Some bonds of the Greek government mature on March 20. The total principal amount is €14.5bn.

The focus in the financial markets is what will happen to these securities and everyday we read about negotiations with the creditors on “private sector involvement (PSI)”. For the latest see this WSJ article Greece Private-Sector Creditors Meet in Paris.

Brokers estimate that of the 14.5 billion euros of these bonds outstanding, the largest holder is the European Central Bank, which bought these securities in 2010 at a price of around 70 cents in an early, ultimately futile attempt to boost Greece’s failing bond market. The brokers say that 4 billion to 5 billion euros of bonds are owned by hedge funds at an average cost of around 40 cents to 45 cents, with some of the larger positions being held by funds based in the United States that have large London offices.

Let us look at what may happen as far as the Eurosystem is concerned on March 20. Let’s assume that the Eurosystem holds €10bn of the maturing issue – €3bn each by De Nederlandsche Bank and the Bank of Greece and €4bn by the European Central Bank. And that the remaining €4.5bn are held by hedge funds.

Let’s assume that the hedge funds will be paid 15 cents for every € of bond held and are issued new restructured debt securities – i.e., €675m (Plus what about the final coupon payment?)

Question: Where does Greece get the €10.675bn from?

The ECB is opposed to losses on the Eurosystem’s holdings as per this Bloomberg report from today so it may get a preferred creditor status.

The Eurosystem and the Greek government cannot roll the debt as it will violate the Treaty. So some official creditor or a group of creditors (EFSF?) will have to purchase €10bn+ of bonds from the Greek government before March 20 who will then pay €3bn each to the De Nederlandsche Bank and the Bank of Greece and €4bn the European Central Bank (plus coupons) on March 20 who will then later purchase the bonds from the group of official creditors!

The same holds even if the Eurosystem takes some loss.

On 28 December 2011, the Eurosystem conducted a large 3-year LTRO (Longer-Term Refinancing Operation) in which banks in the Euro Area bid about €489bn. I covered this in my post Today’s Eurosystem LTRO and I wrote that the LTRO was to help banks meet their funding needs and that they participated in it to roll over existing debt to the financial system excluding the Eurosystem.

My post had some responses having some issues with this but today the ECB released its January Monthly Bulletin which has a section on the bidding behaviour (page 30 of the pub, 31 of the pdf) confirming this:

(click to enlarge)

Some remarks can be made regarding the bidding behaviour in the three-year LTRO. First, the large amount of liquidity obtained by euro area banks in this operation can be viewed as a reflection of their refinancing needs over the coming three years, as shown in Chart A. Measuring the rollover needs over a shorter horizon, for instance over the next six months, even though it captures the large amount of refinancing needed in the first half of 2012, does not fully explain the bidding behaviour. This suggests that medium-term funding considerations may have had a significant influence on the bidding behaviour. Indeed, in addition to assessing the rollover risk faced by banks, it is useful to consider the residual maturity of banks’ outstanding debt. The longer the residual maturity, the lower the risk that banks will need to seek market funding under unfavourable conditions. Chart B illustrates a clear negative relationship between the size of the bids and the residual maturity of the bidders’ debt. This also suggests that funding considerations may have played a major role in determining the bidding behaviour. Second, banks may have placed relatively high bids in the first three-year LTRO as they viewed the operation as attractively priced compared with the prices that could be inferred from the EURIBOR swap curves or the spreads required by the market for bond issuance in 2011.

Overall, the analysis suggests that funding considerations played a major role in the bidding behaviour of banks in this first three-year LTRO, supporting the Governing Council’s view that the announced measures will help to remove impediments to access to finance in the economy, stemming notably from spillovers from the sovereign debt crisis to banks’ funding markets.

In the press conference following the ECB Governing Council decision on monetary policy (to keep the short-term rate targets unchanged), Mario Draghi mentioned that

Let us not forget that in the first quarter of this year, more than €200 billion of bank bonds fall due. So this decision certainly prevented a potentially major funding constraint for our banking system, with all the negative consequences this might have had on the credit side.

Without the LTRO, banks would have faced pressures to redeem maturing obligations by asset sales which could have led to a fall in asset prices, and if the assets were government bonds, it would have increased risks of a self-fullfilling prophecy.

