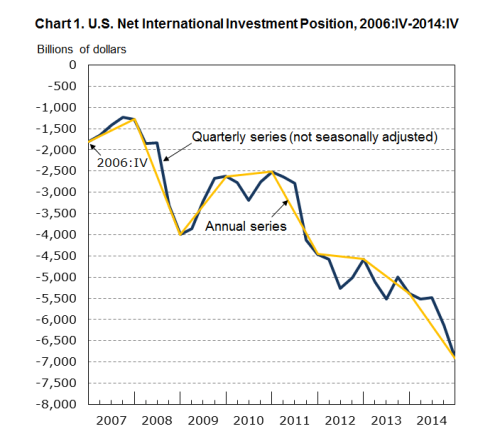

The U.S. Department of Commerce’s Bureau of Economic Analysis today released accounts for the United States’ international investment position. The U.S. is sometimes called the world’s biggest debtor and its net international investment position is now (at the end of 2014) minus $6.9 trillion.

Here’s the chart from the BEA’s website. A few points. The importance of the U.S. balance of payments and international investment position is quite neglected in analysis of the crisis. The United States’ economy went into a crisis (and the rest of the world with it) because a huge rise in private indebtedness led to a fall in private expenditure relative to income when the burden of the debt started pinching. This caused a drop in economic activity and was saved partly due to automatic stabilizers of fiscal policy as tax payments fell due to a drop in economic activity and partly due to a relaxation of fiscal policy itself by the U.S. government and governments abroad. But the huge rise in the U.S. government debt meant that resolving the crisis by fiscal policy alone would have been difficult. This is because a huge fiscal expansion would have meant that the U.S. trade deficit would have risen much faster into an unsustainable path.

See Wynne Godley’s article The United States And Her Creditors: Can The Symbiosis Last? from 2005 here arguing such things.

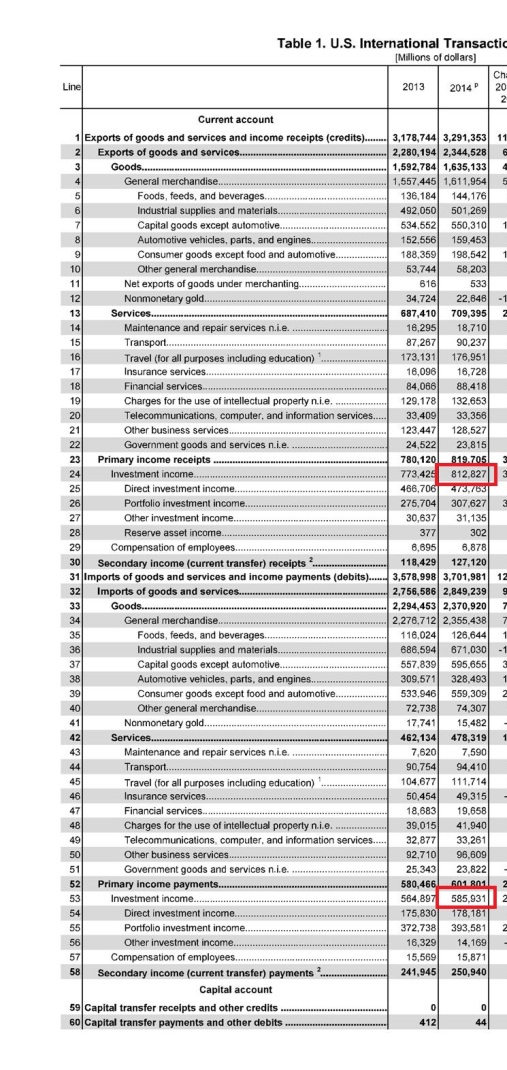

Back to the international investment position. There are a lot of interesting things about it. Although the U.S. in a huge debtor to the rest of the world, the return on assets held by resident economic units of the United States earn more than paying on liabilities to nonresidents. So according to the BEA release U.S. International transactions 2014, investment income in the full year was about $813 billion while income payments was about $586 billion. (More complication arises from “secondary income”).

In addition, revaluations of assets and liabilities also affect the international investment position and revaluations of direct investment held abroad has acted in the United States’ favour.

Of course this cannot always be the case. Take a simple example: Suppose an economic unit’s assets is $100 and liabilities is $150 and suppose assets earn 8% every year and interest paid on liabilities is 5%. So even though the economic unit has a net indebtedness of $50, it is earning

$100 × 8% − $150 × 5% = $0.5

However, if liabilities rise to $160 and beyond the net return turns negative.

In a similar way, there is a tipping point, beyond which the net primary income of the current account of balance of payments turns negative. Because the United States has a negative current account balance and the deficit adds to the net indebtedness every year, at some point in the future, the international investment position may reach a tipping point.

All this sounds as if domestic demand and output are unrelated. This is of course not the case. Imports depend on domestic demand and exports depend on economic activity abroad. Hence the constraint on output at home because if output were to rise fast, the net indebtedness of the United States will also rise fast.

Of course the concept of a tipping point may itself be misleading. Indebtedness can keep rising even if net primary income turns negative without any trouble in financial markets because it all depends on how the financial markets see the problem. But it may be said that once a tipping point is reached, the debt will start to rise much faster than now. My article here hasn’t gone into any analysis here with numbers but I will leave it for another day.

Cyprus has recently received the attention of academicians and financial professionals in recent weeks. Need I say that?

So national bankruptcy is to be resolved by winding down a bank, moving guaranteed deposits (i.e., upto €100,000) to another and as per the latest Reuters article on this, big numbers (anywhere ranging from 20 to 40 per cent loss on deposits on amounts over €100,000) are quoted.

