There will be a webinar on Aug 22nd in honour of Marc Lavoie and Mario Seccareccia. The details are available on a special Facebook page for this.

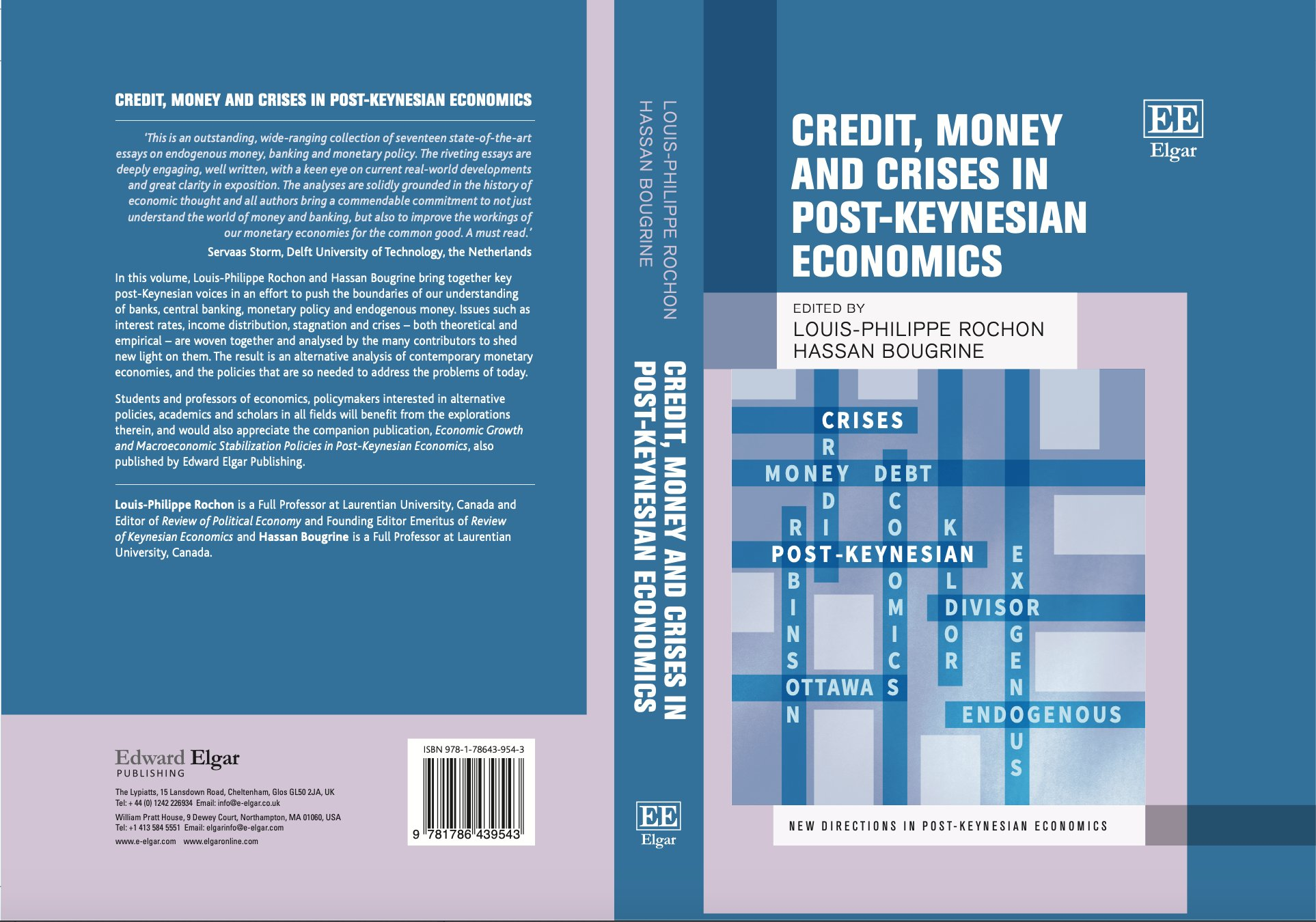