On 8 Dec, the European Central Bank announced that it will conduct two Longer-Term Refinancing Operations (LTRO) with a maturity of 36 months – one each in December and February. According to the initial press release,

The operations will be conducted as fixed rate tender procedures with full allotment. The rate in these operations will be fixed at the average rate of the main refinancing operations over the life of the respective operation. Interest will be paid when the respective operation matures.

The allotment was made today and banks borrowed around €489bn.

The ECB had also given banks an option to shift previous funding:

Counterparties are permitted to shift all of the outstanding amounts received in the 12-month LTRO allotted in October 2011 into the first 3-year LTRO allotted on 21 December 2011.

And according to today’s press release,

The allotment amount of EUR 489,190.75 million includes EUR 45,721.45 million that were moved from the 12-month LTRO allotted in October 2011. A total of 123 counterparties made use of the possibility to shift, whereas 58 banks decided to keep their borrowing in the 12-month LTRO, which has now a remaining outstanding amount of EUR 11,213.00 million.

Another feature of today’s allotment was that Italian banks issued bonds backed by their sovereign and retained the issuance to place them as collateral with their Banca d’Italia – their home NCB for their bids. According to FT Alphaville,

According to Reuters, 14 Italian banks have listed €38.4bn worth of state-guaranteed bonds ahead of the LTRO.

More information:

RTRS-ITALIAN BANKS TAPPED ECB’S NEW 3-YR LOANS FOR MORE THAN 110 BLN EUROS – ITALIAN BANKING SOURCE

RTRS: 14 Italian banks win clearance for state-backed bond issues worth EUR 57-58bln, figure includes EUR 38.4bln already listed – sources

Another reason the auction received so much attention was due to the huge speculation that banks will borrow from the Eurosystem and use it to purchase the debt of their sovereigns and even other Euro Area governments. To me, this is nothing more than speculation because it fails to understand how banks work – the LTRO was to help banks meet their funding needs. It is true that some banks (and only a few) may have done this “carry trade” but it is highly risky and as Megan Greene of Roubini Global Economics put it,

This sort of carry-trade could be extremely dangerous, because it not only fails to break the banking/sovereign feedback loop, it actually strengthens it.

Gavyn Davies of FT had this to say in his blog (which is a fine explanation).

The French government was very explicit that the liquidity injection could be used by banks to buy sovereign debt with a large positive carry. This will almost certainly prove too optimistic, since the banks need the money to redeem their own bonds, not to buy risky debt from sovereigns. Nevertheless, the ECB is certainly preventing banks from selling sovereign debt that they otherwise would have sold, and it is doing this by expanding its own balance sheet. …

In recent posts on the Eurosystem, I looked at how it operates and in The Eurosystem: Part 2 highlighted how capital flow across borders within the Euro Area has led to a large accumulation of TARGET2 balances by some NCBs such as the Deutsche Bundesbank.

If the euro zone breaks into sorry little pieces, Germany could possibly lose its entire €495 billion claim. That’s more than $650 billion. It is 60 percent bigger than Germany’s annual federal budget—and larger than the lending under the European Financial Stability Facility and other aid programs that have received more scrutiny.

Some experts on TARGET2 disagree. So I got into an argument with a blogger (who has a good understanding of TARGET2, btw) according to whom

But let’s take a closer look. Who is this “Germany”? Will the German residents who got their accounts credited as a result of the Target2-facilitated transfers out of Ireland now lose their money? No. There will be no losses to private citizens. Despite all this misleading stuff about “enforced lending”, German citizens will be very grateful that they managed to repatriate their money to German via Target2.

So “Who is Germany”? Hidden in the above quote is that individuals and corporations only make Germany and that if the Euro collapses and hence the European Central Bank goes out of existence, Germany’s Bundesbank’s TARGET2 loss of €465bn (latest data I could get) will be not really a loss for “Germany”. This can be dismissed easily.

According to the IMF’s Balance Of Payments And International Investment Position Manual or BPM6

The IIP is a statistical statement that shows at a point in time the value of: financial assets of residents of an economy that are claims on nonresidents or are gold bullion held as reserve assets; and the liabilities of residents of an economy to nonresidents. The difference between the assets and liabilities is the net position in the IIP and represents either a net claim on or a net liability to the rest of the world.