The current plan is closer to what one would wish to see in an orderly bank resolution. Laiki Bank is to be split into good and bad banks. Deposits of less than €100,000 in the bank and assets worth €9bn – the sum owed to the central bank as part of its liquidity support – will be transferred to Bank of Cyprus. The remainder will be wound down. Those with claims to deposits in excess of €100,000 will obtain whatever the value of the bad bank’s assets turns out to be.

Meanwhile, savers at the Bank of Cyprus with deposits of more than €100,000 will have their accounts frozen and suffer a “haircut” of still unknown size. That reduction in value is likely to be large: perhaps 40 per cent. Finally, temporary exchange controls are to be imposed.

Why are the reasons for such huge numbers?

The reason is that the nation has accumulated huge net indebtedness to foreigners over years and this has been financed by banks raising deposits from foreigners, so that if debt traps are to be avoided, foreigners are to be required to take losses.

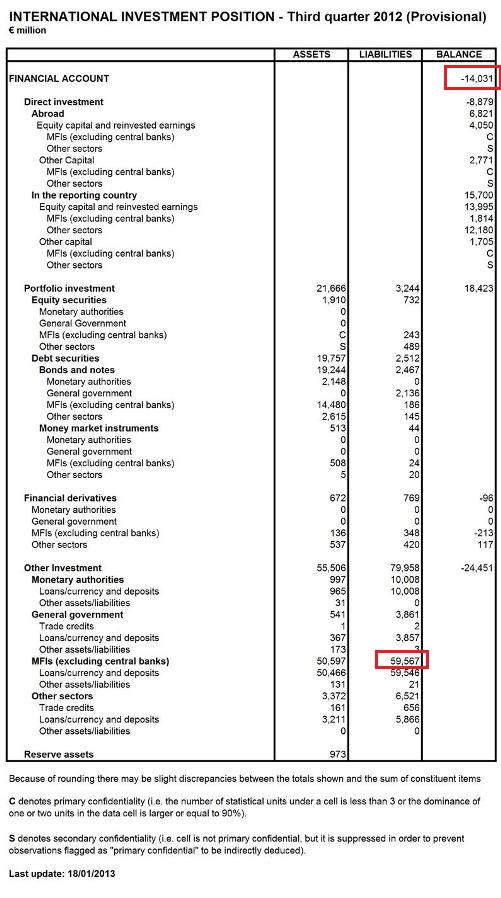

The following is the international investment position of Cyprus at the end of Q3 2012 (source: Central Bank of Cyprus)

In the balance of payments literature, banks’ position is referred as Other Investment. Also, the above refers to a Financial Accountbut it really means net IIP. Ideally it would have been better if this data had been updated but the above information is useful nonetheless.

As a percent of gdp, the net IIP position (with the opposite convention to standard usage) was 81.1% (Source: Eurostat) which is big in itself but very much lower than the now famous banks’ liabilities to foreigners/Russians! (the second red box above).

If a nation wants to resolve bankruptcy, it is better to do it by imposing losses on foreigners – especially if an international lender of last resort is available! And if this is to done it in the optimal way, best to do it once – rather than keep doing it. The ratio of two red boxes in the table – i.e., net liability as a proportion of gross bank liabilities to foreigners is 24.56%.

So Cyprus needs to wipe out about this amount as a percent of deposits roughly. It is not necessary to reach a position of zero indebtedness but something low such as 10% of gdp is ideal. Some buffer is needed because there will be leakages in spite of capital controls – requiring fire sale of foreign assets (and subsequent losses) by banks or borrowing from the ECB which may want to ensure that banks have good collateral for the ELA. Foreign deposits below €100,000 shouldn’t be hit. So “net-net”, as a percentage, this may be higher than 24.56%. All this depends on the latest situation and the distribution of foreign deposits and also the distribution between residents and foreigners but 24.56% of deposits is a good starting point – it gives a rough estimate of the order of magnitude of the problem.

At any rate, losses imposed on foreigners have to be big for the ECB and Euro Area governments to stand behind.

Here’s a new piece by Randall Wray on Economonitor claiming current accounts do not matter (once again!) and didn’t have much of a role on the Euro Area crisis. Part of his arguments are the same as those who participated in public debates 1991 (most, not all) and claimed the balance-of-payments doesn’t matter.

Perhaps he should revise his study of sectoral balances.

Before I consider his analysis, let me remind you why current account deficits matter. A current account deficit is the deficit between the income and expenditure of all resident units of an economy and because it is a deficit, it needs to be financed. Cumulative current account deficits lead to a rise in the net indebtedness of a nation (i.e., consolidated net debt of all resident sectors of an economy) and cannot keep rising forever relative to output. This is because a deficit in the current account is equal to the net borrowing of the nation which has to be financed and secondly, the debt built up needs to be refinanced again and again.

It is clear from the chart that nations with high negative NIIP (and hence high net indebtedness) were/are the ones in trouble.

The accounting identity which connects the NIIP to CAB is:

Δ NIIP = CAB + Revaluations

Most of the times, revaluations have less of a role in explaining the NIIP. Of course one can always come up with exceptions – such as for the United States with huge revaluations due to outward FDI and Ireland. It should however be noted that Ireland also had high current account deficits.

Here is data from the IMF on the current account balances:

From this you can see “Germany is not Greece”, “Netherlands is not Spain”, “Finland is not Cyprus” and so on and also the relation of CAB to NIIP.

Let me turn now to what Wray has to say:

Yesterday one presenter at this conference provided a lot of interesting data on cross border lending by European banks, most of which consisted of lending to fellow EMU members. He showed a strong correlation between cross border lending and cross border trade. Hence, posited a link between flows of finance and flows of goods and services. So far, so good. He also accepted a comment from the audience that correlation doesn’t prove causation, and that flows of finance are orders of magnitude larger than trade in goods and services—in other words, most of the financial churning has nothing to do with “real” production.

