Recently I commented on a paper, The Financial Crisis In The Eurozone: A Balance-Of-Payments Crisis With A Single Currency? by Eladio Febrero, Jorge Uxó and Fernando Bermejo, published in ROKE, Review Of Keynesian Economics. I hadn’t realised that Sergio Cesaratto has a reply (paywalled) in the same issue.

Sergio Cesaratto. Picture credit: La Città Futura, Sergio Cesaratto

Abstract:

Febrero et al. (2018) criticise the balance-of-payments (BoP) view of the European Economic and Monetary Union (EMU) crisis. I have no major objections to most of the single aspects of the crisis pointed out by these authors, except that they appear to underline specific sides of the EMU crisis, while missing a unifying and realistic explanation. Specific semi-automatic mechanisms differentiate a BoP crisis in a currency union from a traditional one. Unfortunately, these mechanisms give Febrero et al. the illusion that a BoP crisis in a currency union is impossible. My conclusion is that an interpretation of the eurozone’s troubles as a BoP crisis provides a more consistent framework. The debate has some relevance for the policy prescriptions to solve the eurocrisis. Given the costs that all sides would incur if the currency union were to break up, austerity policies are still seen by European politicians as a tolerable price to pay to keep foreign imbalances at bay – with the sweetener of some European Central Bank (ECB) support, for as long as Berlin allows the ECB to provide it.

Sergio carefully responds to all views of Febrero et al. and Marc Lavoie, Randall Wray and also Paul De Grauwe, pointing out that he agrees with most of their views except that their dismissal of this being a balance-of-payments crisis with their claims that the problem could have been addressed by the Eurosystem/ECB lending to governments without limits. He points out that, “The austerity measures that accompanied the ECB’s more proactive stance are clearly to police a moral hazard problem”. It is true that the ECB, the European Commission and the IMF overdid the austerity but it doesn’t mean that Sergio’s opponents’ claims are accurate.