A nation’s net wealth is the value of its real assets and its net international investment position. This definition has a Mercantalist bias but they have been proven right many times! A loss of Germany’s TARGET2 balance will represent a loss to Germany as a whole. Let us look at this closely with some real numbers.

According to the Bundesbank’s Balance of Payments Statistics, November 2011, (with English translation below)

(click to enlarge)

(click to enlarge)

Germany had assets of €6,158bn and liabilities of €5,209bn and thus a net asset position of around €949bn.

The table columns 26 and 27 show how Bundesbank’s foreign assets have increased recently but aren’t fully updated. Another table from the publication gives the updated numbers.

(click to enlarge)

with the English translations:

(click to enlarge)

So the Deutsche Bundesbank had a TARGET2 balance of €465bn at the end of October and is still rising! This is a sizable fraction of the net asset position of €949bn. (for other comparions, Germany’s 2010 GDP was €2,499bn).

The reason I went through this detail was to help the reader appreciate the question “Who is Germany”. Many breakup scenarios may put Germany at the risk of losing out this huge asset. No domestic transaction will bring this back to the original level.

There are even more dreadful scenarios one can think of. A sudden loss of confidence and a dramatic “flight to quality” will lead residents and foreigners selling foreign assets in the Euro Area (in addition to non-Euro denominated assets) and shifting the liquidated deposits via TARGET2 to German banks and if Germany loses its TARGET2 balance, it could become a net debtor to the rest of the world!

An example will illustrate this. Suppose there is a further shift of €1,000bn before a Eurocalypse. This will lead to Germany’s gross assets increasing from €6,158bn to €7,158bn and liabilities from €5,209bn to €6,209bn, leaving the net position unchanged but increasing the Bundesbank’s TARGET2 position from €465bn to €1,465bn. A potential impairment of 100% implies that Germany’s Net International Investment Position is minus €516bn. All this ignoring residents’ revaluation losses of assets held abroad in such scenarios which will make the whole thing even more disastrous!

The above analysis is for non-residents inside the Euro Area making a financial flight to quality into Germany. For residents, a shift of say €1bn does not increase gross asset and liability positions – as far IIP construction is concerned – but increases Bundesbank’s TARGET2 assets by €1bn with the same effect as above.

In either case – residents or non-residents – Germany’s net asset position is under high risk because of the potential loss due to Bundesbank’s TARGET2 balance vanishing in thin air.

Of course, it won’t be an immediate risk to Germany in the sense that it can go back to the Deutsche Mark and redenominate debts in the new currency and do a fiscal expansion to prevent a loss in output. At any rate, Germany’s wealth which it earned in all these years would have reduced – a Mercantalist’s nightmare.

This is the fifth part of the series of posts on the description of the Eurosystem. In this post, I will discuss whatever I had kept postponing in previous posts – except central bank swaps, which I will postpone to Part 6.

The Euro Area is comprised of 17 nations using the Euro as the legal tender and this is referred to as EA17. In addition, 10 more nations potentially can join the Euro, so they refer to “EU27”. In the recent “summit to end all summits”, European leaders believed in Merkels and worked toward changing the Treaty. UK’s Prime Minister David Cameron refused to sign the new European accord – a wonderful thing to do.

[The UK always had an opt-out option and this move effectively divorces the UK from EU. The other nation with an opt-out is Denmark. The remaining 8 are: Bulgaria, Czech Republic, Hungary, Latvia, Lithuania, Poland, Romania and Sweden. The Wikipedia entry Enlargement of the Euro Zone has good details.]

Before the summit of political leaders, the ECB, in its monthly monetary policy meeting, decided to take steps to improve banks’ conditions: It will now conduct two LTROs with a maturity of 36 months and reduced reserve requirements from 2% to 1%. Other than that, it allowed NCBs to accept bank loans satisfying certain criteria as collateral and reduced the ratings threshold on Asset-Backed Securities. Before this, the maximum maturity of LTRO till date was 1 year.

In the press conference that followed, Mario Draghi, the President of the ECB, dashed market hopes of a more aggressive intervention of the ECB in the markets. The press conference transcript is here. However, analysts saw this as a signal from the ECB to force Euro Area governments into agreeing into fiscal contraction ahead of the summit and still expect the ECB to intervene.