So atleast Wray accepts there is a correlation of some kind. For causation, see the arguments presented at the beginning of this post.

I won’t rehash that argument. Balances do balance, after all. For every current account deficit there’s a capital account surplus. It seems to me that the claim that the EMU suffers from “imbalances” is on even shakier ground. After all, they all use the same currency, so there’s no chance that an “imbalance” will lead to a run on the currency and to exchange rate depreciation (a usual fear following on from a current account deficit).

This argument was made by neoclassical economists around late 80s and early 90s when Europe was planning to form a monetary union. See this post Martin Wolf Pays A Generous Tribute To Anthony Thirlwall. Wray misses the point that a balance-of-payments crisis also leads to a deflationary spiral and that even though there is no exchange rate collapse, there is deflation in the Euro Area – exactly as predicted by those economists who thought the notion “current account deficits do not matter” was precisely wrong in the early 1990s.

Then Wray goes on to suggest that banks creating a boom and bust in Germany would have looked different:

Yes. But in what sense is that an “imbalance”? Look at it this way. What if instead of running up real estate prices in the sunny south—so that Brits and northern Europeans could enjoy vacation homes—the German banks had instead fueled a real estate bubble in Berlin? What if they had eliminated all underwriting standards and lent until the cows come home on the prospect that Berlin house prices would rise at an accelerating pace? Speculators from across the world would buy a piece of the bubble on the prospect that they’d reap the gains and sell-out at the peak. Construction activity would boom, workers could demand higher wages and would increase consumption, and Germany would have experienced higher price inflation than the rest of Euroland.

In the hypothetical case of Wray where German banks lend the non-financial sectors till the “cows come home”, domestic demand would have risen sharply (which he himself suggests) and this would have had the adverse effect on the balance of payments. Germany would have started running current account deficits because imports are dependent on domestic demand. Germany would have suffered similar fate but in the end it would have depended on how fast the domestic demand rose.

Wray should be careful in doing sectoral balances.

Bad bank behavior can boom or bust an economy—with or without current account deficits. And that’s pretty much what happened in Spain and Ireland (and also in Iceland).

Wray would have sounded right if he had given examples of nations having current account surpluses but from IMF’s table above it can be seen that both Spain and Ireland had huge current account deficits.

What about Iceland?

The data is from 2004-2011 and you can see that in 2008, Iceland had a current account deficit of 28.4%.

Wray then compares the Euro Area to the United States:

In Euroland, all use the same euro currency, and clearing is accomplished among the central banks and through the ECB (that is where Target 2 comes in). It works about as smoothly as the US system. But here’s the difference: the ECB “district banks” are national central banks. It is thus easier to keep mental tabs on the “imbalances” by member states in the EMU than in the USA.

Yes keeping mental tabs on imbalances (and not “imbalances”) can have its effect, but Wray crucially misses the point that in the United States, there is an automatic mechanism of compensating for trade imbalances via fiscal transfers. This acts via lower total taxes paid by regions facing slowdown caused by trade imbalances (not to be confused with lesser taxes paid due to reduced tax rates if any). A rise in public expenditure (not necessarily discretionary but resulting from government guarantees made beforehand) also helps.

Wray however quotes Mosler but he misses the point as well since it talks of directed government spending as opposed to a built in automatic mechanism which (the latter) prevents a crisis at this scale/type from happening.

Generally speaking, Wray seems to suggest that the crisis happened because the private sector credit-led boom went bust and this has nothing to do with current account imbalances. While it is true that the private sector credit-led boom ended in a bust and caused a crisis, what Wray misses is that the current account deficits contributed to exacerbating the crisis because nations in trouble built up huge indebtedness to the rest of the world and had troubles to refinance their debts. If all sectors of an economy have a consolidated net indebtedness position to the rest of the world, they will have issues borrowing and refinancing since – as a matter of accounting – foreigners have to attracted. Foreigners were unwilling because of doubts and also because there was/is a crisis in the world economy, they changed their portfolio preferences – making the whole issue of financing even more difficult.

A Digression On TARGET2

It can be argued that since the TARGET2 mechanism has a stabilizer of some sort – that since the Eurosystem TARGET2 claims arising due to capital flight from the “periphery” is an accommodative item in the balance-of-payments, current account deficits shouldn’t have been an issue.

The error in this argument is that while it is true that capital flight is automatically financed by the resultant Eurosystem TARGET2 claims and that this is helpful, it depends on the hidden assumption that banks have unlimited/uncollaterilized overdrafts at their home central banks. We have seen in various scenarios – such as with procedures such as the Emergency Liquidity Assistance (ELA) – that banks in the “periphery” can either run out of sufficient collateral needed to borrow from their home NCB or have chances to run out of collateral. They hence need to attract funds from abroad. The nation as a whole is dependent on foreigners. Current account deficits are not self-financing.

The BEA reported yesterday that the U.S. Net International Investment Position at the end of 2011 was minus $4,030.3bn. The large change compared to the end of 2010 (where it was -$2,473.6bn) was due to large revaluations of assets and liabilities in addition to the current account deficit. See the BEA blog on this.

For IIP, Foreign Direct Investments are measured at “current costs”. When evaluated at market prices, the net international investment position at the end of 2011 would have been minus $4,812.4bn. The NIIP also includes official gold holdings and if this is excluded, the net indebtedness is greater than $5T.

The following is the NIIP as a percent of GDP at market prices.

There are several reasons this by itself hasn’t worked against the U.S. The U.S. dollar is the reserve currency of the world* and secondly direct investments make huge returns for the U.S. (It should still be noted that the current account deficits bleed demand in the U.S. at a massive scale). Direct investment abroad at the end of 2011 was about $4.5tn and foreign direct investment by nonresidents in the United States $3.5T.