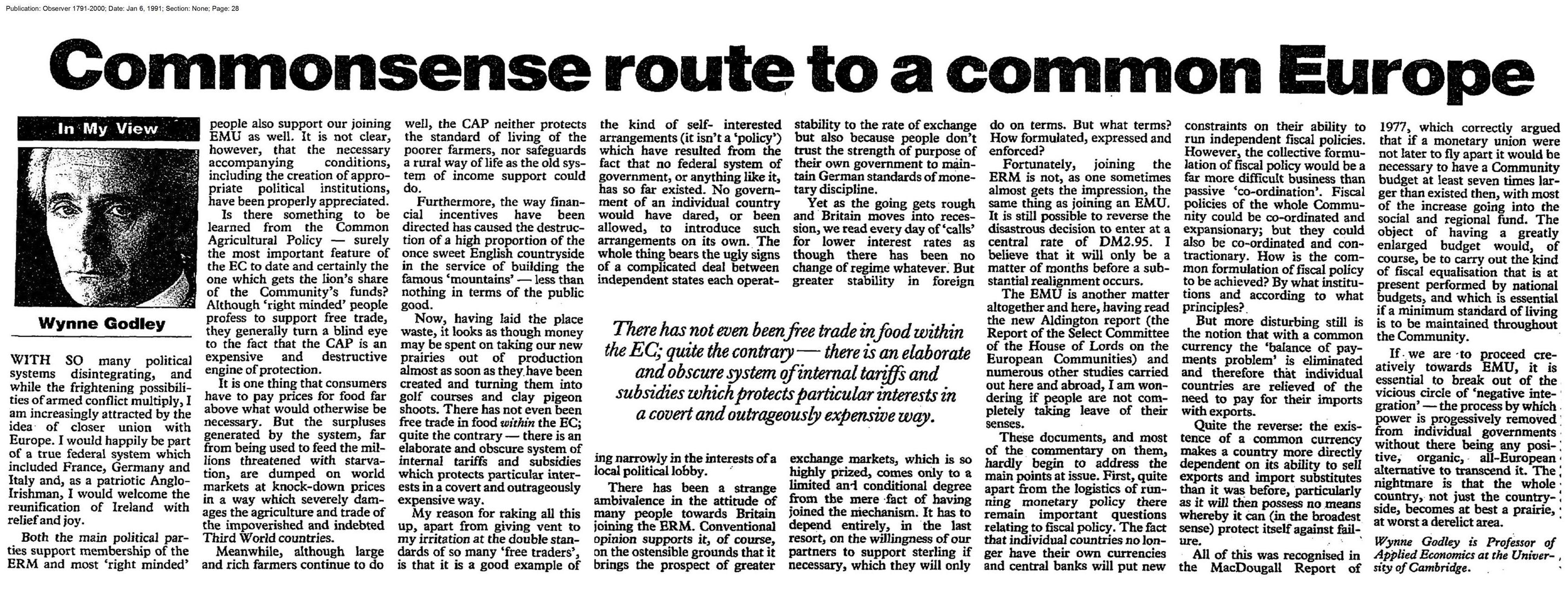

… But more disturbing still is the notion that with a common currency the ‘balance or payments problem’ is eliminated and therefore that individual countries are relieved of the need to pay for their imports with exports.

Quite the reverse: the existence or a common currency makes a country more directly dependent on its ability to sell exports and import substitutes than it was before, particularly as it will then possess no means whereby it can (in the broadest sense) protect itself against failure.

– Wynne Godley, Commonsense Route To A Common Europe, inThe Observer, 6 January 1991.

Greece had large negative current account balance of payments and Germany had the opposite over the lifetime of the Euro.

Yet, there are some economists who argue that the Euro Area crisis is not a balance of payment crisis. Of course there are other aspects to the crisis as well but this in my view is the main issue. There was a debate between Sergio Cesaratto and Marc Lavoie on this. Now there is a new paper in the most recent issue of ROKE (Review of Keynesian Economics) by Eladio Febrero, Jorge Uxó and Fernando Bermejo which discusses this. The Wayback Machine/Internet Archive link is here if you are reading it after the journal puts the paywall again.

The authors seem to be against Sergio Cesaratto view. Since I agree with Cesaratto, I thought I should comment on it.

The fundamental problem of the Euro Area is that it doesn’t have a central government. If there had been a central government like the US federal government, with large fiscal powers, the Euro Area crisis would have been far less deeper. This is because weaker regions would have been recipients of “fiscal transfers”, i.e., receive more government expenditure than what they send in taxes.

Fiscal transfers can be seen transactions in the balance of payments of Euro Area countries if the EA had a central government. The way to do balance of payments for monetary and political unions is explained in the IMF Balance of Payments and International Investment Position manual. Take a country like Greece. The Euro Area government would be considered external to Greece. Same for other countries. But for the Euro Area as a whole, the central government would be considered inside the Euro Area.

So government expenditure would appear in Greek exports in the goods and services account and transfers in the secondary income account. Taxes would appear only in the latter.

So there is an improvement in the current account balance of payments for regions compared to the case when there is no central government. Current account balances accumulate to the net international investment of the whole country. A country which has persistent imbalances would have negative net international investment position, i.e., indebtedness to other countries.

So fiscal transfers keep all this in check by improving the current account balance. So if the Euro Area had a central government, debts of a country like Greece would be in check.

By joining the half-baked half-way house, Greece got an overvalued exchange rate and easier access for other Euro Area countries into its markets and its external imbalances worsened in its lifetime inside the monetary union.

Nations with high current account deficits will also have higher public debt than otherwise and would need international investors to buy the debt which residents won’t. Normally the price would adjust to bring international investors but as we have seen, sometimes there is no price and a fall in bond prices might lead to expectations of further fall leading external investors to dump the bonds instead of finding them attractive.

The trouble with Febrero et al. is that they seem to think that the European central bank can purchase all government debt of nation. Certainly, the European Central Bank (ECB) has stepped in at various times to ease the pressure on government bond markets. But the trouble with this is that there are under some conditions such as assuming it can impose tight fiscal policy on the governments it is helping.

If the Euro Area treaty is modified to allow countries to have independent fiscal policies, then for stability, the ECB has to buy bonds without limits and can keep accumulating. It is a political mess. A country like Germany could argue that it is writing an open cheque to Greece.

A political union wouldn’t have such problems. National level governments such as the Greek government would have fiscal rules on them, and hopefully not the supranational government. This is like the United States where state governments have rules on their budgets.

In contrast, if the ECB guarantees Greece’s debt, it has to impose some rules and since Greece is not recipient of any equalisation payments—the fiscal transfers—its performance is still dependent on its competitiveness. This is because competitiveness would affect the Greece government’s fiscal balance and hence put a deflationary pressure on Greece’s fiscal stance.