Securities Markets Programme

Back in May 2010, the ECB observed that yields of a few “peripheral” government bonds were rising and it looked as if it could become a “self-fulfilling prophecy” and decided to intervene in the markets. In the ECB’s words, the Governing Council decided to:

To conduct interventions in the euro area public and private debt securities markets (Securities Markets Programme) to ensure depth and liquidity in those market segments which are dysfunctional. The objective of this programme is to address the malfunctioning of securities markets and restore an appropriate monetary policy transmission mechanism. The scope of the interventions will be determined by the Governing Council. In making this decision we have taken note of the statement of the euro area governments that they “will take all measures needed to meet [their] fiscal targets this year and the years ahead in line with excessive deficit procedures” and of the precise additional commitments taken by some euro area governments to accelerate fiscal consolidation and ensure the sustainability of their public finances.

In order to sterilise the impact of the above interventions, specific operations will be conducted to re-absorb the liquidity injected through the Securities Markets Programme. This will ensure that the monetary policy stance will not be affected.

The outstanding amount held (settled, to be precise) by the Eurosystem as on Dec 2 was about €207bn, as per this link.

This has continued to rise in recent months because of rising yields of government bonds with markets suspecting that the public debts of Spain and Italy are on unsustainable territory. So the Eurosystem intervenes frequently and the market participants quickly figure this out.

Who Buys – NCBs or ECB?

Some people have asked me – who buys the bonds: NCBs or the ECB? The answer – I believe – is both. Someone asked me if there are traders in the ECB building at Frankfurt. I do not know – perhaps a few. Someone pointed out that the ECB may be buying using the NCB as its agent. Possible. There’s another question, which nobody has asked me – does an NCB of country A buy government bonds of country B? I think so. Who decides all this is not an easy question!

For example, according to the Banque de France Annual Report 2010, (page 118 of publication, 108 of pdf)

The total amount of securities held by NCBs of the Eurosystem under the SMP increased to EUR 60,873 million, of which EUR 9,353 million are held by the Banque de France and are shown under asset item A7.1 in its balance sheet. Pursuant to Article 32.4 of the ESCB statute, any risks from the holding of securities under the Securities Markets Programme, if they were to materialise, should eventually be shared in full by the NCBs of the Eurosystem in proportion to the prevailing ECB capital key shares.

Assuming, the Eurosystem didn’t need to buy French government bonds till now, (at least till 2010 end), it seems it has purchased government bonds of other EA17 nations.

What about the ECB? Yes. According to the ECB Annual Report 2010, page 223 (page 224 of pdf):

Compare that to the Eurosystem’s consolidated balance sheet item (7.1 below) which was large compared to €17.9bn above at the end of 2010:

Also, according to Banca d’Italia’s Annual Report 2010 (page 224 of publication, 231 of pdf):

“Securities held for monetary policy purposes” was about €18bn at the end of 2010, of which about €8bn was in government bonds under SMP and the remaining covered bonds.

So to summarize, government debt is purchased by all NCBs and the ECB and the NCB purchase is not restricted to purchasing government bonds of the same nation the NCBs are located.

The same is true with the Covered Bonds Purchase Programme. The latter is somewhat equivalent to the Federal Reserve’s purchase of Agency Mortgage-Backed Securities in the United States. Covered Bonds are somewhat similar to Asset-Backed Securities such as MBS; the former are on balance sheet of the issuing bank, unlike the latter which are moved into Special Purpose Entities. The assets backing covered bonds are clearly identified in a “cover pool” and are “ring-fenced” which means that if the issuing bank closes down due to insolvency, the assets in the covered pool will be used to pay the covered bond holders, before they are available to unsecured creditors including depositors. The reason the ECB has chosen covered bonds instead of ABS is because of the strength of the covered bond lobby in Europe.

Emergency Loan Assistance

Imagine the following. A Euro Area country X’s government bond yields are at rising and the bond markets are highly suspicious of the government’s solvency. Banks are also in a bad situation and funds have made frequent flights out of the country. The banks have provided all collateral they had to their home NCB. (To be technically correct, foreign assets are pledged to the respective foreign NCB who acts as a custodian for the home NCB). The government has €8bn of payments to bond holders this week. The government has enough funds deposited at a local bank, so it can meet its obligations. However, most bond holders are foreigners. When the government pays the bond holders, the payment will go through via TARGET2 and commercial banks will run out of collateral to provide to their home NCB.