U.S. International Investment Position

(click to enlarge)

The direct investment abroad makes a huge killing for the U.S. as can be seen from the balance of payments. In 2011, direct investment receipts was around $480bn and direct investment payments only $159bn.

U.S. Current Balance of Payments

(click to enlarge)

*non-direct investment income is already against the United States’ favour though.

Beate Reszat has written a very nice article on TARGET2 Target2 – Q&A which should be read by anyone interested. The article seems to be in response to a speech by George Soros earlier this month in Italy. The link appears in her post and the relevant section of the transcript quoted.

Although it is a very informative article, I think the writer gives a misleading picture by disagreeing with George Soros.

For a background, the whole debate started when a German Professor Hans-Werner Sinn wrote an article The ECB’s Stealth Bailout which led to a series of attacks from academicians to bankers to central banks seriously questioning Sinn. Sinn’s arguments are full of errors but this brought into focus the TARGET2 claims of creditor nations’ NCBs and the risks that this asset may “disappear”.

Critics of Sinn learned the TARGET system and to my surprise, their description had a lot of features on money endogeneity – surprising since most of these writers err on describing one pole (of the two poles) of money endogeneity – that between banks and their central bank.

In the end, the critics claimed victory – although powerful persons such as George Soros and Jen Weidmann of Bundesbank understood and saw the situation slightly differently. Even Martin Wolf who has differences with Weidmann on the German economic strategy – rightly in my view – agrees that it may lead to losses to Germany in case of debtor nations leaving the Euro Area.

(By the way this link by Robert M Wuner has the complete list of articles on the TARGET2 debate).

While it is difficult to summarize the whole debate, the point which comes to mind is that while those who have written about the TARGET2 system in a more technically correct way (central bank articles, banks’ research publications, academicians), they are seriously misleading. Some don’t see it while – in my opinion – the Eurosystem authors see it and downplay the risks.

So here’s from Beate’s article:

If the country in question refrains from staying connected to Target2 and, at the same time, is abandoning the ECB – in my understanding (but we must ask the jurists to find out) its paid-up capital will have to be returned plus its share of profit, or minus its share of loss according to a consolidated closing balance sheet and profit and loss statement.

Now this is serious underplay. She concludes:

The way the issue of Target2 balances is discussed in public is most regrettable. The ever new records of unmanageable bilateral debt allegedly heaping up in the system arouse fears which are wholly unreasonable and stand in the way to finding a viable crisis solution. Two points should be kept in mind: Monetary policy matters such as the creation of central bank money must not be confused with the process of payment and settlement of central bank money, and intra-group payment flows as part of the normal business of the system must not be confused with profits and losses.

At closer inspection, the €2 trillion debt scenario conjured up by some observers in an utterly irresponsible way is evaporating into thin air and the euro crisis – although still a very serious problem and a big challenge – appears as one that probably can be handled.

The error in analysis such as this is that of not thinking of “money” as simultaneously as an asset and a liability.

It is best to think of the creditor nations as a whole so that the complication of “capital key” can be avoided. In my post Who Is Germany I argue that the exit of debtor members of the Euro Area will lead to losses for the creditor nations because the debtor nations will not be able to pay the Euro-denominated TARGET2 liabilities. This appears via a direct loss on the central banks’ balance sheet. And since this is a loss of the balance sheet of a nation (or a group of nations as a whole), it is plainly incorrect to argue that it does not matter or that Soros is wrong. The complication of “capital key” is a bit of a sideshow – if Germany’s losses are less than its TARGET2 claims, other NCBs lose. It is true that the Bundesbank may be capitalized by the German government – in case – but no amount of domestic transaction can change the external assets (of Germany as a whole). The fact that it is a loss to Germany can be seen by looking at the International Investment Position. If the Bundebank loses its TARGET claims, it is a loss for the whole nation. As the chapter 7 of the IMF’s Balance Of Payments And International Investment Position Manual (BPM6) says:

The IIP is a subset of the national balance sheet. The net IIP plus the value of nonfinancial assets equals the net worth of the economy, which is the balancing item of the national balance sheet.

In fact, George Soros’ argument is that since exits of debtor nations from the Euro Area will lead to serious losses to creditor nations, this has the effect of forcing the latter – especially Germany – to do something and in fact in leading them to move toward higher integration! (as a title of his recent article The Accidental Empire from Project Syndicate suggests).

To the point of Beate Reszat’s dislike for the phrase – “evaporating in thin air”, the BPM6 and the 2008 SNA use similar terminology – “appearance and disappearance of assets”!

According to a Wall Street Journal article from yesterday Cyprus Seen Close to a Request for Bailout, Cyprus (2011 GDP: €18bn approximately) is set to become the fourth Euro Area nation to seek a bailout after Greece, Ireland and Portugal. According to the WSJ:

Late last year, the country negotiated a €2.5 billion ($3.1 billion) bilateral loan from Russia. Now, Cyprus is in talks with China for another bilateral loan, of an undisclosed amount, that looks unlikely to materialize in time.

Had to go into trouble considering that economists have been realizing that the Euro Area problems is an internal balance of payments crisis.

The closest proxy for a nation’s net indebtedness is the net international investment position (as opposed to “external debt” which excludes equity held by nonresidents). Here’s the chart as of 2011: the NIIP is at the end of 2011 and the GDP is the gross domestic product for the whole year.

(click to enlarge)

Note: Greece’s NIIP improved in 2011 (from minus 100% of gdp) due to large revaluation losses suffered by foreigners as Greece financial markets fell in 2011.

The financial markets is now nervous about Spain and Slovakia’s next in the line if the graph is to be believed and it’s external position is in dangerous territory also – at minus 64%.