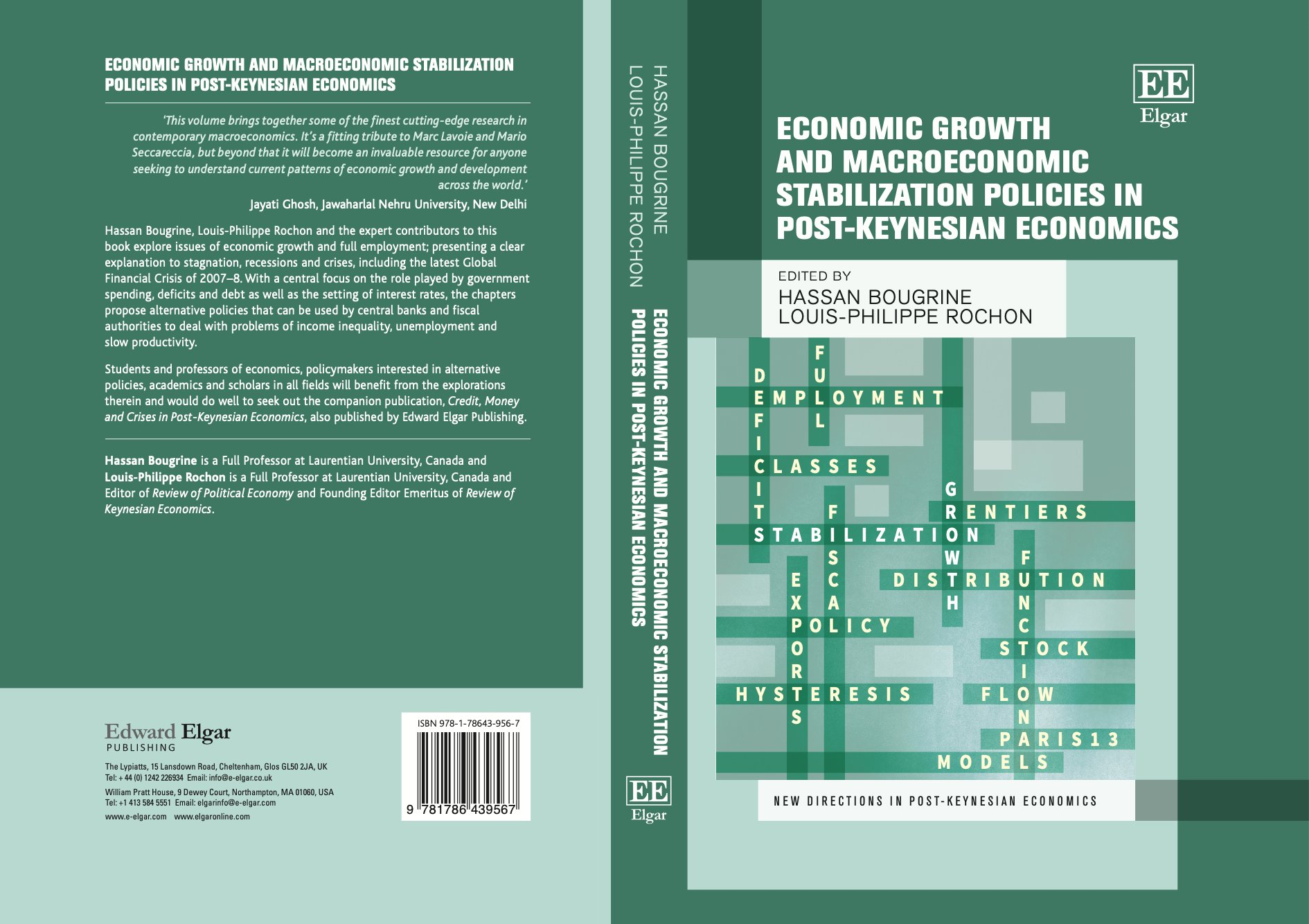

There are two volumes of essays in their honour. Links:

In addition, there’s a new book (forthcoming) with selected essays of Marc.

