Marc Lavoie’s has a new bookPost-Keynesian Growth Theory: Selected Essays with a collection of his essays on some of his important papers on growth. The cover features Michal Kalecki, Nicholas Kaldor, Joan Robinson and Luigi Pasinetti. Will be out soon.

In the same series, there’s also a book from 2020 Post-Keynesian Monetary Theory: Selected Essays. You can preview the introduction to this book on Google Books. So even if you’ve read all the papers, don’t miss the detailed introduction which gives an idea of his thoughts through the years. It also has a foreword by Louis-Philippe Rochon. And an interview with him on that book.

There’s a new short biography of Nicholas Kaldor titled Nicholas Kaldor’s Economics: A Review by Luis Gomes. The author reminds of Kaldor’s proposals for the world as a whole, something which is highly needed today more than ever (and something I regularly refer to):

In 1984 Nicholas Kaldor gave a series of lectures in Italy, which become a posthumous book in 1996. These lectures [“Causes of Growth and Stagnation in the World Economy” … ] presented an integrated set of policies with which to tackle economic problems. In this series of lectures, Nicholas Kaldor commented on the four basic principles for good macroeconomic administration: (i) it is needed a coordinated fiscal action which include a set of targets for a balanced balance of payments and a full employment budget; (ii) the interest rate should be the lowest possible: (iii) it is important to prevent the volatility of international commodity prices (via stocks and via an international currency) (iv) it is necessary to overcome chronic inflation trends under full employment, due to the system of adjusting wages via sectoral collective agreement …

There are many biographies (from short articles to full papers) and I thought I should list them:

A short article titled Portrait: Nicholas Kaldor by Luigi Pasinetti, published in 1981 published in Challenge.

Luigi Pasinetti’s Nicholas Kaldor: A Few Personal Notes, published in 1983.

Anthony Thirlwall’s 1987 book titled Nicholas Kaldor,

Anthony Thirlwall’s 1987 article Nicholas Kaldor 1908–1986. Republished 1991 in the book Nicholas Kaldor And Mainstream Economics Confrontation Or Convergence? and again in 2015 in the book Essays On Keynesian And Kaldorian Economics.

Geoffrey Harcourt’s articleNicholas Kaldor, 12 May 1908–30 September 1986 published in 1988 in Economica and republished in the book Post-Keynesian Essays In Biography by Harcourt himself.

Ferdinando Targetti’s 1992 bookNicholas Kaldor: The Economics And Politics Of Capitalism As A Dynamic System.

Marjorie Shepherd Turner’s bookNicholas Kaldor And The Real World published in 1993.

Anthony Thirwall’s sectionNicholas Kaldor, A Biography in Nicholas Kaldor’s book Causes Of Growth And Stagnation In The World Economy published posthumously in 1996.

Adrian Wood‘s entryKaldor, Nicholas (1908–1986) in The New Palgrave Dictionary Of Economics published in 2008.

John E. King’s bookNicholas Kaldor published in 2008.

Luigi Pasinetti’s chapter Nicholas Kaldor (1908–1986): Growth, Income Distribution, Technical Progress in his bookKeynes And The Cambridge Keynesians: A ‘Revolution in Economics’ To Be Accomplished, published in 2009.

John E. King’s chapterNicholas Kaldor (1908–1986) in the book Handbook On The History Of Economic Analysis Volume I published in 2016.

John E. King’s chapterNicholas Kaldor (1908–1986) in The Palgrave Companion To Cambridge Economics published in 2017. (h/t Marc Lavoie).

Apart from the above, following are useful to know about Nicholas Kaldor, although can’t be described as biography:

Introduction by Ferdinand Targetti and Anthony Thirlwall to the bookThe Essential Kaldor, a collection of papers of Kaldor, published in 1989.

The practical triumph of the free trade doctrine is the fact that even the severest critics of the general policy line of noninterference usually find it difficult to free themselves from its fascination.

– Gunnar Myrdal

I was reading this bookThe Dynamics Of Poverty: Circular, Cumulative Causation, Value Judgments, Institutions And Social Engineering In The World Of Gunnar Myrdal by Mats Lundahl, which is a sort of an intellectual biography published in 2021.

Gunnar Myrdal was the first to apply his own idea of circular, cumulative causation to international trade and success and failure of nations. Roughly it means: success breeds further success and failure begets more failure, in the words of Nicholas Kaldor.

Although the idea was original to Myrdal, the detailed mechanism was first formulated by Nicholas Kaldor in 1970 in his paperThe Case For Regional Policies.