According to Wynne Godley, anything between 20-40% of net foreign indebtedness can be highly dangerous. Of course his models also show that there is nothing intrinsically stopping such imbalances from continuing and can go on as long as foreigners do not mind but something has to give in – such as slower growth to prevent the imbalances from continuing before foreigners start minding or a crash.

At this point, Slovakia doesn’t seem to be in trouble with its generic 10-year government bond yield at 3.645% – with its public debt at 43.3% of gdp at the end of 2011 according to Eurostat. This of course means that the domestic private sector is a net debtor (i.e., its financial assets is lesser than its liabilities). A more detailed analysis is required on how internal imbalances will play out and spill over to the external sector. Here’s from Statistical Appendix of the “Alert Mechanism Report”.

(click to enlarge)

Moving on to something different:

Heteredox Economics In Playboy!

Via Twitter:

click to view the tweet on Twitter

John Cochrane of Chicago calls heteredox economists “kooks” and claims he and his colleagues use rigorous models!

If a government (outside monetary unions) can make a draft at the central bank, why do rating agencies rate governments’ creditworthiness?

In this post, I will attempt to describe the dynamics of defaults and restructurings by going through some monetary economics of open economies.

Carmen Reinhart and Kenneth Rogoff wrote a book in 2009 titled This Time Is Different: Eight Centuries Of Financial Folly or simply This Time Is Different arguing that governments do indeed default – both in debt denominated in the domestic and foreign currencies. They blame the public debt and the government for the public debt – hence giving the innuendo that governments across the planet should attempt to cut public debt by tight fiscal policies. This is an illegitimate conclusion – on which I will say more below.

At another extreme are the Chartalists who argue that the government cannot “run out of money” and hence fiscal policy has no monetary constraints. Sometimes they qualify this statement by saying that the currency they are discussing are “sovereign currencies”. Now, there are various definitions of what a sovereign currency is but it is frequently pointed out by them that nations who have seen restructuring of government debt did not have a “sovereign currency” – because the currency is either pegged or fixed or it is the case that the government had a lot of debt in foreign currency which presumably allows defaults/restructuring of government debt in the domestic currency as well. The motivation behind this is Milton Friedman’s idea that nations should freely float their currencies in international markets and that markets will clear and that the State intervention in the currency markets can only make things worse. Hence Reinhart/Rogoff don’t prove them wrong – according to them – since the situations are supposedly different.

We will see that while there is some truth to it, the notion of a “sovereign currency” is highly misleading. Such intuitions are coincident with the incorrect notion that indebtedness to foreigners (in domestic currency) is just a technical liability and there’s nothing more to that!

Here’s S&P’s article on the methodology it uses to assign ratings on governments: Standard & Poor’s – Sovereign Government Rating And Methodology. One can see the importance it gives to the external sector. However, S&P does not provide a mechanism on how a government will finally end up defaulting. The purpose of this post is to look into this.

Before this let us make a connection between the public debt and the net indebtedness of a nation. Most people in the planet confuse the two. The former is the debt of the government whereas the latter is the (net) indebtedness of the nation as a whole. This is the net international investment position (adjusting for traditional settlement assets such as gold) with the sign reversed. This can be obtained by consolidating all the sectors of an economy and the consolidation involves (for example) netting of the assets of the domestic private sector held abroad and also its gross indebtedness to the rest of the world.

So one can think of two extremes:

Japan – with a high public debt of about 195% of gdp (includes just the central government debt), while being a net creditor of the world. It’s NIIP is about 50% of gdp (data source: MoF, Japan)

Australia – with a low public debt of 18% of gdp and NIIP of minus 59% of gdp.

So in the case of Japan, while the government is a huge debtor, the nation as a whole is a creditor, whereas in the case of Australia, it is the opposite. So the rating agencies get it wrong or opposite!

Let us first assume a closed economy. The greatest starting point in analyzing economies is the sectoral balances approach. For a closed economy it is:

NAFA = DEF

where NAFA is the Net Accumulation of Financial Assets of the private sector and DEF is the government’s budget deficit. If the private sector wants to accumulate a lot of financial assets, and the government wants to run the economy near full employment, the public debt will be higher, the higher the propensity to save, for example. (This is not as straightforward as presented here but can be shown in a simple stock-flow consistent model). So unlike what neoclassical economists think, the level of public debt is somewhat irrelevant. Neither does the government has too much trouble in financing its debt because the public debt is the mirror image of the private sector net financial asset position.

Now let us take the case of an open economy. The sectoral balances identity now is

NAFA = DEF + CAB

A deficit in the current account implies an increase in the net indebtedness to foreigners. Unless the markets miraculously clear with the exchange rate adjusting to bring the CAB in balance, a deficit in the current account implies the nation as a whole has to attract foreigners to finance this deficit i.e., via a lower NAFA or higher DEF. In the long run, the private sector is accumulating financial assets (or has small positive NAFA) and the whole of the current account balance is reflected in the public sector balance.

So the debate fixed vs floating doesn’t help too much. A relaxation of fiscal policy may spill over into higher imports with the public debt and the net indebtedness to foreigners keeps rising forever to gdp. Hence nations typically have to curb growth to bring the current account into balance.

This is theory. So let’s look at an open economy mechanism of an event of default by the government as a story.

In the following, I will use the phrase “pure float” instead of the dubious terminology “sovereign currency”.