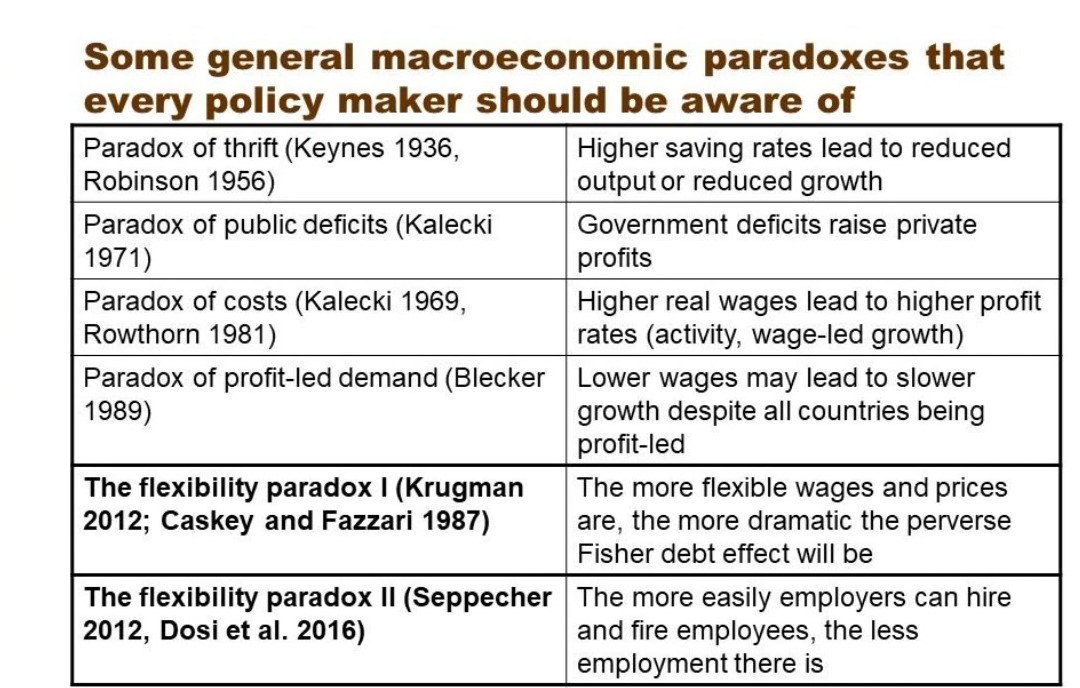

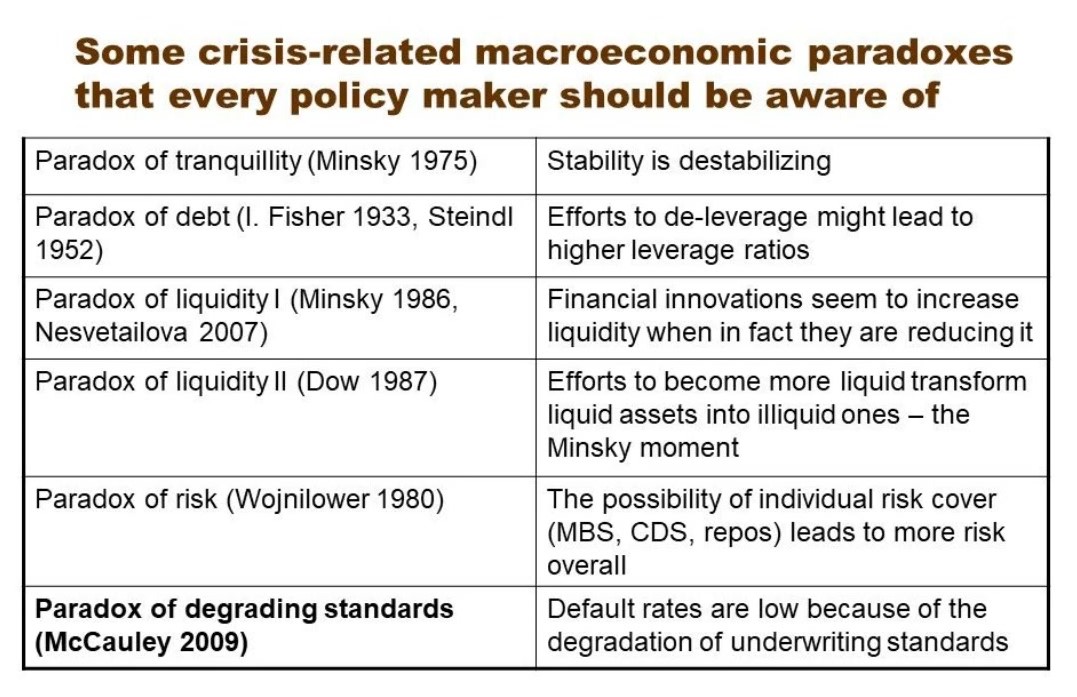

Image from Louis-Philippe Rochon