According to Lundahl’s book Myrdal’s genius can be found in the following works (page 82):

Gunnar Myrdal also spent much of the 1950s working on problems related to poverty and inequality on the international level and on the relation between polarization between regions within a country and polarization between countries. This resulted in a ‘trilogy’: An International Economy, Development and Under-Development: A Note on the Mechanism of National and International Economic Inequality, usually referred to as his Cairo lectures, and Economic Theory and Under-Developed Regions (or Rich Lands and Poor).18

…

18Myrdal (1956a, 1956b, 1957a, 1957b).

…

References

…

Myrdal, Gunnar (1956a), An International Economy: Problems and Prospects. New York: Harper & Brothers Publishers

Myrdal, Gunnar (1956b), Development and Under-Development: A Note on the Mechanism of National and International Economic Inequality. Cairo: National Bank of Egypt

Myrdal, Gunnar (1957a), Economic Theory and Under-Developed Regions. London: Gerald Duckworth & Co

Myrdal, Gunnar (1957b), Rich Lands and Poor: The Road to World Prosperity. New York: Harper & Brothers

…

You can find the first and the third/fourth book (which are the same but just different names in the UK and the US) at Internet Archive in this link. “Cairo Lectures”, seems difficult to obtain, but the important part Trade As A Mechanism Of International Equality can be found in Gerald M. Meier’s book Leading Issues In Economic Development.

Ramesh Chandra has a recently released bookEndogenous Growth In Historical Perspective: From Adam Smith To Paul Romer, and one of his chapters is on Nicholas Kaldor and circular and cumulative causation.

Chandra’s own views are different but I thought his description of Gunnar Myrdal and Nicholas Kaldor’s insights was amazing with the most appropriate quotes like the following (from page 201 in print/209 in pdf):

Gunnar Myrdal (1956, 1957) and Nicholas Kaldor (1978), on the other hand, argued that because of the operation of circular cumulative causation free trade led to interregional and international inequalities. Myrdal (1956) maintained that “if left to its own course, economic development is a process of circular and cumulative causation which tends to award its favours to those who are already well endowed and even to thwart the effort of those who happen to live in regions that are lagging behind” (quoted from Meier 1989, p. 385). Further, “on the international as well as national level trade does not by itself necessarily work for equality. A widening of markets strengthens often on the first hand the progressive countries whose manufacturing industries have the lead and are already fortified in surroundings of external economies, while the underdeveloped countries are in continuous danger of seeing even what they have of industry and, in particular, their small scale industry and handicrafts outcompeted by cheap imports from industrial countries, if they do not protect them” (ibid., p. 385). International trade does promote primary exports from developing countries but here they face adverse demand conditions or inelastic demand in world markets. Any technological improvements which reduce primary goods prices benefit the importing countries. Thus, “forces in the markets will in a cumulative way tend to cause even greater international inequalities between countries as to their level of economic development and average national income per capita” (ibid., p. 385).

Likewise, Kaldor (1978), in his paper “Nemesis of free trade”, thought that free trade may be good under constant costs but under increasing returns it benefitted some countries (or regions) at the cost impoverishment of others. He agreed with Myrdal that international trade perpetuated international inequalities, and developing countries would do well if they industrialized behind tariff and quantitative restrictions. Kaldor also stated that protectionism was good not only for developing countries but also for a developed country like Britain. In the initial stages of her growth, free trade suited Britain. But after Germany, France, USA, and Japan industrialized, Britain could not compete and one market after another became closed. Had Britain not been ideologically wedded to free trade, her living standards would have been much better.

…

References

…

Kaldor, Nicholas. 1978. Nemesis of free trade. In Further Essays on Applied Economics. London: Duckworth.

…

Meier, Gerald M. 1989. Leading Issues in Economic Development. Oxford and New York: Oxford University Press.

…

Myrdal, Gunnar. 1956. Development and Underdevelopment. Cairo: National Bank of Egypt Fiftieth Commemoration Lectures.