Here’s the simplest model:

In the above, a nation with its currency on a pure float and with zero official sector liabilities in foreign currencies has a somewhat weak external position in 2012. Now, according to some of the Neochartalist arguments this nation can’t default on its government debt. However this is a wrong conclusion as the scenario above hightlights. In the scenario constructed, the balance of payments position weakens over the years (and I have mentioned that roughly in 2020 it weakens). In 2022, foreigners are no longer willing to finance the debt. This may be due to a capital flight or due to the inability of the banking system to maintain a low net open position in foreign currency. The depreciation of the domestic currency isn’t sufficient to clear the fx markets and the official sector (either the central bank or the government’s treasury) necessarily has to intervene in the foreign exchange markets by issuing debt denominated in foreign currency. The government is then acting as the borrower of the last resort and the objective is to use the proceeds to partially have more foreign exchange reserves and/or to sell the foreign currency proceeds from the debt issuance to clear the fx markets. The government is then left with a net liability position in the foreign currency. Soon the external situation worsens to the point requiring official foreign help – such as from the IMF – which promises to help and requires a restructuring of the debt both in domestic and foreign currencies.

Free marketers have a blind belief in the markets and the theories are built on the assumption that markets always clear. The recent crisis has highlighted that this isn’t the case. Even for the case of Australia – whose currency can be considered closed to being pure float – has had issues in the external sector and the Reserve Bank of Australia had to borrow in US dollars from the Federal Reserve (via swap lines) to help Australian banks meet their foreign currency funding needs during the crisis.

Of course the above is not typical but to prevent the external vulnerability to go out of control, governments keep domestic demand low and a lot of times, they over-do this.

The point of the exercise is to prove that it is not meaningless to think of nations becoming bankrupt in whichever situation one can think of and it doesn’t help to laugh at the rating agencies and make fun of them – possibly with the exception for the case of Japan. Statements such as “government with a sovereign currency cannot become bankrupt” are simply misleading. In the above, the Chartalists would argue that the currency was not sovereign and they were not wrong about the default but the currency was sovereign in their own definition in 2012!

Here are some comments on some nations.

Japan: As mentioned above, Japan is a net creditor of the rest of the world and partially as a consequence of that, most of the Japanese government’s debt is held internally. The rating agencies are aware of this but in spite of this continue to make comments on the creditworthiness of the Japanese government. It is possible that residents may transfer funds abroad for unknown reasons (which the raters for some reason suspect) but it may require just a minor interest rate hike to prevent this from happening. Japan has a relatively strong external situation and hence has no issues in financing its government debt.

Canada: Nick Rowe of WCI mentioned to me on his blog that worrying about the balance of payments constraint is like “beating a dead horse” – citing the example of Canada which has floated its currency and it seems has no trouble with its external sector. But this ignores other things in the formulation of the problem. Canada is an advanced nation and an external situation which is not weak. However, a growth of the nation much faster than the rest of the world will lead to a worsening of the external situation. To some extent the nation’s external situation has been the result of its relatively better competitiveness of exporters compared to its propensity to import and a demand situation which either as a conscious attempt of demand management of the government or by pure fluke has helped its external situation remain non-vulnerable.

United States: The US dollar is the reserve currency of the world and slowly over time, the United States has turned from being a creditor of the rest of the world to becoming the world’s largest debtor nation. (Again not due to its public debt but because of its net indebtedness to foreigners). The US external sector is a great imbalance and any attempt to get out of the recession by fiscal policy alone will worsen its external situation leading to a crash at some point. S&P is right! So to come out of the depressed state, the nation has to complement fiscal expansion with improvement of the external situation such as by (and not restricted to) asking trading partners to not revalue their currencies. Still for some reasons bloggers at the “New Economic Perspectives” think that

… Bernanke also knows that the US has infinite ability to finance these fiscal components, that there is no solvency issue and that the policy rate and both ends of the yield curve are under the direct control of the Fed.

Back to This Time Is Different. While Reinhart and Rogoff’s analysis of government debt may be useful, their conclusions can be destructive for the world as a whole. The domestic private sector of a nation needs continuous injection from outside so that it can run surpluses in general and tightening of fiscal policies will lead to a depression. Global imbalances is crucial in understanding the nature of this crisis (and not public debt alone) and even coordinated attempts to reflate economies may provide only a temporary relief. Since failure in international trade restricts the growth of nations and their attempts to reach full employment, what the world needs is an entirely different way to run the economies under managed trade with fiscal expansion. Ideas of “free trade” such as that outlined here by Alan Blinder simply help some classes of society at the expense of others because it relies on the “market mechanism” which has failed over and over again.

This brings me to “sovereignty”. As argued, the concept “sovereign currency” is almost vacuous (except highlighting the problems of the Euro Area) but sovereignty as argued by Wynne Godley in his great 1992 article Maastricht And All That and by Anthony Thirlwall in the same year on FT (my post on it here Martin Wolf Pays A Generous Tribute To Anthony Thirlwall) definitely have great importance. Some of Thirwall’s concepts of economic sovereignty in the article were: the ability to protect and encourage strategic industries, the possibility of designing systems of managed trade to even out payments imbalances, the ability to protect against certain countries with persistent surpluses, differential taxes which discriminate in favour of the tradeable goods sector.

My last post was on U.S. net income payments from abroad and how it continues to be in the favour of the United States. The late Wynne Godley had been analyzing this since 1994. In an article titled U.S. Trade Deficits: The Recovery’s Dark Side?, written with William Milberg, he had a section called “Foreign indebtedness and the foreign income paradox” where he said:

So far, the practical consequences of the United States having become “the world’s largest debtor” have not been all that significant… But it would be an error to suppose that, because the net return on net assets has been negligible in the recent past, the same thing will be true in the future…

… Why did the net foreign income flow remain positive for so long after 1988? In order to understand this apparent paradox, it is essential to disaggregate stocks of assets and liabilities and their associated flows, and to distinguish (in particular) between financial assets and direct investments… The reason that net foreign income remained positive for so long can now be understood (at least up to a point) by making a comparison of the flows shown in Figure 3 with the stocks shown in Figure 2. The net inflow that arises from direct investment has been roughly equal to the net outflow on financial assets in recent years, even though the stock of financial liabilities has been about five times as large as the market value of net foreign investments. In other words, the rate of return on net direct investments far exceeded the rate on net financial liabilities

Figure 2 referred to is below:

and Figure 3:

which is what I redrew with updated data in my previous post. But as we saw the net income payments from abroad continues to be positive (!!) even till date but the reason is similar. Foreign direct investment in the United States has risen to $2.8T at the end of 2011 as per Federal Reserve’s Z.1 Flow of Funds while U.S direct investment abroad rose to $4.8T – significantly higher (even as a percent of GDP) than in the mid-90s.