On the other hand, a Euro Area with a central government would imply Greece is recipient of substantial equalisation payments and its competitiveness isn’t so binding.

An argument of the economists arguing that the European monetary system has this thing called TARGET2 and that the intra-Eurosystem balances (i.e., automatic credits offered by one national central bank to another) can rise without limit is used in this paper. This is highly misleading. It is true but one should look at the changes in debits and credits elsewhere. Suppose a country like Greece sees a large private financial outflow. While T2 can absorb a lot of this—much more than anyone imagined—in the late stages, Greece banks become heavily indebted to their national central bank, The Bank of Greece. When they run out of collateral, the rules under ELA, Emergency Liquidity Assistance, is triggered. So TARGET2 or more accurately the Eurosystem cannot absorb everything.

In summary, the Euro Area cannot do without a central government in the long run. Anyone who thinks that the ECB or the Eurosystem can buy whatever residual debt private investors doesn’t understand that in such a system, Euro Area governments are given an open cheque.

The difference between not having a central government and a central government is that in the former, there is no equivalent income flow as in the latter. The Eurosystem purchases would affect the financial account of balance of payments, not the current account.

One of the noticeable assertions of the paper is:

With T2, there is just one currency. This means that if foreign exchange markets did not exist, there could not be a BoP crisis, so that the cause of the crisis should be found elsewhere.

The trouble with this is that it sees it only as a currency crisis. But the fact is that countries whose external position were weak were the ones running into trouble in the Euro Area. Had current account deficits not blown up, countries would have had better fiscal balance since the current account balance and the budget balance are related by an identity and even behaviourally as can be seen in stock-flow consistent models. In crisis times, foreign investors are more likely to shift their funds in their home countries. With better balance of payments, public debt would be held more internally and there would have been less pressure on government bonds.

There are comments in the paper about too much credit etc. This is true, but then the Euro Area crisis would have looked more like the economic and financial crisis affected the United States.

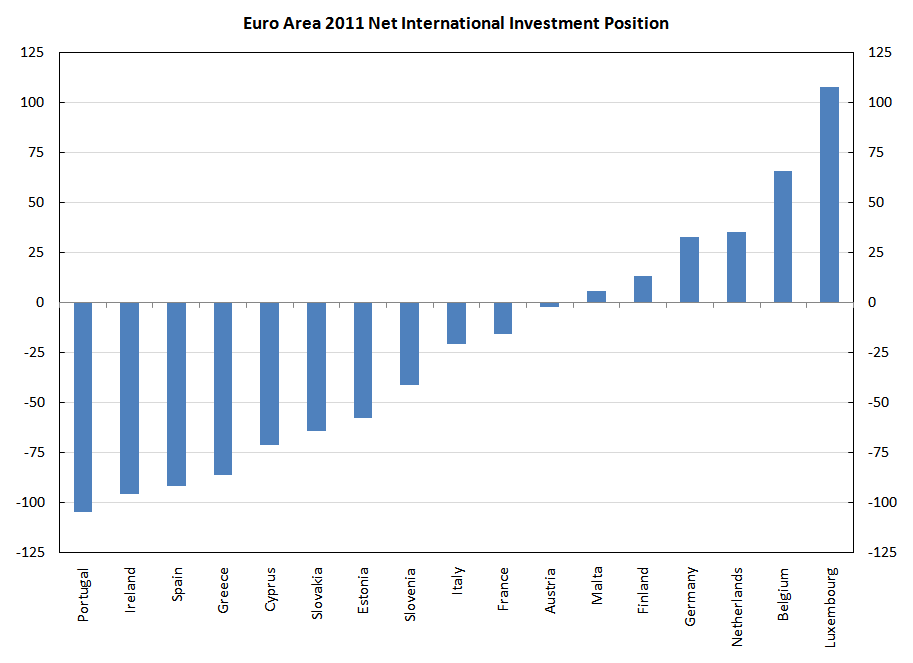

Here’s the the NIIP of Euro Area countries in 2011.

Doesn’t this explain why Germany was in a better position than Greece when the crisis started heating up? Or that Netherlands was in a better position than Portugal?

At their blog, in an article titled The Economic Scars of Crises and Recessions, the IMF is now conceding that demand affects supply and that all types of recessions lead to a permanent damage to the supply side. This is known in Post-Keynesian literature as the endogeneity of the natural rate of growth.

