In his newsletter, Chartbook, in a recent post Chartbook 442: Global imbalances – A new cocktail in old bottles: World Economy April 2026:, Adam Tooze discusses global imbalances but seems dismissive of the problem.

For some, the continuing accumulation of US sovereign liabilities is a worry. It is true that the US Treasury borrows at rates that are higher than for some rich-country sovereigns. But if that is your concern, why start with the balance of payments? If you want to reduce America’s fiscal overhang, issue less debt. In the current moment it is not just American trade policy that is shocking. Never in American history has the country run such a large budget deficit at a time of relatively full employment.

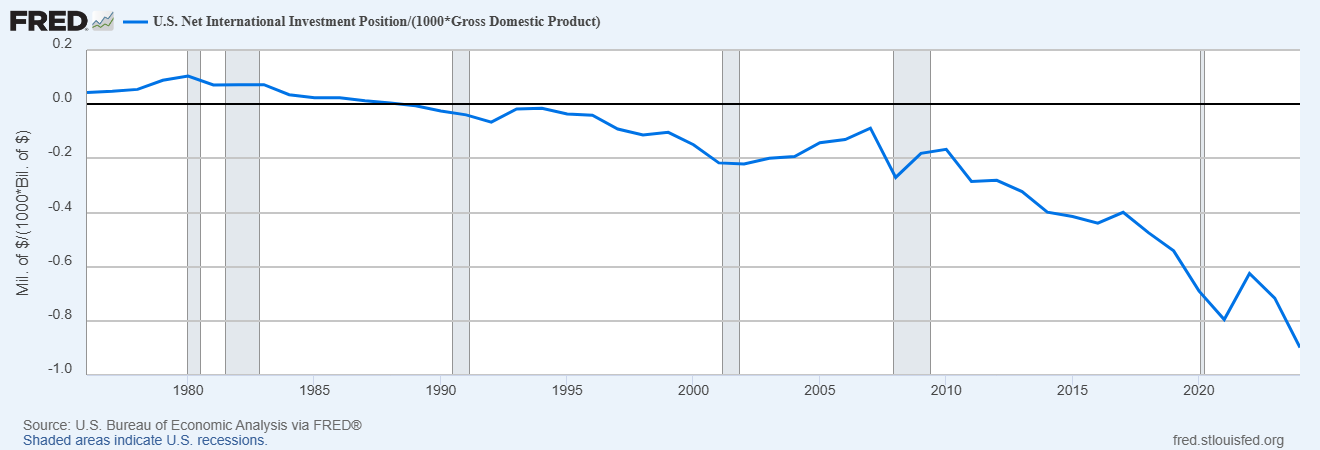

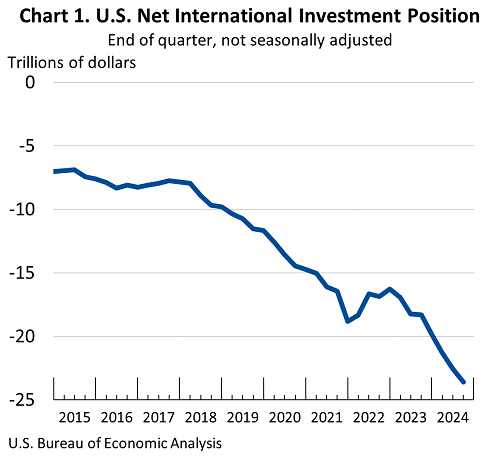

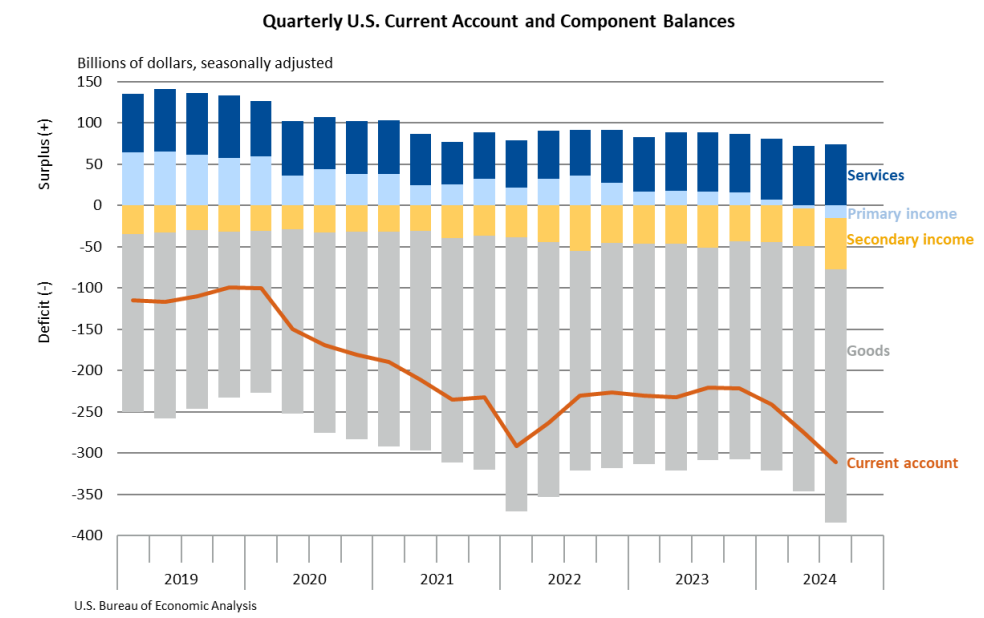

Now that is quite dismissive, especially since the United States is not at full employment. Worse, he comes close to getting it but does not in fact get it: the budget deficit and public debt are large as percent of gdp because of the current account deficits. Having a policy of fiscal contraction would lead to a fall in gdp. Tooze seems to be minimising the causality from the current account balance to budget deficit. Public debt is not itself a problem but reflects the huge negative net international investment position of the United States. Large deficits because the balance of payments situation reduces the expenditure multiplier to bring sufficient taxes in.

From a larger perspective, Tooze offers no solution to all this. Why would he? The purpose of his article is to play down the problem.

Years later, Adam Tooze is going to be writing a mea culpa on how he was wrong on this problem.

The irony is that Adam Tooze is highly influenced by Wynne Godley, who worried about imbalances, and proposed to change the economic order to move toward a system of balanced trade combined with expansionary fiscal policies. In his 2018 book Crashed, Tooze says:

Wynne Godley was a mentor and teacher of a very different kind. Spontaneously warm and generous in spirit, he took me under his cape in my first year at King’s and introduced me, and a group of my contemporaries, to what, at the time, was a highly idiosyncratic brand of economics. In so doing he provided a model of intellectual warmth and vitality. And he confirmed doubts that had been gestating in me about the IS-LM model that was my first great love in economics. Wynne introduced me to the importance of looking “beyond the flows” and insisting on stock-flow consistency in macro models. I don’t think this book, written almost thirty years later, would have been the same without his early influence.