The net direct investment has seen huge returns (both via income and holding gains) and so this killing has brought in good fortunes for the United States. Of course with the whole current account of balance of payments in deficit, the external sector bleeds the circular flow of national income in the United States and contributes to weak demand there.

So a current account deficit is bad for the United States but financing this deficit has been easy for the United States given that the US Dollar is the reserve currency of the world. Why do nations require reserve assets? The late Joseph Gold of the IMF gave a nice description in his book Legal and Institutional Aspects of the International Monetary System: Selected Essays:

click to view on Google Books

What makes the US dollar the reserve currency of the world is difficult to argue. However it cannot be taken for granted that the United States may enjoy this exorbitant privilege given that the Sterling was once the darling of the financial markets and central banks.

Their argument is similar – direct investments have made huge returns for the domestic private sector of the United States and gives a good account of the external sector. Here’s a graph of the United States’ net international investment position using data reported by the Federal Reserve’s Z.1 Flow of Funds Accounts as well as the BEA’s International Investment Position:

Why the difference is a topic for another post. I don’t know it yet. Gourinchas and Rey have some answers. The Federal Reserve’s data is till 2011 end and quarterly (and seasonally adjusted) while BEA data is yearly and available till 2010.

So, from the graph above, the United States became a net debtor of the world around 1986. The indebtedness has been rising mainly due to the huge current account deficits the nation manages to run and is partly offset by “holding gains”.

Here’s a graph of the current account deficit plotted with other “financial balances” (since they are related by an identity)

By the way, the U.S. was a creditor of the world when the Bretton Woods system of fixed exchange rates collapsed. Some authors describe this collapse by saying that money has become fiat since 1971 – whatever that means!

Gourinchas and Rey point out – correctly in my opinion:

The previous discussion points to a possible instability, even in an international monetary system that lacks a formal anchor. The relevant reference here is Triffin’s prescient work on the fundamental instability of the Bretton Woods system (see Triffin 1960). Triffin saw that in a world where the fluctuations in gold supply were dictated by the vagaries of discoveries in South Africa or the destabilizing schemes of Soviet Russia, but in any case unable to grow with world demand for liquidity, the demand for the dollar was bound to eventually exceed the gold reserves of the Federal Reserve. This left the door open for a run on the dollar. Interestingly, the current situation can be seen in a similar light: in a world where the United States can supply the international currency at will and invests it in illiquid assets, it still faces a confidence risk. There could be a run on the dollar not because investors would fear an abandonment of the gold parity, as in the 1970s, but because they would fear a plunge in the dollar exchange rate. In other words, Triffin’s analysis does not have to rely on the gold-dollar parity to be relevant. Gold or not, the specter of the Triffin dilemma may still be haunting us!

Gourinchas and Rey’s arguments depend on estimating a tipping point – the point where the net income payments from abroad turn negative. This of course depends on various assumptions but let us look at it.

The gross assets of the United States held abroad and liabilities to foreigners keep changing as the nation is able to increase its liabilities and use it to make direct investments abroad. The reserve currency status has provided the nation with this privilege as central banks around the world are willing to hold dollar-denominated assets. The positive return (as well as revaluation gains from the depreciation of the dollar – when it depreciates) helps reduce the net indebtedness but the current account deficit contributes to increasing it.

The following is the graph of gross assets and liabilities – using the Federal Reserve’s Z.1 Flow of Funds Accounts data and also BEA’s data for the ratio:

So assuming assets held abroad A make a return rA and liabilities L to foreigners lead to payments at an effective interest rate rL income payments from abroad will turn negative whenever

rA · A − rL · L < 0

So A and L are changing due to the current account deficits and revaluation gains on assets and liabilities. Meanwhile, the effective interest rates are themselves changing in time because of various things such as short term interest rates set by the central banks, market conditions, state of the economy etc. Also, if the private sector of the United States makes more direct investments abroad, this will contribute to increase rA (if successful) and the process can go on with net income payments from abroad staying positive for longer. The tipping point is defined by Gourinchas and Rey as the ratio L/A beyond which the the net income payments turn negative. According to their analysis (based purely on historical data), this is 1.30.

If the net income payments from abroad turns negative, international financial markets and central banks may start suspecting the future of the exorbitant privilege according to the authors. Of course, it may be the case that even if it turns negative, the United States’ creditors don’t mind – this has been the case of Australia. The following is from the page 18 of the Australian Bureau of Statistics release Balance of Payments and International Investment Position, Australia, Dec 2011 and in their terminology – which is the same as the IMF’s – it is called “net primary income”)

(Australia’s Q4 2011 GDP was around A$369bn for comparison) and the above graph is quarterly.

So, to conclude the process can continue as long as foreigners do not mind. It shouldn’t be forgotten however that Australian banks had funding issues during the financial crisis and the RBA used its line of credit at the Federal Reserve via fx swaps to prevent a run on Australian banks and it is difficult to design policy without keeping in mind the possibility of walking into uncharted territory.