Earlier it was thought by them that these are temporary and the economy recovers to its pre-recession trend.

In a 2016 article for the INET, Marc Lavoie had argued how these ideas were new to the mainstream but well known in the heterodox literature.

These are not special to just recessions, as the IMF authors seem to be arguing but is happening continuously, even outside recession. The 2002 paperThe Endogeneity Of The Natural Rate Of Growth by Miguel A. León‐Ledesma and A. P. Thirlwall for the Cambridge Journal Of Economics is a great reference.

If there’s full employment, the rate of growth of GDP is equal to the rate of growth of the labour force plus the rate of growth of productivity. This is Harrod’s natural rate of growth. Unlike the natural rate of interest or of unemployment, this is not vacuous. Of course, below full employment, an economy can grow faster, although the actual rate of growth depends on demand always. We also know that the rate of growth of productivity depends itself on the rate of growth of the GDP. So that implies that the natural rate of growth is endogenous.

From the León‐Ledesma-Thirlwall paper:

The question of whether the natural growth rate is exogenous or endogenous to demand, and whether it is input growth that causes output growth or vice versa, lies at the heart of the debate between neoclassical growth economists on the one hand, who treat the rate of growth of the labour force and labour productivity as exogenous to the actual rate of growth, and economists in the Keynesian/post-Keynesian tradition, who maintain that growth is primarily demand driven because labour force growth and productivity growth respond to demand growth, both foreign and domestic. The latter view does not imply, of course, that demand growth determines supply growth without limit; rather, that aggregate demand determines aggregate supply over a range of full employment growth rates, and that in most countries demand constraints (related to excessive inflation and balance of payments disequilibrium) tend to bite long before supply constraints are ever reached.

The new issue of ROKE is out and the journal has made available Marc Lavoie and Brett Fiebiger’s article free.

Abstract:

In late 2008 a consensus was reached amongst global policymakers that fiscal stimulus was required to counteract the effects of the Great Recession, a view dubbed as the New Fiscalism. Pragmatism triumphed over the stipulations of the New Consensus Macroeconomics, which viewed discretionary fiscal actions as an irrelevant tool of counter-cyclical macroeconomic policy (if not altogether detrimental). The partial re-embrace of Keynes was however relatively short-lived, lasting only until early 2010 when fiscal consolidation came to the forefront again, although the merits of fiscal austerity were questioned when economic recovery did not really materialize in 2012. This paper traces the ups and downs of the debate over the New Fiscalism, especially at the International Monetary Fund, by analysing IMF documents and G20 communiqués. Using fiscal policy as a means to exit the crisis remains contentious even amidst recognition of secular stagnation.

Referred is also a 2016 article by Janet Yellen who makes a huge concession about the state of Macroeconomics:

The Influence of Demand on Aggregate Supply

The first question I would like to pose concerns the distinction between aggregate supply and aggregate demand: Are there circumstances in which changes in aggregate demand can have an appreciable, persistent effect on aggregate supply?

Prior to the Great Recession, most economists would probably have answered this question with a qualified “no.” They would have broadly agreed with Robert Solow that economic output over the longer term is primarily driven by supply–the amount of output of goods and services the economy is capable of producing, given its labor and capital resources and existing technologies. Aggregate demand, in contrast, was seen as explaining shorter-term fluctuations around the mostly exogenous supply-determined longer-run trend. This conclusion deserves to be reconsidered in light of the failure of the level of economic activity to return to its pre-recession trend in most advanced economies. This post-crisis experience suggests that changes in aggregate demand may have an appreciable, persistent effect on aggregate supply–that is, on potential output.

The idea that persistent shortfalls in aggregate demand could adversely affect the supply side of the economy–an effect commonly referred to as hysteresis–is not new; for example, the possibility was discussed back in the mid-1980s with regard to the performance of European labor markets.

There’s a nice new book titled, Advances In Endogenous Money Analysis, edited by Louis-Philippe Rochon and Sergio Rossi.

