The US public debt is rising $1 trillion every 100 days, headlines say. Is the US public debt sustainable?

Well, the US net international investment position is on an unsustainable path and that reflects on the US public debt. The solution is not fiscal contraction but using policy to address the US balance of payments.

According to the Federal Reserve release Z.1, the US net international investment position was −$19.37 trillion at the end of 2023. (Table B.1, line 24), while the Gross Domestic Product for 2023 was $27.36 trillion. (Table F.2, line 1).

Since government deficit is connected to the current account balance by an identity,

NL = DEF + CAB

where NL is the private sector net lending, DEF is the government deficit, CAB is the current account balance, it suggests a connection between the government deficit and current account balance not just as a static identity but behaviourally and there is a connection between the public debt and the net international investment position. In behavioural stock-flow consistent models, this can be seen more clearly.

The US has had high current account deficits and that has put the US economy on an unsustainable path.

And in general, there is no market mechanism to resolve imbalances. Lots of political discourse in the US has been around trade/tariffs etc. Industrial policy has also appeared. Note that many people define industrial policy as government picking winners, but that is misleading/a deceit. The aim of industrial policy is to improve competitiveness of a country and that has to do with exports and imports.

A lot of people complaining about the path of the US public debt seem to suggest that the way to solve it is via fiscal contraction. But that causes a deflation of the US economy and increases unemployment.

But sadly, the other side denies that there is any problem with sustainability/trade etc. So we have crazy politics. An important problem is the lack of understanding how economic forces operate. Or that people’s self-interests stand in the way of understanding.

The resolution of the problem lies in the US asking the rest of the world to increase growth by more fiscal expansion (which would increase US exports and reduce US imports relative to GDP), use protectionist measures and industrial policy and then work toward a system of planned/regulated trade where international trade is generally balanced.

This is a continuation of a recent post at this blog, Public Debt And Current Account Deficits, in which I argued that the current account balance of payments affects the public debt.

A usual objection to the connection is that the two deficits—current account deficit and the budget deficit—although connected by an identity, don’t move together and in fact move in the opposite direction frequently. This point was raised by the blog Econbrower, yesterday.

The identity in question is:

NL = DEF + CAB

where, NL is the private sector net lending, DEF is the government’s deficit and CAB is the current account balance of payments (and is to a zeroth order approximation, exports less imports).

This is not a behavioural hypothesis but still a useful tool to build a narrative. Also, the causality connecting the identities is domestic demand and output at home and abroad.

Imagine, initially that NL is a small positive relative to GDP (for example, NL/GDP = 2%), Also remember that,

NL = Private Income − Private Expenditure

Now assume that private expenditure rises relative to private income. This will lead to higher GDP, a higher national income and a rise in imports because of income effects and hence a lower CAB. It will also lead to higher taxes because of higher income and hence will reduce the budget deficit, DEF, ceteris paribus.

So if the current account balance is in deficit, it would mean that the budget deficit and the current account deficit move in opposite directions.

That’s the theoretical basis for the empirical relationship. But that in itself isn’t the whole story. This is because the other balance—net lending, NL—has a life of its own. As is the case in the United States and several western countries, it turned negative once or twice in the 1990s the 2000s, and when the private sector’s debt rose, it made a sharp U-turn into the positive territory. The blue line in this graph:

Click the graph to see it on FRED.

So, if net lending reverts to its mean of staying positive, one can then conclude that the cumulative budget deficit, or the public debt is affected by cumulative current account deficits.

At any rate, the public debt shouldn’t be the main object of study. What’s more important is the international investment position. And it’s an identity that:

NIIP = cumulative CAB + Revaluations

where, NIIP, is the net international investment position.

A nation which runs current account deficits can become indebted to the rest of the world. IIP is the position of assets and liabilities of resident sectors of a nation. So, the net debt (the negative of NIIP) is the nation’s debt.

The above linked Econbrowser post brings in the complication of revaluations to deny the relationship between CAB and NIIP. But revaluations can’t save you for long.

In short, both public debt and NIIP depend on current account deficits.

Finally a weak analogy: if you play in the rain, you might enjoy it as well. But then if you get sick, you can’t say, “I felt so good playing in rains, so playing in the rain didn’t make me sick”. Saying the two deficits (current account and budget) move in opposite directions is an argument like that.

Yesterday, there was an article at Vox which takes issue with a statement from Donald Trump which connects the US public debt with current account deficits.

Trump ran his campaign on dividing people, is out to destroy health care and wants a regressive system of taxation and so should be resisted. At the same time, a blanket opposition is counterproductive, especially when it is an important matter.

Vox quotes Trump:

For many, many years the United States has suffered through massive trade deficits; that’s why we have $20 trillion in debt.

In response, Vox claims:

The US trade deficit refers to the fact that the US imports more from the world than it exports. The national debt is the result of the fact that the US government spends more revenue than it collects. There’s no direct relationship between the two.

The whole article is written to claim that there is no connection. But anyone who knows the sectoral balances identity will recognize that there is a connection.

So the sectoral balances identity is:

NL = DEF + CAB

where, NL is the private sector net lending, DEF is the government’s deficit and CAB is the current account balance of payments (and is to a zeroth order approximation, exports less imports).

Of course, this is an identity and shouldn’t be confused for any behavioural hypothesis but it’s still useful in creating a narrative around a model (such as an SFC model) with behaviour for households, firms, the financial system, the government and the rest of the world.

On an average the private sector net lending is a small positive number relative to GDP (such as 2%), although it can fluctuate a lot. So for the U.S. economy, we saw that it was negative a lot in the 2000s and then reverted to a large positive just before and during the crisis.

One should of course keep in mind the correct causality connecting the three terms. What connects them is demand and output at home and abroad.

So the government’s deficit is affected by exports and imports. If there’s a large current account deficit, there’s a fall in demand and hence output and hence income and hence taxes leading to a higher government deficit than otherwise. Deficits in turn affects the public debt.

In other words, the U.S. public debt would have been lower, ceteris paribus, had the problem of the U.S. trade imbalance would have been addressed. This would have happened because of higher national income and higher taxes.

People don’t see the connection because they are comparing different nations. So for example, Japan has been successful in international trade and yet has a high public debt. In the other extreme, Australia has had large current account deficits over the years and public debt much lower than Japan (relative to GDP). But one should do a ceteris paribus comparison.

This quote of Abba Lerner from his article “The Burden of the National Debt,” in Lloyd A. Metzler et al.,Income, Employment and Public Policy (New York, 1948), p. 256 is frequently quoted in the Post-Keynesian blogosphere:

One of the most effective ways of clearing up this most serious of all semantic confusions is to point out that private debt differs from national debt in being external. It is owed by one person to others. That is what makes it burdensome. Because it is interpersonal the proper analogy is not to national debt but to international debt…. There is no external creditor. “We owe it to ourselves.”

This is unfortunately inconsistent with his “functional finance”. Abba Lerner clearly says that external debt can be problematic. However he probably never realized that if his advise is followed in running fiscal policy, a nation’s balance of payments will deteriorate and its international debt will increase (because current account balance adds to the net international investment position).

Public debt is not the same the negative of the net international investment position but it’s related as the external debt is directly or indirectly picked up by the public sector.

Sound finance is all junk science but Abba Lerner is not your friend to learn about money, debts, deficits and all that.

Frequently, discussions about debt sustainability have discussions about the importance of the interest rate and growth in debt sustainability analysis. See for example, today’s Paul Krugman’s post on his blog. It is concluded that as long as the rate of interest is below the rate of growth, the ratio public debt/gdp doesn’t explode. Unfortunately, this result is erroneous.

John Maynard Keynes’ biggest disservice to the profession is to not start with the open economy. In my view, debt sustainability is tightly connected to balance of payments.

Imagine a nation whose exports is constant. If output rises, it will have adverse effects on the current account balance of payments because of income induced increase in imports. This will have an adverse effect on the international investment position of the nation: the net international investment position will keep deteriorating unless output is slowed down or some measure is taken to improve exports. In the case of rising exports, there is a similar constraint, except it is weaker but dependent on the rate of growth of exports.

If the ratio net international investment position/gdp keeps deteriorating, either the public debt to non-residents or private indebtedness to non-residents or both have to keep rising, all unsustainable.

There are some complications. A nation’s balance of payments also depends on how assets held abroad and liabilities to foreigners affect the primary income account of balance of payments. Also, the exchange rate can depreciate (or be devalued in fixed-exchange rate regimes) improving exports and reducing imports. However assuming that exchange rate movements do the trick is believing in the invisible hand. Foreign trade doesn’t just depend on price competitiveness but also on non-price competitiveness. These complications are highly interesting but do not affect the fundamental fact that a nation’s success is dependent on the success of corporations to compete in international markets for goods in services.

Even the conclusion that the government should contract fiscal policy and aim for a primary surplus in its budget balance or else the ratio public debt/gdp keeps rising if the rate of interest is greater than the rate of growth is erroneous. Consider a closed economy. An expansion in fiscal policy will automatically raise output and gdp and hence tax collections to prevent the ratio public debt/gdp from exploding. The public sector balance may hit primary surpluses but not due to contraction of fiscal policy or targeting a primary surplus in its budget balance.

In short, although the rate of interest and the rate of growth are important in debt sustainability analysis, it is not as easy as is usually presenting in macroeconomics textbooks and in the blogosphere. For a more detailed analysis see the reference below.

Reference

Godley, W. and B. Rowthorn (1994) ‘Appendix: The Dynamics of Public Sector Deficits and Debt.’ In J. Michie and J. Grieve Smith (eds.), Unemployment in Europe (London: Academic Press), pp. 199–206

If a government (outside monetary unions) can make a draft at the central bank, why do rating agencies rate governments’ creditworthiness?

In this post, I will attempt to describe the dynamics of defaults and restructurings by going through some monetary economics of open economies.

Carmen Reinhart and Kenneth Rogoff wrote a book in 2009 titled This Time Is Different: Eight Centuries Of Financial Folly or simply This Time Is Different arguing that governments do indeed default – both in debt denominated in the domestic and foreign currencies. They blame the public debt and the government for the public debt – hence giving the innuendo that governments across the planet should attempt to cut public debt by tight fiscal policies. This is an illegitimate conclusion – on which I will say more below.

At another extreme are the Chartalists who argue that the government cannot “run out of money” and hence fiscal policy has no monetary constraints. Sometimes they qualify this statement by saying that the currency they are discussing are “sovereign currencies”. Now, there are various definitions of what a sovereign currency is but it is frequently pointed out by them that nations who have seen restructuring of government debt did not have a “sovereign currency” – because the currency is either pegged or fixed or it is the case that the government had a lot of debt in foreign currency which presumably allows defaults/restructuring of government debt in the domestic currency as well. The motivation behind this is Milton Friedman’s idea that nations should freely float their currencies in international markets and that markets will clear and that the State intervention in the currency markets can only make things worse. Hence Reinhart/Rogoff don’t prove them wrong – according to them – since the situations are supposedly different.

We will see that while there is some truth to it, the notion of a “sovereign currency” is highly misleading. Such intuitions are coincident with the incorrect notion that indebtedness to foreigners (in domestic currency) is just a technical liability and there’s nothing more to that!

Here’s S&P’s article on the methodology it uses to assign ratings on governments: Standard & Poor’s – Sovereign Government Rating And Methodology. One can see the importance it gives to the external sector. However, S&P does not provide a mechanism on how a government will finally end up defaulting. The purpose of this post is to look into this.

Before this let us make a connection between the public debt and the net indebtedness of a nation. Most people in the planet confuse the two. The former is the debt of the government whereas the latter is the (net) indebtedness of the nation as a whole. This is the net international investment position (adjusting for traditional settlement assets such as gold) with the sign reversed. This can be obtained by consolidating all the sectors of an economy and the consolidation involves (for example) netting of the assets of the domestic private sector held abroad and also its gross indebtedness to the rest of the world.

So one can think of two extremes:

Japan – with a high public debt of about 195% of gdp (includes just the central government debt), while being a net creditor of the world. It’s NIIP is about 50% of gdp (data source: MoF, Japan)

Australia – with a low public debt of 18% of gdp and NIIP of minus 59% of gdp.

So in the case of Japan, while the government is a huge debtor, the nation as a whole is a creditor, whereas in the case of Australia, it is the opposite. So the rating agencies get it wrong or opposite!

Let us first assume a closed economy. The greatest starting point in analyzing economies is the sectoral balances approach. For a closed economy it is:

NAFA = DEF

where NAFA is the Net Accumulation of Financial Assets of the private sector and DEF is the government’s budget deficit. If the private sector wants to accumulate a lot of financial assets, and the government wants to run the economy near full employment, the public debt will be higher, the higher the propensity to save, for example. (This is not as straightforward as presented here but can be shown in a simple stock-flow consistent model). So unlike what neoclassical economists think, the level of public debt is somewhat irrelevant. Neither does the government has too much trouble in financing its debt because the public debt is the mirror image of the private sector net financial asset position.

Now let us take the case of an open economy. The sectoral balances identity now is

NAFA = DEF + CAB

A deficit in the current account implies an increase in the net indebtedness to foreigners. Unless the markets miraculously clear with the exchange rate adjusting to bring the CAB in balance, a deficit in the current account implies the nation as a whole has to attract foreigners to finance this deficit i.e., via a lower NAFA or higher DEF. In the long run, the private sector is accumulating financial assets (or has small positive NAFA) and the whole of the current account balance is reflected in the public sector balance.

So the debate fixed vs floating doesn’t help too much. A relaxation of fiscal policy may spill over into higher imports with the public debt and the net indebtedness to foreigners keeps rising forever to gdp. Hence nations typically have to curb growth to bring the current account into balance.

This is theory. So let’s look at an open economy mechanism of an event of default by the government as a story.

In the following, I will use the phrase “pure float” instead of the dubious terminology “sovereign currency”.

Here’s the simplest model:

In the above, a nation with its currency on a pure float and with zero official sector liabilities in foreign currencies has a somewhat weak external position in 2012. Now, according to some of the Neochartalist arguments this nation can’t default on its government debt. However this is a wrong conclusion as the scenario above hightlights. In the scenario constructed, the balance of payments position weakens over the years (and I have mentioned that roughly in 2020 it weakens). In 2022, foreigners are no longer willing to finance the debt. This may be due to a capital flight or due to the inability of the banking system to maintain a low net open position in foreign currency. The depreciation of the domestic currency isn’t sufficient to clear the fx markets and the official sector (either the central bank or the government’s treasury) necessarily has to intervene in the foreign exchange markets by issuing debt denominated in foreign currency. The government is then acting as the borrower of the last resort and the objective is to use the proceeds to partially have more foreign exchange reserves and/or to sell the foreign currency proceeds from the debt issuance to clear the fx markets. The government is then left with a net liability position in the foreign currency. Soon the external situation worsens to the point requiring official foreign help – such as from the IMF – which promises to help and requires a restructuring of the debt both in domestic and foreign currencies.

Free marketers have a blind belief in the markets and the theories are built on the assumption that markets always clear. The recent crisis has highlighted that this isn’t the case. Even for the case of Australia – whose currency can be considered closed to being pure float – has had issues in the external sector and the Reserve Bank of Australia had to borrow in US dollars from the Federal Reserve (via swap lines) to help Australian banks meet their foreign currency funding needs during the crisis.

Of course the above is not typical but to prevent the external vulnerability to go out of control, governments keep domestic demand low and a lot of times, they over-do this.

The point of the exercise is to prove that it is not meaningless to think of nations becoming bankrupt in whichever situation one can think of and it doesn’t help to laugh at the rating agencies and make fun of them – possibly with the exception for the case of Japan. Statements such as “government with a sovereign currency cannot become bankrupt” are simply misleading. In the above, the Chartalists would argue that the currency was not sovereign and they were not wrong about the default but the currency was sovereign in their own definition in 2012!

Here are some comments on some nations.

Japan: As mentioned above, Japan is a net creditor of the rest of the world and partially as a consequence of that, most of the Japanese government’s debt is held internally. The rating agencies are aware of this but in spite of this continue to make comments on the creditworthiness of the Japanese government. It is possible that residents may transfer funds abroad for unknown reasons (which the raters for some reason suspect) but it may require just a minor interest rate hike to prevent this from happening. Japan has a relatively strong external situation and hence has no issues in financing its government debt.

Canada: Nick Rowe of WCI mentioned to me on his blog that worrying about the balance of payments constraint is like “beating a dead horse” – citing the example of Canada which has floated its currency and it seems has no trouble with its external sector. But this ignores other things in the formulation of the problem. Canada is an advanced nation and an external situation which is not weak. However, a growth of the nation much faster than the rest of the world will lead to a worsening of the external situation. To some extent the nation’s external situation has been the result of its relatively better competitiveness of exporters compared to its propensity to import and a demand situation which either as a conscious attempt of demand management of the government or by pure fluke has helped its external situation remain non-vulnerable.

United States: The US dollar is the reserve currency of the world and slowly over time, the United States has turned from being a creditor of the rest of the world to becoming the world’s largest debtor nation. (Again not due to its public debt but because of its net indebtedness to foreigners). The US external sector is a great imbalance and any attempt to get out of the recession by fiscal policy alone will worsen its external situation leading to a crash at some point. S&P is right! So to come out of the depressed state, the nation has to complement fiscal expansion with improvement of the external situation such as by (and not restricted to) asking trading partners to not revalue their currencies. Still for some reasons bloggers at the “New Economic Perspectives” think that

… Bernanke also knows that the US has infinite ability to finance these fiscal components, that there is no solvency issue and that the policy rate and both ends of the yield curve are under the direct control of the Fed.

Back to This Time Is Different. While Reinhart and Rogoff’s analysis of government debt may be useful, their conclusions can be destructive for the world as a whole. The domestic private sector of a nation needs continuous injection from outside so that it can run surpluses in general and tightening of fiscal policies will lead to a depression. Global imbalances is crucial in understanding the nature of this crisis (and not public debt alone) and even coordinated attempts to reflate economies may provide only a temporary relief. Since failure in international trade restricts the growth of nations and their attempts to reach full employment, what the world needs is an entirely different way to run the economies under managed trade with fiscal expansion. Ideas of “free trade” such as that outlined here by Alan Blinder simply help some classes of society at the expense of others because it relies on the “market mechanism” which has failed over and over again.

This brings me to “sovereignty”. As argued, the concept “sovereign currency” is almost vacuous (except highlighting the problems of the Euro Area) but sovereignty as argued by Wynne Godley in his great 1992 article Maastricht And All That and by Anthony Thirlwall in the same year on FT (my post on it here Martin Wolf Pays A Generous Tribute To Anthony Thirlwall) definitely have great importance. Some of Thirwall’s concepts of economic sovereignty in the article were: the ability to protect and encourage strategic industries, the possibility of designing systems of managed trade to even out payments imbalances, the ability to protect against certain countries with persistent surpluses, differential taxes which discriminate in favour of the tradeable goods sector.

James Tobin was one of the greatest economists. He had stock-flow consistency, understood how the monetary and financial system worked and had great ideas on open economy macroeconomics. However, he struggled to express his ideas at a more formal level, especially since he used some neoclassical formalism.

This post may be of interest to Neochartalists. It seems there was a Committee on Public Debt in 1949 and they released a reportOur National Debt. James Tobin reviewed the report.

Tobin begins by saying:

The peace of mind of a conscientious American must be disturbed every time he is reminded that his government is 250 billion dollars in debt. He must be shocked by the frequent announcement that every newborn baby is burdened, not with a silver spoon, but with a debt of $1700. The citizen depressed by these somber calculations will find no solace in the book under review. The Committee on Public Debt Policy and its advisors are leaders in the worlds of banking, insurance, business, economics, and education. Experts in finance, they have undertaken to enlarge public understanding of the debt. The Committee believes that the challenge can be met, the difficulties overcome, the crisis surmounted. But these hopeful prophecies are voiced in the tone of a leader summoning his people to an uphill struggle which will demand all their courage, wisdom, and devotion. The world is too full of such struggles, and the Committee does the public it wishes to enlighten no service by elevating to epic status the management of the national debt.

The book permits lay readers to retain misconceptions of the nature of public debt and exaggerated impressions of its present size. The amateur is bound to project to a national scale his own experience of private debt. To him “debt” is a frightening word, and counting debt in billions staggers his imagination. But a national debt is a burden on the nation analogous to the burden of a private debt on an individual only if the nation is in debt abroad. If the United States owed 250 billion dollars to foreign creditors, our real national income would be reduced by the five billion dollars of our annual production exported to pay the interest. As the debt became due, we would face additional sacrifices to repay it, or we could extend it only on terms allowed by foreign lenders. Happily the 250 billion dollars are owed by the Government to its own citizens. Indeed, about one quarter of the present debt is not even an obligation of the Government to its citizens; it is essentially a debt of the federal government to itself or to state and local governments. Payments of interest are not an external drain on our production, and, thanks to the lending power of the Federal Reserve System, the Government need never encounter difficulty in refinancing existing debt or in borrowing more money.

The Committee’s report seemed to have been insistent on retiring the public debt on which Tobin says:

… Deficit spending in times of high demand and full employment is certainly inflationary. This does not prove that old public debt, merely by its continued existence, is inflationary and should be retired.

The present debt represents almost entirely the wartime savings of Americans, who earned record incomes in war production and could not find consumers’ goods to buy. Had the war been financed wholly by taxation, the public could not have acquired these savings …

And on interest payments:

The second possible danger in the public debt is the burden of interest charges. Transfer of interest from taxpayers to bondholders is a nuisance. Committing a large share of the national income in advance as interest on the debt weakens incentives for effort and risk-taking. Interest transfers may promote income inequality. These evils are scarcely serious enough to justify sacrificing other objectives of current public policy to a commitment for debt retirement. Interest payments now amount to only two per cent of the national income; the percentage should decrease with economic progress provided full employment and low interest rates are maintained.

And finally:

… Decisions concerning current taxes and appropriations should be geared to the current economic situation; they should not be influenced by irrational fear of the national debt. But the debt will undoubtedly continue to be an ideological symbol invoked in every public debate. The purpose of this book, the advancement of popular understanding of the debt, remains unfulfilled.

Banca d’Italia – Italy’s National Central Bank – released its Financial Stability Report, Nov 2011 recently. With movements in Italian government bond yields making headlines, the following graphs from the report might be useful.

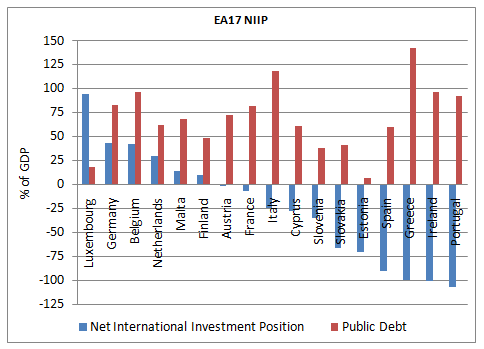

The Euro Zone is under a crisis. Is there a chart which shows what the underlying factor is which makes the difference ? Below:

You can see that the external situation is clearly the one which makes the difference as opposed to the public debt. It’s true that Belgium’s bond market is under pressure – creditors may not like high public debt but I think the graph is still useful.