Once net primary income turns negative, the process can quickly run into unsustainable territory due to the magic of compounding of interest unless the currency depreciates in the favour of the nation helping exports. Else demand has to be curtailed to prevent an explosion but this hurts employment. Other policy options include promotion of exports and asking trading partners to increase domestic demand by fiscal expansion.

This is the first part of a series of posts I intend to write on the “rest of the world” accounts in National Accounts. This blog is about looking at economies from the point of view of National Accounts, Cambridge Keynesianism and Horizontalism. While various descriptions of balance of payments exist, most of them simply end up making money exogeneity assumption somewhere in the description!

In my view a careful description of balance of payments offers great insights on how economies work and what money really is. It is impossible to understand the success and failures of nations without understanding the external sector.

A description in terms of stocks and flows is the most appropriate for macroeconomics. Fortunately, national accountants have a good systematic approach to this.

Consider the following transaction: a government (or a corporation) raises funds in the international markets. The buyers can be residents as well as non-residents. The currency of the new issuance can be domestic as well as foreign. Does this by itself increase the net indebtedness of the nation as a whole?

The answer is No, and can be a bit surprising to the reader because the answer is the same whether the currency is domestic or foreign. The trick in the question is that an issuance of debt increases the assets and liabilities of the issuer!

(Note: the question was about the transaction, not on what happens after this)

Gross assets and liabilities vis-à-vis the rest of the world can be a bit more complicated and we need a more systematic analysis.

Consider another transaction. A government is redeeming a 7% bond with a notional of 1bn with semi-annual coupons. How much does the net indebtedness of the country change? Assuming that all the lenders are in the rest of the world sector, the net indebtedness changes by 35m. Does not matter if the currency is domestic or not. Why 35m? Because the semi-annual coupon has to be paid on redemption and the coupons are interest payments and this is recorded in the current account and this increases the net indebtedness. The principal payment cancels out the earlier liability – the bonds.

So between the start and the end of the period, foreigners earned 35m and this increased the net indebtedness of the nation who paid the interest. Of course there are other transactions which can cancel this out.

In another scenario, if all the bond holders were residents, the net indebtedness does not change – whether the bonds were in domestic currency or not.

The above was about financing. What about imports and exports? Exports provide income to a nation or a region as a whole and imports are opposite. If a nation is a net importer (more appropriately running a current account deficit), this means its expenditure is higher than income. When expenditure is higher than income, this has to be financed and this is via net borrowing.

There is one important point worth stressing. Many people – including many economists (most?) – treat liabilities to foreigners in domestic currency as not really a liability at all – at least the government’s liabilities. The reason provided is that while usually the government is forbidden from making an overdraft at the central bank or have limited powers in using central bank credit, it can end up making a higher use of it than the limits allowed – in extreme conditions. This in my opinion, is a silly intuition.

While it is true that the governments of most nations (with exceptions such as the Euro Area governments) can make a draft at the central bank and this offers the government protection to tide over extreme emergencies, the government has to directly or indirectly finance the current account deficits and this can prove unsustainable. Despite this there is an advantage in having indebtedness to foreigners in the domestic currency because:

An indebtedness to foreigners in domestic currency prevents revaluation losses on the debt if foreigners continue holding the debt and if the currency depreciates against foreign currencies. If the debt is denominated in a foreign currency and if it depreciates, more income needs to be earned from abroad to service the principal and interest payments.

The discussion can be confusing because of the relative ease with which the United States has managed till now to finance its current account deficits because the US dollar is the reserve currency of the world and continues to do so and the holders are willing to accept liabilities of resident sectors of the United States, especially the government’s at low interest rates/yields.

James Tobin, who has provided the best description of the meaning of government deficits and debt said this in an article “Agenda For International Coordination Of Macroeconomic Policies” (Google Books link)

Nonzero current accounts must be financed by equivalent capital movements, in part induced by appropriate structure of interest rates.

We will discuss this further in many posts and for now here’s a good illustration of how the balance of payments accounts are kept. This is from the Australian Bureau of Statistics’ manualBalance of Payments and International Investment Position, Australia, Concepts, Sources and Methods, 1998

(click to enlarge)

So, one starts out with the international investment position and records the transactions in the current account and the financial account. The difference is that the former records income/expenditure flows while the latter records financing flows. The current account includes items such as imports, exports, dividends, interest payments paid to/received from non-residents etc., while the capital account records transactions such as residents’ purchases of assets abroad, increase in liabilities to non-residents and so on. Since debits and credits equal, the balances in the two accounts cancel out. To calculate the international investment position, we add the financial account flows and calculate revaluations to reach the end of period international investment position.

The international investment position records assets and liabilities vis-à-vis the rest of the world. If the difference – the NIIP – is negative, it means the nation is a debtor nation. In the construction above, all transactions between residents and non-residents are recorded – whether in domestic or foreign currency. The numbers are then converted to the domestic currency according to the best rules prescribed by national accountants.

We will look into these in more detail – including all causalities of course – in later posts in this series. Till then, the summary is: imports are purchased on credit.

Found this graph at this hilarious blog which quotes Diapason Research. The graph plotted by the researchers uses cumulative current account balances from IMF’s data. I instead directly used the Net International Investment Position at the end of Q3 2011 from Eurostat.

The blue bars plot the net indebtedness of each EA17 nation (with signs reversed) and the red line is cumulative from left to right. It does not sum to zero because the Euro Area as a whole is a net debtor of the rest of the world.

The indebted European nations owe their creditors €2.2tn – which is almost 40% of the gdp of these nations as a whole.

An alternative way to plot the NIIP- in ascending/descending order as a percent of gdp. Readers of the Concerted Action blog will know that I love the NIIP! I just found a nicer way to plot this. The alternative graph is below: