which has roots in the New Cambridge approach to studying economies and how it can be applied to find political economic solutions to put the world in a sustainable path of growth and achieve full employment. It is also about about the Post-Keynesian theory of Endogenous Money and the Stock Flow Coherent Approach. Using the blogosphere as a medium to satiate my crave to put forth my understanding of how economies work, I aim to make a difference. Post-Keynesians emphasize that monetary economies function differently from the chimerical neoclassical story and money cannot but be endogenous. I plan to take the reader into how the monetary and financial system works, the role of various sectors (individuals and institutions) in a demand-led process, their behaviour and what can be done to reverse sectoral imbalances that have built up.

Why Keynesianism was short-lived in the Great Recession is a difficult question to tackle in a single post. Before the 1970s, for many years, the world was run using Keynesian principles and suddenly it fell apart. To me, the situation right now is very reminiscent of what went on during the 70s and the 80s (I am not that old!).

Francis Cripps wrote this brilliantly in a 1983 article What Is Wrong With Monetarism [1]

The conclusion which has to be drawn is that, if a modern economic system is to function properly, a mechanism is required for the management of aggregate demand. Now it happens that the need for management of aggregate demand within a closed national economy can be met rather easily. It is easily met because national economies have an institution called the state which is unique in that it has virtually unlimited powers of credit creation or borrowing (or would have within a closed national economy). Keynesians gave up at this point, thinking that once the need for demand management had been pointed out, and the possibility for demand management by a national government had been understood, the problem of demand management was solved once and for all. Unfortunately, there is no such thing as the state in the contemporary international economy at the international level and the absence of the state as such at the international level is, I believe, a sufficient explanation of why the world economy has run into serious problems of recession …

… The important point is rather that in an international economy the possibilities of national demand management are strictly limited. They are limited by problems of balance of payments adjustment and international finance. Governments that wish to regulate national demand so as to sustain full employment run into problems of increasing trade deficits and, in economics with liberal exchange regimes, loss or confidence and outflows of capital. It is actual or potential balance of payments crises which have been decisive in breaking the habit or Keynesian demand management at the national level. Many national governments are still trying but they are trying under difficulties and they are frightened of balance of payments problems that would result if they tried too hard.

Further, as Francis Cripps concluded, in that brilliant article,

… [U]ntil the economists in our society get around to tackling this problem, we risk being stuck with periods of long recession, even if we are occasionally and accidentally favoured with periods of world boom.

In the book From Keynesianism To Monetarism: The Evolution Of UK Macroeconometric Models [2], Peter Kenway writes:

… There is, however, a greater sense in which the development of the Cambridge Group in that period is more important than the model that came to represent them. That sense stems from the historical significance of those ideas…. the ideas were therefore more ‘anti-Keynesian’ than ‘Keynesian’… what makes the anti-Keynesian views of the 1970s Cambridge Economic Policy Group so significant is that they grew out of the very heart of Keynesianism itself …

… On the one hand, as far as the goals it espoused are concerned, of full employment, of steady growth and of government’s responsibility to pursue these ends, the Group’s commitment to Keynesianism never wavered. But on the other hand, as far as the practice of Keynesianism was concerned, and especially the conceptualization of the reasons for the increasing and evident failure of that practice, the Policy Group not only was part of, but in some respects actually led the revolution against Keynesianism in the UK …

(No) Conclusion

Think my blog posts should be short, but this being the introduction needed to longer. Come back for some Kaldorian Monetary Economics!

References

Francis Cripps, What Is Wrong With Monetarism, pp 55-68, Monetarism Economic Crisis And The Third World, ed. Karel Jansen, Frank Cass, 1983.

Peter Kenway, p 92, From Keynesianism To Monetarism: The Evolution Of UK Macroeconometric Models, Routledge, 1994 (2011 reprint).