Marc Lavoie’s has a new bookPost-Keynesian Growth Theory: Selected Essays with a collection of his essays on some of his important papers on growth. The cover features Michal Kalecki, Nicholas Kaldor, Joan Robinson and Luigi Pasinetti. Will be out soon.

In the same series, there’s also a book from 2020 Post-Keynesian Monetary Theory: Selected Essays. You can preview the introduction to this book on Google Books. So even if you’ve read all the papers, don’t miss the detailed introduction which gives an idea of his thoughts through the years. It also has a foreword by Louis-Philippe Rochon. And an interview with him on that book.

The Nobel Prize in economics this year was given in one half to David Card for his work for showing using “natural experiments” that “that increasing the minimum wage does not necessarily lead to fewer jobs”.

The profession has taken so much time to accept this. Also, many have pointed out that it’s not accurate and the prize press release itself indicates that it is for the experimental methodology and not much for the result.

At any rate, it is ridiculous that such a thing was known in the 1930s: Michał Kalecki wrote on it. The idea that increasing wages raises unemployment is an old dogma and so proving it wrong as some “credibility revolution” (as many economists claim) is a bit ridiculous.

Anyways, the point of my post is to highlight how Michał Kalecki had not only argued that increasing wages does not necessary have a negative effect, he went on to argue that it has a positive effect. He was arguing for wages in general, not just about a law on minimum wage, but the ideas are obviously similar: wages in general or the minimum wage.

The following are two quotes from 1939 and 1971 respectively. Correct me if I am wrong if someone had said this before him.

In Essays In The Theory Of Economic Fluctuations, 1939 in Collected Works Of Michał Kalecki, Vol. I:

Final remarks

1. There are certain ‘workers’ friends’ who try to persuade the working class to abandon the fight for wages in its own interest, of course. The usual argument used for this purpose is that the increase of wages causes unemployment, and is thus detrimental to the working class as a whole.

The Keynesian theory undermines the foundation of this argument. Our investigation above has shown that a wage increase may change employment in either direction, but that this change is unlikely to be important. A wage increase, however, affects to a certain extent the distribution of income: it tends to reduce the degree of monopoly and thus to raise real wages. On the other hand, ‘real’ capitalist incomes tend to fall off because of the relative shift of income from rentiers to corporations, which lowers capitalist propensity to consume.

In Class Struggle And The Distribution Of National Income, in Collected Works Of Michal Kalecki, Volume II. Capitalism: Economic Dynamics:

… a wage rise showing an increase in the power of the trade unions leads-contrary to the precepts of classical economics-to an increase in employment. Conversely, a fall in wages showing a weakening in their bargaining power leads to a decline in employment. The weakness of trade unions in a depression manifested in permitting wage cuts contributes to the deepening of unemployment rather than to relieving it.

If you find any quotes before these dates, please let me now. Could be from Michał Kalecki himself!

There was a virtual conference recently on Michal Kalecki’s economics. The video of the talks and presentations are available at the Fundacja Lipińskiego page for it—the link above.

Great mix of history of Kalecki’s work, history of Kaleckian economics and the extreme relevance of all this.

I came across this 1932 article by Michal Kalecki, Inflation And War, in which he talked of a coordinated fiscal expansion (although he was not optimistic that politicians might do it)!

He says:

What indeed could change the situation is fiscal inflation on large scale, for instance, by the government obtaining large credits from the central bank and spending them on massive public works of one sort or another. In this case the money no doubt would be spent and this would result in increased employment (combined with an overall reduction in wage rates). However, even such an intervention could be effective only if it were undertaken in a closed economy, e.g. in the capitalist system as a whole, embracing the whole world, where there is one exchange only and no tariff barriers. If fiscal inflation is carried out on a broader scale in one country alone it must cause disturbances in the rate of exchange. A rise in local output requires increased supplies of foreign raw materials and imports as well. At the same time, together with employment domestic prices rise which restricts exports. Consequently, the balance of payments deteriorates, an outflow of gold and foreign exchange follows, and the exchange rate falls.

In general, these processes will end earlier because in expectation of their development foreign capital will withdraw and local capitalists will purchase foreign exchange thus accelerating devaluation. This, in turn, will distort the fiscal inflation process because of rise in prices of foreign raw materials will add to a general price rise until the symptoms of hyperinflation, already known from our experience, appear. Therefore, a necessary condition for fiscal inflation to be effective is an international agreement of the capitalist powers, which is, of course, totally utopian. Thus, imperialism, which is an unavoidable phase in the development of capitalism, makes the ‘inflationary’ way of mitigating the crisis unavailable.

The article in available in his Collected Works, Volume VI, pages 175-179 and was originally written in Polish.

Keynesian policy is popular again. Many fiscal hawks are now arguing for stimulus, although they want to do it only temporarily. I came across this 1976 articleMichal Kalecki: A Neglected Prophet by Joan Robinson where she argued once again for Michal Kalecki’s originality.