There’s a great chapter on Nicholas Kaldor’s views on money over the years by John E. King and another by Marc Lavoie titled, Assessing Some Structuralist Claims Through A Coherent Stock–Flow Framework. John E. King also discusses the importance of fiscal policy in Kaldor’s work:

Kaldor continued to insist on the importance of fiscal policy. The first point in his ‘constructive programme of recovery’ from the world stagflationary crisis of the early 1980s was international agreement on ‘coordinated fiscal action including a set of consistent balance of payments targets and “full employment” budgets’ (Kaldor, 1996, pp. 86, 87). Existing budget deficits, he maintained, were

largely the consequence of the low level of activity. On a ‘full employment’ basis they would show a highly restrictive picture – they would show surpluses and not deficits. Contrary to appearances, the requirement of stability is for expansionary budgets – with lower taxes and higher expenditure, and not further fiscal restriction (as is advocated, for example, by M. de Larosiere of the International Monetary Fund). (Ibid., p. 87)

International coordination was critical to the success of this strategy. Trade liberalization was not consistent with full employment: ‘under conditions of unrestricted free trade the actual volume of production and trade may in fact be considerably less than under some system of regulated trade’ (ibid., italics in the original).

The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2017 was awarded to Richard H. Thaler “for his contributions to behavioural economics”.

In his book, Post-Keynesian Economics: New Foundations, (2014), Marc Lavoie has a nice discussion/critique on what’s called “New Behavioural Economics”:

I wasn’t too excited about “agent-based models” before this, but I saw this paperWhat Drives Markups? Evolutionary Pricing In An Agent-Based Stock-Flow Consistent Macroeconomic Model by Marc Lavoie (co-authored with Pascal Seppecher and Isabelle Salle) and it got me a bit interested.

From the paper:

ABMs are conceived to analyze out-of-equilibrium dynamics and adaptation processes from heterogeneous and interacting entities … On a more specific note, we use a stock-flow consistent (hereafter, SFC) framework … there has been a multiplicity of macroeconomic models that combine two important features: the principle of decentralization/disaggregation which is found in ABM and the principle of stock-flow consistency … In an ABM, macroeconomic variables are the result of a simple process of aggregation of individual data, as in the real word [sic] …, so that the accounting accuracy provided by the SFC ensures the relevance of the aggregation process …, as well as the interconnected nature of the balance sheets of all agents. Symmetrically, AB principles could provide micro-foundations to SFC macroeconomics, that is, a way to logically articulate and rigorously organize the interactions between the micro and the macro levels.

In the last post, Effective Demand And The Labour Market, I argued how the effect of raising minimum wages on employment is straightforward—it’s beneficial. This seems contradictory to the “intuition”—which it is not really, it’s learning to think like an economist—which suggests that raising wages will lead to unemployment.

Economists have been struggling to find answers to analysis which do not find empirical support. But they needn’t, as explanations are already available. You just need to take the Keynesian principle of effective demand more seriously.

Keynes highlighted the paradox of thrift — reduction in the propensity to consume (or rise in the propensity to save) leads to a fall in output. This goes against intuition, which considers saving as only positive. Of course the solution is to not promote a policy in which consumers spend like crazy. So fiscal policy has to be relaxed if consumers want to save a lot.

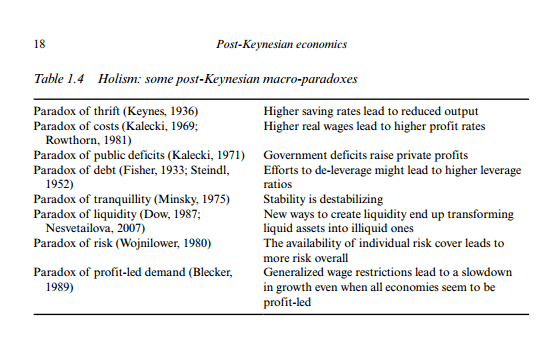

And there are other paradoxes such as the paradox of costs, which is related to the discussion on wages, profits, output and employment in the previous post. Here’s a table from Marc Lavoie’s fantastic book, Post-Keynesian Economics: New Foundations.

Marc Lavoie’s list of macro paradoxes

Intuition derived out of learning New Consensus Economics will lead one to believe that raising real wages will lead to a fall in profit rates. Michal Kalecki highlighted that this isn’t the case. As Marc Lavoie says, “what seems reasonable for a single individual or nation leads to unintended consequences or even to irrational collective behaviour when all individuals act in a similar way.”