Myrdal, Gunnar. 1957. Economic Theory and Underdeveloped Regions. London: Gerald Duckworth

In Anthony Thirlwall’s essayNicholas Kaldor: A Biography, 1908–1986, (first published in 1987 and republished in 2015, [note: he has a full biography too]), there’s a para which has both the history of Kaldor’s thoughts on circular and cumulative causation and a short explanation:

As Kaldor grew older (and perhaps wiser?), he lost interest in theoretical growth models and turned his attention instead to the applied economics of growth. Two things particularly interested him: first, the search for empirical regularities associated with ‘interregional’ (country) growth rate differences, and secondly, the limits to growth in a closed economy (including the world economy). The distinctive feature of all his writing in this field was his insistence on the importance of taking a sectoral approach, distinguishing particularly between increasing returns activities on the one hand, largely a characteristic of manufacturing, and diminishing returns activities on the other (namely agriculture and many service activities). Kaldor’s name is associated with three growth ‘laws’ which have become the subject of extensive debate.73 The first ‘law’ is that manufacturing industry is the engine of growth. The second ‘law’ is that manufacturing growth induces productivity growth in manufacturing through static and dynamic returns to scale (also known as Verdoorn’s Law). The third ‘law’ states that manufacturing growth induces productivity growth outside manufacturing, by absorbing idle or low productivity resources in other sectors. The growth of manufacturing itself is determined by the growth of demand, which must come from agriculture in the early stages of development, and from exports in the later stages. Kaldor’s original view74 was that Britain’s growth rate was constrained by a shortage of labour, but he soon changed his mind in favour of the dynamic Harrod trade multiplier hypothesis of a slow rate of growth of exports in relation to the income elasticity of demand for imports, the ratio of which determines a country’s balance of payments constrained growth rate. Because fast growing ‘regions’ automatically become more competitive vis á vis slow growing regions, through the operation of the second ‘law’, Kaldor believed that growth will tend to be a cumulative disequilibrium process—or what Myrdal once called a ‘process of circular and cumulative causation’,—in which success breeds success and failure breeds failure. He articulated these ideas in several places, most notably in two lectures: his Inaugural Lecture at Cambridge in 1966,75 and in the Frank Pierce Memorial Lectures at Cornell University in the same year.76 Most of the debate concerning Kaldor’s growth laws has centred on Verdoorn’s Law and the existence of increasing returns. Kaldor drew inspiration for the theory from his early teacher, Allyn Young, and his neglected paper ‘Increasing Returns and Economic Progress’.77 Young, in turn, derived his inspiration from Adam Smith’s famous dictum that productivity depends on the division of labour, and the division of labour depends on the size of the market. As the market expands, productivity increases, which in turn enlarges the size of the market. As Young wrote ‘change becomes progressive and propagates itself in a cumulative way’, provided demand and supply are elastic. Hence increasing returns is as much a macroeconomic phenomenon as a micro-phenomenon, which is related to the interaction between activities, and cannot be adequately discerned or measured by the observation of individual industries or plants. Kaldor was convinced by theoretical considerations and by his own research, and that of others, that manufacturing is different from agriculture and most service activities in its ability to generate increasing returns in the Young sense.

…

Notes

…

See A. P. Thirlwall (ed.), ‘Symposium on Kaldor’s Growth Laws’, Journal of Post-Keynesian Economics, Spring 1983.

See Causes of the Slow Rate of Economic Growth of the United Kingdom (CUP, 1966).

As note 74

Strategic Factors in Economic Development (Cornell University, Ithaca, New York, 1967).

Economic Journal, December 1928.

…

I don’t see much reference to short book Strategic Factors In Economic Development anywhere and I wasn’t even aware of the book till I reread this passage again recently. Must get it. Although according to this review, there’s nothing much in addition to Causes Of The Slow Rate Of Economic Growth Of The United Kingdom.

I have never been able to appreciate Kaldor’s earlier models, perhaps he tried to unsuccessfully build a stock-flow coherent model.

Also, in recent times, Post-Keynesians have come to the realisation that trade elasticities are endogenous not fixed parameters. To me that the most crucial aspect of circular and cumulative causation, although the Verdoorn Law plays a role too.

There was a recent critique of neochartalism by Costas Lapavitsas and Nicolás Aguila at the Developing Economics blog titled Monetary Policy Is Ultimately Based On A Theory Of Money: A Marxist Critique Of MMT.

Now, I don’t think that there is any Marxist theory of money, The true description of money and everything else can only be via using national accounts and the flow of funds, like Post-Keynesian stock-flow consistent models but the article has some interesting critique:

For Marxist political economy, monetary sovereignty depends on the relationship between capitalist accumulation in a nation-state and the ability to acquire world money, which in turn reflects a country’s place in the world market. The need for world money becomes clear once we consider capitalism as a global system, as it is needed for commodity transactions, the transfer of value, and the settlement of obligations among different parts of the world. The passage from the national to the international realm is a major problem for neo-Chartalist theory as there is no supranational state choosing units of account or having the power to tax at the international level.

