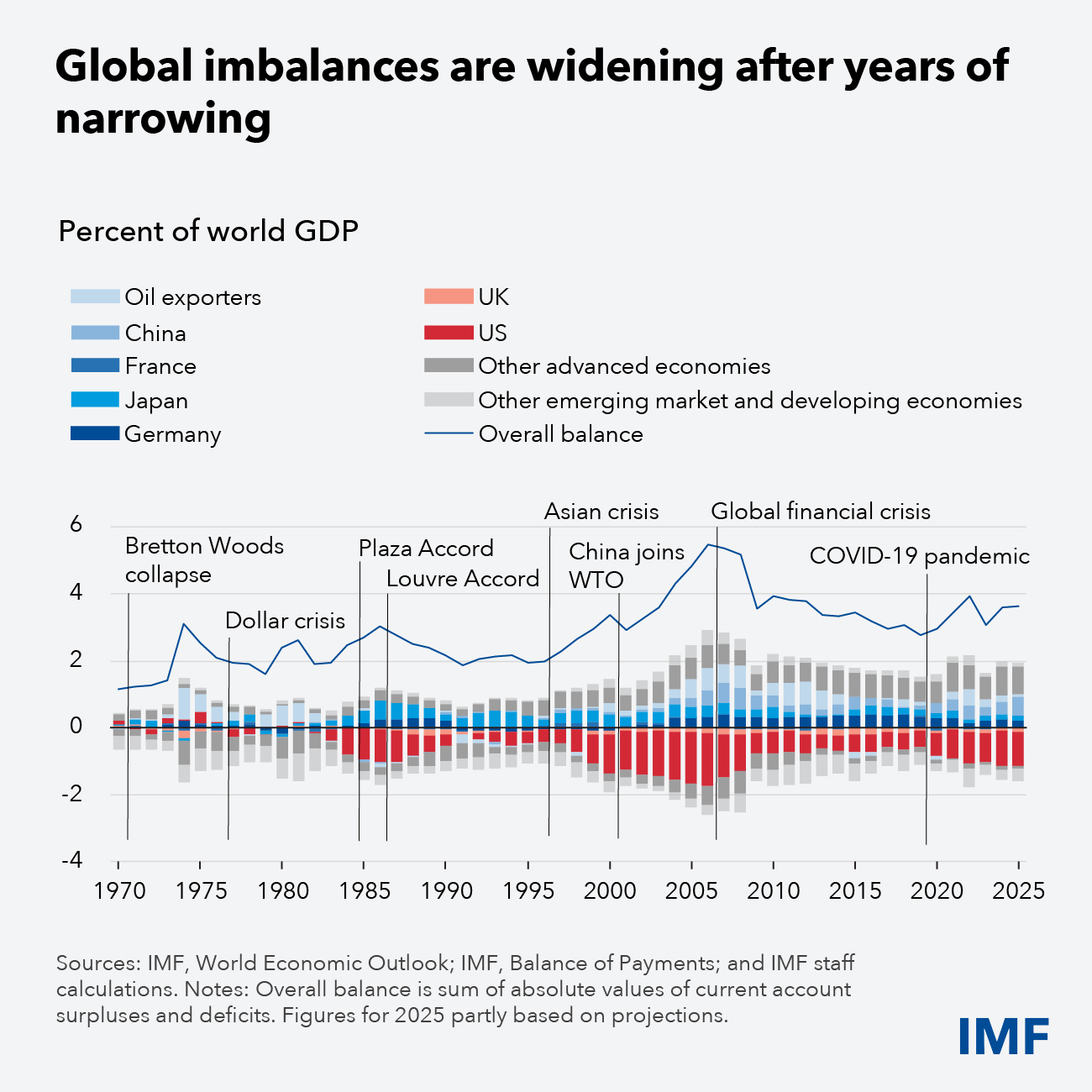

A few days ago, the IMF wrote about global imbalances, with this chart:

Source: IMF

The IMF’s analysis uses the identity:

S − I = DEF + CAB

where S is private sector saving, I is capital formation (investment), DEF is the government deficit, and CAB is the current account balance.

You can move the government deficit term to the left-hand side, with S and I now denoting the saving and capital formation of the whole country:

S (national) − I (national) = CAB

And just reasoning from the accounting identity, it concludes that, to improve the current account balance, saving has to be raised—and that this should be done via fiscal tightening.

Ugh.

Although it is fascinating that the IMF is at least acknowledging that there is a problem!

However, the IMF’s solution is ridiculous:

This synchronized adjustment would lead to the best outcome for the global economy. The economic drag from US fiscal tightening would be offset by stronger demand from China and Europe. But even if such coordination proves difficult, the best course of action for each country is clear: start addressing domestic imbalances now, regardless of what others do.

The IMF understands that fiscal tightening would slow down the US economy, so it is calling for coordination with China and Europe, which would require them to pursue fiscal expansion. But it is still proposing fiscal tightening even if others do not cooperate, on the assumption that this would pressure them.

There is no guarantee that this would work—it could instead lead to a worldwide recession.

Instead, we should abandon these dogmas and work toward a plan like Keynes’ proposal (without any Bancor), where countries with current account deficits can use import controls and industrial policy, while surplus countries relax import controls and provide assistance to deficit countries. In extreme cases where they fail to rebalance, they should pay penalties to the rest of the world.

Under such a change in the international order, fiscal tightening is not required per se.