Robinson:

He told me that he had taken a year’s leave from the institute where he was working in Warsaw to write his own General Theory. (When his early Polish essays were published in English, it became clear that he had worked out the main points by 1933.) In Stockholm someone gave him Keynes’s book. He began to read it—it was the book that he had intended to write. He thought, perhaps further on there will be something different. No, it was his book all the way. He said: “I confess, I became ill. Three days I lay in bed. Then I thought—Keynes is better known than I am. These ideas will get across much quicker with him and then we can get on to the interesting question, which is of course the application of these theoretical ideas to policy-making. Then I got up.” Kalecki did not make any public claim to his independent discovery of what became known as Keynes’s General Theory. I made it my business to blow his trumpet for him, but I was often met with skepticism. In the US, only Lawrence Klein recognized (in The Keynesian Revolution, 1947) that Kalecki’s system of analysis was as complete as Keynes’s and in some respects superior to it.

At the end of his life Michal told me that he felt he had done right not to make any claim to priority over Keynes. It would only have led to a tiresome kind of argument. Perhaps people have been skeptical of Kalecki’s contribution to the history of economic theory precisely because he did not demand recognition himself. Such dignified behavior is rare in this degenerate age. The only reference Kalecki ever made to the question is in the preface to a selection of essays, published, alas, posthumously. “The first part includes three papers published in 1933, 1934, and 1935 in Polish before Keynes’ General Theory appeared, and containing, I believe, its essentials.”3

3Michal Kalecki, Selected Essays on the Dynamics of the Capitalist Economy, 1933-1970 (Cambridge University Press, 1971), p. vii.

There are many other by Joan Robinson where she argued this, especially this.

… a wage rise showing an increase in the power of the trade unions leads-contrary to the precepts of classical economics-to an increase in employment. Conversely, a fall in wages showing a weakening in their bargaining power leads to a decline in employment. The weakness of trade unions in a depression manifested in permitting wage cuts contributes to the deepening of unemployment rather than to relieving it.

– Michal Kalecki, 1971 in Class Struggle And The Distribution Of National Income, in Collected Works Of Michal Kalecki, Volume II. Capitalism: Economic Dynamics

Michał Kalecki in “Stimulating the World Business Upswing,” in Collected Works of Michał Kalecki, vol. 1, Capitalism: Business Cycles and Full Employment, ed. Jerzy Osiatyński, trans. Chester Adam Kisel (Oxford: Clarendon, 1990), 156–64 (possibly ahead of John Maynard Keynes):

We very often encounter the argument against building new factories while the old ones are still unemployed. This simple truism shares the fate of many of its fellows—it is false. In order for existing capital equipment to be fully employed, it must be continually expanded, since then accumulated profits are invested. If they are not invested, profits fall and, along with the fall in profits, there is a decline in the capacity utilization of existing factories.

Let us assume, as often happens in the USA, that two competing railway lines run between two cities. Traffic on both lines is weak. How does one deal with this? Paradoxically, one should build a third railway line, for then materials and people for construction of the third will be transported on the first two. What should be done when the third one is finished? Then one should build a fourth and a fifth one … This example, as we warned, is paradoxical, since unquestionably it would be better to undertake some other investment near the first two railway lines rather than build a third one; nevertheless, it perfectly illustrates the laws of development of the capitalist system as a whole.

The General Theory of Employment, Interest and Money was published in January, 1936.

Meanwhile, … , Michal Kalecki had found the same solution.

His book, Essays in the Theory of Business Cycles, published in Polish in 1933, clearly states the principle of effective demand in mathematical form. At the same time he was already exploring the implications of the analysis for the problem of a country’s balance of trade, along the same lines that I followed in drawing riders from the General Theory in essays published in 1937.

The version of his theory set out in prose (published in ‘Polska Gospodarcza’ No. 43, X, 1935) could very well be used today as an introduction to the theory of employment.

He opens by attacking the orthodox theory at the most vital point – the view that unemployment could be reduced by cutting money wage rates. And he shows (a point that Keynesians came to much later, and under his influence) that , of monopolistic influences prevent prices from falling when wage costs are lowered, the situation is still worse, because reduced purchasing power causes a fall in sales on consumption goods …

…

Michal Kalecki’s claim to priority of publication is indisputable.

– Joan Robinson, Kalecki And Keynes in Essays In Honour Of Michal Kalecki, 1964.

Jan Toporowski’s intellectual biography, volume 2 of Michał Kalecki is out now.

In the last post, Effective Demand And The Labour Market, I argued how the effect of raising minimum wages on employment is straightforward—it’s beneficial. This seems contradictory to the “intuition”—which it is not really, it’s learning to think like an economist—which suggests that raising wages will lead to unemployment.

Economists have been struggling to find answers to analysis which do not find empirical support. But they needn’t, as explanations are already available. You just need to take the Keynesian principle of effective demand more seriously.

Keynes highlighted the paradox of thrift — reduction in the propensity to consume (or rise in the propensity to save) leads to a fall in output. This goes against intuition, which considers saving as only positive. Of course the solution is to not promote a policy in which consumers spend like crazy. So fiscal policy has to be relaxed if consumers want to save a lot.

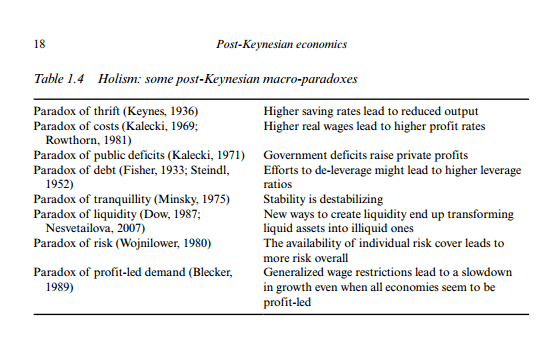

And there are other paradoxes such as the paradox of costs, which is related to the discussion on wages, profits, output and employment in the previous post. Here’s a table from Marc Lavoie’s fantastic book, Post-Keynesian Economics: New Foundations.

Marc Lavoie’s list of macro paradoxes

Intuition derived out of learning New Consensus Economics will lead one to believe that raising real wages will lead to a fall in profit rates. Michal Kalecki highlighted that this isn’t the case. As Marc Lavoie says, “what seems reasonable for a single individual or nation leads to unintended consequences or even to irrational collective behaviour when all individuals act in a similar way.”

Further, Marc Lavoie says:

The paradox of costs, in its static version, says that a decrease in real wages will not raise the profits of firms and will instead lead to a fall in the rate of employment. This was explained by Kalecki in a Polish paper first written in 1939, where he concluded that ‘one of the main features of the capitalist system is the fact that what is to the advantage of a single entrepreneur does not necessarily benefit all entrepreneurs as a class’. Its dynamic version has been proposed by Robert Rowthorn. It says that rising real wages (relative to productivity) can generate higher profit rates. This flies in the face of a microeconomic analysis that would demonstrate that lower profit margins generate lower profit rates. But if higher real wages generate higher aggregate consumption, higher sales, higher rates of capacity utilization and hence higher investment expenditures, profit rates will be driven up.

So while it may be beneficial to an individual firm to reduce wages and get a higher profit rate, it will be the reverse if everyone tries to do it.

For a fantastic discussion of these paradoxes, refer to the book Post-Keynesian Economics: New Foundations. Chapter 1 can be accessed for free at the publisher’s website.

Noah Smith asks, “Why the 101 model doesn’t work for labor markets”.

He realizes the answer but attributes it to Nick Hanauer. Smith says:

And with labor markets, it’s very hard to find a shock that only affects one of the “curves”. The reason is because almost everything in the economy gets produced with labor. If you find a whole bunch of new workers, they’re also a whole bunch of new customers, and the stuff they buy requires more workers to produce. If you raise the minimum wage, the increased income to those with jobs will also boost labor demand indirectly (somehow, activist and businessman Nick Hanauer figured this out when a whole lot of econ-trained think-tankers missed it!).

So Smith indeed concedes that the profession missed it out. But the attribution is incorrect. All this was figured out by Michal Kalecki in the 1930s.

Economists use supply-demand curves all the time without realizing that the diagram really doesn’t have time in it. Also, supply demand analysis crucially misses out the fact that supplies and demands are brought into equivalence not only because of “price clearing” but also quantity clearing. So while the supply-demand analysis is correct, it should be used more carefully.

So increases in real wages raises consumption and this leads to higher production plans which requires more labour. So because of the principle of effective demand, the reverse of what the New Consensus Economics says is true.

And also—without proof—it should be easy to see this in a stock-flow consistent model. Raise the wage rate and see the effect on output and employment. As simple!

But may be not. If say only the minimum wage is raised, although unemployment will fall in the short run, medium and long run effects can still be either way. So if fiscal policy is not relaxed, i.e., say, the growth rate of government expenditure is not increased, a rise in output will result in a rise in tax flows to the government and this may cause a slowdown in the rise of private sector wealth, resulting in a fall in output in the medium run. So fiscal policy also needs to be relaxed. Moreover, in the case of an open economy, faster rise in the wage rate may result in a fall in “price competitiveness”, and result in a fall in exports. A rise in a minimum wage in one region—say a state in the United States—may lead to a transfer of business operations to another state or even offshoring. So a global policy response is needed in the long run.

At any rate, we are far from the simplification of New Consensus Economics which starts off with a rise in unemployment due to a rise in real wage rises. The short run effect is completely the opposite.