Further, Marc Lavoie says:

The paradox of costs, in its static version, says that a decrease in real wages will not raise the profits of firms and will instead lead to a fall in the rate of employment. This was explained by Kalecki in a Polish paper first written in 1939, where he concluded that ‘one of the main features of the capitalist system is the fact that what is to the advantage of a single entrepreneur does not necessarily benefit all entrepreneurs as a class’. Its dynamic version has been proposed by Robert Rowthorn. It says that rising real wages (relative to productivity) can generate higher profit rates. This flies in the face of a microeconomic analysis that would demonstrate that lower profit margins generate lower profit rates. But if higher real wages generate higher aggregate consumption, higher sales, higher rates of capacity utilization and hence higher investment expenditures, profit rates will be driven up.

So while it may be beneficial to an individual firm to reduce wages and get a higher profit rate, it will be the reverse if everyone tries to do it.

For a fantastic discussion of these paradoxes, refer to the book Post-Keynesian Economics: New Foundations. Chapter 1 can be accessed for free at the publisher’s website.

h/t Matias Vernengo, I came across this nice short documentary Kalecki. Geniusz Zapomniany (Kalecki: Forgotten Genius) on the life of the Polish 🇵🇱 economist Michal Kalecki.

Michal Kalecki with India’s first Prime Minister Jawaharlal Nehru. Click the picture to see the documentary in a new tab.

I also came across this nice article by Marc Lavoie, Kalecki And Post-Keynesian Economics, in the book, Michał Kalecki In the 21st Century, edited by Jan Toporowski and Łukasz Mamica and published in 2015. Toporowski also appears in the documentary above.

In that article Marc Lavoie says that although the work of Kalecki is “extensive and paramount”, some Post-Keynesian authors have been reluctant to accept it. Marc Lavoie argues that it ought to not be that way and that “some post-Keynesians believe that Kalecki, rather than Keynes, provides the best foundations for post-Keynesian theory”.

The importance of national accounts and flow of funds is underemphasized by economists. It’s as crucial as calculus and real analysis is to physics. Economists confound income flows with financial flows, but matters of national accounts were kindergarten stuff for Kalecki. With such advantage, Kalecki made a huge amount of progress in his work on economic dynamics.

There’s a new book, The Palgrave Companion To Cambridge Economics which features among other things biographies of Wynne Godley, Joan Robinson and Nicholas Kaldor and other notable Cambridge economists. Wynne Godley’s biography—Wynne Godley (1926-2010)—is by his closest collaborators – Francis Cripps and Marc Lavoie (pp. 929-953)

You can access the book on Springer, if you have subscription or preview it on Google Books.

Excerpt:

One interpretation of Godley’s theoretical work is that it is a quest for the Holy Grail of Keynesianism. Keynesians of all stripes had for a long time mentioned the need to integrate the real and the monetary sides of economics. Integration was all the talk, but for a long time, little seemed to be achieved … The main purpose of the Godley and Cripps’s 1983 book is to amalgamate the real and the financial sides, providing a theory of real output in a monetary economy …

Godley believed that Keynesian orthodoxy ‘did not properly incorporate money and other financial variables’ (ibid.: 15). Godley and Cripps and their colleagues ‘found quite early on that there was indeed something deficient in most macroeconomic models of the time’, including their own, ‘in that they tended to ignore constraints which adjustments of money and other financial assets impose on the economic system as a whole’ (ibid.: 16). Interestingly, Godley was aware of the work being carried out at about the same time by Tobin and his Yale colleagues, as well as by others such as Buiter, Christ, Ott and Ott, Turnovsky, and Blinder and Solow, who emphasized, as Godley and Cripps (ibid.: 18) did, that ‘money stocks and flows must satisfy accounting identities in individual budgets and in an economy as a whole’. Still, Godley thought that the analysis of the authors in this tradition was overly complicated, in particular because they assumed some given stock or growth rate of money, ‘leaving an endogenous rate of interest to reconcile’ this stock of money with the fiscal stance (Godley 1983: 137). Godley and Cripps (ibid.: 15) were also annoyed by several of the behavioural hypotheses found in the work of these more orthodox Keynesians, as they ‘could only give vague and complicated answers to simple questions like how money is created and what functions it fulfils’. The Cambridge authors thus wanted to start from scratch, with their own way of integrating the real and the financial sides, thus avoiding these ‘tormented replies’ (ibid.) …

Ultimately, Godley’s desire to present a definitive treatise based on consistent macroeconomic accounting gave rise, nearly 25 years later, to the Monetary Economics book (Godley and Lavoie 2007a) …

{kind=link}