The capacity to acquire world money necessary for participation in the world market differs dramatically among nation-states, and thus the global monetary system is hierarchically structured. In contemporary capitalism, one country, the U.S.A., issues quasi-world money, subject to competition by others. The lack of monetary sovereignty for other countries, far from being a policy choice, results from their subordinated position in the international hierarchy. This is particularly relevant for analysing economic policy in developing countries, where MMT prescriptions lose much of their appeal …

As long as countries are trading goods and assets with the external world, the acceptability of the currency is critical. Here taxing residents isn’t sufficient to make the currency acceptable to foreigners.

There’s an implicit wrong idea in neochartalism that the exchange rate adjusts smoothly to make things fine. A sort of an invisible hand sneaked in.

So unlike what neochartalists (the ones calling their theory “MMT”) say, floating the value of the currency won’t do the trick. It’s not like there’s always a price, sometimes there is no price to clear the foreign exchange market and the government might need to step in and meet the demands of investors.

Fiscal policy has a strong role to play, but ultimately exports have to rise in the long-run and fiscal policy becomes endogenous to it as Nicholas Kaldor had argued.

To make matters complicated, neochartalists also say similar things without saying that they realised these things only after they were challenged and forced to make changes. Big changes!

Thomas Palley likes to point out that neochartalism is a mix of old and new and the new is significantly wrong. The new relies heavily on claims about acceptance of currencies in the international markets. Such erroenous notions make them claim things like current account deficits are indefinitely sustainable. As long as acceptability of the domestic currency is not cast in stone, that’s of course not true.

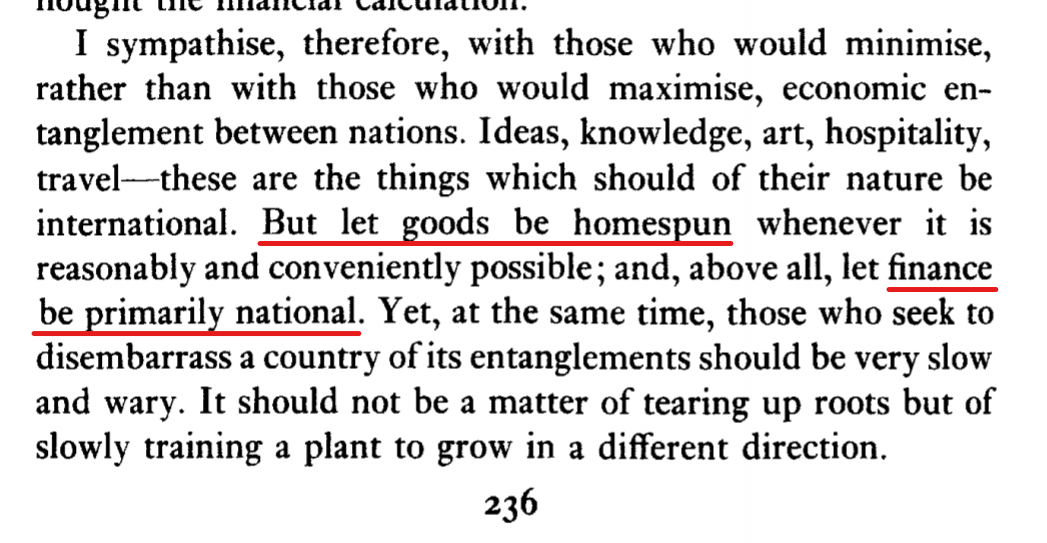

Nicholas Kaldor in Limitations Of The General Theory, published in Collected Economic Essays, Volume 9, first published 1982 on the role and importance of history in causation:

My purpose here is to show that many of the difficulties which emerged in the operation of Keynesian policies of demand management were due not to any defect in basic conception but to the failure of Keynes (and of his followers) to work out the full implications of his ‘paradigm’ of the economy as against the ruling ‘paradigm’ of neo-classical economics.

Keynes himself emphasized that the writing of his book was ‘one long struggle to escape from habitual modes of thought and expression … The difficulty lies not in the new ideas, but in escaping from the old ones, which ramify, for those brought up as most of us have been, into every corner of our minds.’3

As far is possible within the confines of a lecture, I hope to demonstrate that the limitations of the General Theory derive more from a failure to escape from traditional modes of thought than from any basic defect in those aspects which were fundamentally new. Apart from his failure to cut himself loose from one of the main tenets of the quantity theory of money, with which I shall deal only briefly as I have discussed it extensively on earlier occasions, the three main aspect in which Keynes remained too much a follower of tradition concern: first, the micro-economic background, in other words, the implications for his theory of the way markets function; second, the regional or territorial aspect, the implications of inter-regional trade for the differing rates of employment-growth of different areas; and finally, the failure to recognize that owing to the importance of increasing returns in manufacturing, the development of an industrial system is largely self-generated, where, owing to a powerful feed-back mechanism, ‘events of the recent past can only be explained in terms of the actual sequence through which the system has progressed; history enters into the causation of events in an essential way’.4

3General Theory, Preface, p. vii.

4 Cf. Jukka Pekkarinen, On The Generality of Keynesian Economics (Helsinski, 1979), p. 113. He adds that in consequence ‘it is not reasonable to view the economic process as allocating given resources wuth given technologies and preferences’.

From a Twitter discussion on balance-of-payments, I was reminded of a section of John E. King’s 2009 biography of Nicholas, titled by the name.

From pages 193‒195 (+ endnote + references in Bibliography):

Kaldor’s willingness to take extreme positions was very well illustrated by his post-1966 emphasis on exports as the only exogenous source of effective demand, which I criticised in Chapter 4, Section 7. The closely related balance-of-payments-constrained growth models seem, at first glance, to be more relevant to a (long-departed) world of fixed exchange rates than to the world we live in, with floating currencies and huge payments deficits (and surpluses) that can apparently be sustained indefinitely. Kaldor would probably have responded to this with four counter arguments. First, he would have claimed that it was true only of rich countries with currencies that were sufficiently attractive for foreigners to hold to make continuing large deficits sustainable (for example the United States, the Euro bloc, Britain and Australia). The balance of payments constraint remained binding for small, poor countries with unattractive currencies (Bolivia, Zambia, Thailand). Such countries also continued to be dependent on the IMF and the World Bank, which dictated deflationary responses to their payments deficits, including (but not confined to) devaluation. In any case, Kaldor would have insisted, the external constraint continued to operate at the regional or sub-national level: poor, relatively backward regions cannot depreciate against richer, more productive regions within their own country (this was why he had advocated the Regional Employment Premium).

Second, Kaldor would have invoked his habitual ‘elasticity pessimism’ to deny that (at least for countries with initially serious problems of international competitiveness like the United Kingdom) currency depreciation would have the stimulating effect on exports, and the dampening effect on imports, that mainstream theory dictated. In this he would have been vindicated by evidence concerning the ‘Kaldor paradox’: countries that devalued in the 1950s, 1960s and 1970s tended to lose market share in world trade, while those countries whose currencies appreciated gained in market share (McCombie and Thirlwall 1994, pp. 289–99). Third, he might well have accepted Paul Davidson’s argument that a floating exchange rate regime introduced an unwelcome element of uncertainty into the world economy, discouraging investment and slowing growth across the board, so that a return to fixed exchange rates was both possible and desirable (Davidson 2006). 13

Fourth, and decisively, Kaldor would have argued that there were two channels through which the balance of payments constraint operated, not one. In addition to the policy channel (‘stop-go’, or demand deflation in response to payments deficits), there is an automatic process through which poor export performance leads to sluggish aggregate demand and thence to low business investment and slower output and productivity growth, in the absence of any policy response whatsoever. This fourth defence hinges on the controversial proposition that, for any individual country or region, exports are the only exogenous source of demand, with investment (and consumption) being entirely endogenously determined. This is a very strong assumption, but if it is accepted, the external constraint on growth becomes binding in all circumstances, and cannot be written off as historically or geographically specific, or confined to the Bretton Woods epoch (see also McCombie and Thirlwall 1994).

…

Notes

…

Note, however, his stated belief that a return to Bretton Woods in the late 1970s would have made things worse (Kaldor 1978c, p. xxi). Not all Post Keynesians agree with Davidson on this important point, Wray (2006) for example arguing that flexible exchange rates are a necessary condition for national economic sovereignty.

…

Bibliography

…

Davidson, P. 2006. ‘Liberalization or regulating international capital flows?’, in L.-P. Rochon and S. Rossi (eds), Monetary and Exchange Rate Systems: A Global View of Financial Crises, Cheltenham: Elgar, pp. 167–90. …

McCombie, J. S. L. and Thirlwall, A. P. 1994. Economic Growth and the Balance-of-payments Constraint. Basingstoke: Macmillan.

…

Wray, L. Randall. 2006. ‘To fix or float: theoretical and pragmatic considerations’, in L.-P. Rochon and S. Rossi (eds), Monetary and Exchange Rate Systems: A Global View of Financial Crises, Cheltenham: Elgar, pp. 210–31.

Now, I do believe in this (for the present rules of the game), as it otherwise stock-flow ratios rise without limits, fixed exchange rates or floating, something King seems to be fine with!

Also, King is extremising Kaldor’s views, which are extreme nontheless—not extreme in a negative way. What’s exogenous and endogenous also changes with the time-period we’re looking at. Something which is exogenous in the short-run can be consistently thought of as endogenous in the long-run.

The latest edition of The Economist has this cover, worrying about the rise in the idea of national self-sufficiency.

Obviously, The Economist whose purpose is to promote the propaganda of free trade doesn’t like this as any country achieving self-sufficiency would mean a reduction of market share of large corporations whose interests the magazine has spoken since 1843, the year it was founded.

John Maynard Keynes wondered about national-self sufficiency too. In an article titled National Self-Sufficiency in the year 1933, which he argued:

Of course self-sufficiency is one thing, but there’s also the idea of planned trade. These two concepts are related but are potentially different.

One of the promoters of planned trade was Nicholas Kaldor. In The Role Of Increasing Returns, Technical Progress And Cumulative Causation In The Theory Of International Trade And Economic Growth, Economie Appliquée, 34(4): 593–617, 1981, he motivates the reasons for a planned trade:

At the moment the world suffers from an insufficiency of demand for industrial products which most industrial countries however are not in a position to remedy, because of the need to avoid deficits in their balance of payments. It does not follow therefore that free trade leads to the maximum development of trade: if it involves chronic imbalances it might lead to a situation in which the world economy is in a state of continued recession, which cannot be effectively counterbalanced by national policies of economic management. Most governments and economists are in constant fear lest the state of recession will lead to the haphazard introduction of protective measures to domestic industries, which on balance will cause a further shrinkage of world demand. This may well happen in the absence of a coordinated policy, but my own prescription would not be that we must stick to free trade (whatever the cost), but to introduce a system of planned trade between the industrially developing countries, so as to remove the balance of payment constraint on their internal expansion.11

Contrary to the actual policies adopted—which put trade restrictions mostly on imports from low wage developing countries—I would allow such imports freely since these countries have an unlimited appetite for manufactured imports of capital goods, which is only restrained by their ability to pay for them. Contrary to the general view, therefore, it is not the imports coming from the developing countries, but the import penetration of goods produced in developed countries which threatens major industries of other developed countries (such as the motor car industry in Britain or the television industry in the U.S.) and which requires some system of regulation of trade if we wish to remove existing impediments for the expansion of production and employment in the industrial countries of the world.12

11 The French Government in the year preceding the legislative election, under the leadership of M. Barre, advocated something similar with their slogan “Croissance ordonnée des échanges”. It is possible however that it was a temporary slogan for the sake of electoral popularity since not much was heard about these policies after the last French elections.

12 It also requires the recycling of OPEC surpluses—a function which has been performed up to now, not by official institutions such as the IMF, but mainly American private banks, operating through the Euro-dollar market. While I have no time to develop this theme on the present occasion, I think I ought to mention that I would favour as an instrument of such planning the introduction of some licensing system for imports of manufactures which is directly linked to exports, so that imports and exports are kept in some agreed balance.

Basically in the regime of free trade, the market mechanism does not bring balance-of-payments imbalances in balance. The price mechanism to keep global imbalances in check simply doesn’t work. Instead it works by putting a deflationary bias on the whole world.

Hence there is a need for using official mechanisms to keep imbalances in check without output suffering.

Imperialism and free-trade is the most important reason for why some countries are rich and others poor. Because of the principle of circular and cumulative causation, they rarely catch up. Poor countries aren’t “underdeveloped”—it’s a misleading word—they’re exploited. Hence there’s a need for global rules to allow for convergence of fortunes of nations. The current rules of globalisation lead to polarisation and welfare of a few, not the many.

I recently recommended Ha-Joon Chang’s lecture series. It’s a long one—13 lectures followed by discussions.

In the discussion part of the talk Why Are Some Countries Rich And Others Poor, Ha-Joon Chang calls for asymmetric protectionism. The global rules are in favour of poor countries and not the rich ones.

Nicholas Kaldor was proposing “planned trade” in the 70s and the 80s and also a plan to have balanced trade. So a part of planned trade would be to allow poor countries to use tariffs and quotas without the fear of retaliation by rich countries.