The above is one way in which banks can run out of collateral and there are other ways in which the government is not the direct reason for the outflow of funds, such as a simple capital flight. For this reason, some NCBs invented a programme called “Emergency Loan Assistance” which may not have been a terminology used in the Treaty. The relevant article which may provide an NCB with this power is the Article 14.4 of the Statute of the ESCB and of the ECB

14.4. National central banks may perform functions other than those specified in this Statute unless the Governing Council finds, by a majority of two thirds of the votes cast, that these interfere with the objectives and tasks of the ESCB. Such functions shall be performed on the responsibility and liability of national central banks and shall not be regarded as being part of the functions of the ESCB.

The situation highlighted above happened frequently with Greece during the past few months. The ELA, however was first used by Ireland in 2010. From the Central Bank of Ireland Annual Report 2010

(click to expand)

The item highlighted “Other Assets” contains the balance sheet item for Emergency Loan Assistance. More below, but before this, it is instructive to look at Liabilities:

(click to enlarge)

So, the Central Bank of Ireland’s Liabilities to the rest of the Eurosystem was around €145bn! – which is indicative of how much funds flew out of Ireland and the amount of stress the nation went through. (Ireland’s 2010 GDP was €154bn, btw). I described how funds flow within the Euro Area in Part 2 of this series.

Back to ELA. Page 104 of the publication (106 of the pdf) describes Other in Other Assets as:

This includes an amount of €49.5 billion (2009: €11.5 billion) in relation to ELA advanced outside of the Eurosystem’s monetary policy operations to domestic credit institutions covered by guarantee (Note 1(v)). These facilities are carried on the Balance Sheet at amortised cost using the effective interest rate method. All facilities are fully collateralised and include sovereign collateral as well as a broad range of security pledged by the counterparties involved.

The Bank has in place specific legal instruments in respect of each type of collateral accepted. These comprise: (i) Promissory Notes issued by the Minister for Finance to specific credit institutions and transferrable by deed, (ii) Master Loan Repurchase Deeds covering investment/development loans, (iii) Framework Agreements in respect of Mortgage-Backed Promissory Notes covering non-securitised pools of residential mortgages, (iv) Special Master Repurchase Agreements covering collateral no longer eligible for ECB-related operations and (v) Facility Deeds providing a Government Guarantee. In addition, the Bank received formal comfort from the Minister for Finance such that any shortfall on the liquidation of collateral is made good. Where appropriate, haircuts (ranging from 5.5 per cent to 80 per cent) have been applied to the collateral. Credit risk is mitigated by the level of the haircuts and the Government Guarantee. At the Balance Sheet date no provision for impairment was recognised.

You can find details of these in this blog post Irish Central Bank Comfort at the blog called Corner Turned, which is now inactive.

Oh yeah … How does the Irish NCB provide the loans? Hint: Loans make deposits.

FT Alphaville has two nice posts (among others) on ELA in Greece: Sundry secret Greek liquidity [updated], Hooray for, erm, Greek ELA?. The first one pokes on how the Bank of Greece – Greece’s NCB – hides the item under “Sundry” and the second one one how Greek banks’ net interest income were higher than expected – the reason being that expensive deposits were replaced by cheaper NCB funding!

This concludes this post. In Part 6 – the final one – I will discuss central bank liquidity swap lines with the Federal Reserve.

This is a continuation of posts The Eurosystem: Part 1, Part 2, and Part 3 in which I went through a description of the payment system TARGET2 both domestic and cross-border and the process of how banks obtain reserves from the Eurosystem.

This post will go into the details of the Eurosystem operations. Like all central banks, the ECB simply targets interest rates, in particular the EONIA – the Euro Overnight Index Average . It is “[a] measure of the effective interest rate prevailing in the euro interbank overnight market. It is calculated as a weighted average of the interest rates on unsecured overnight lending transactions denominated in euro, as reported by a panel of contributing banks” according to the ECB website.

It should be noted outright that at some places in the ECB website, there are claims that it controls the money stock. A closer investigation shows no sign of the ECB doing anything of the sort and this claim is just a rhetoric. The Eurosystem is acting just like other central banks, changing short term interest rates and attempting to impact demand. It is impossible for any central bank to control the money stock. I had two posts on money endogeneity: Horizontalism and More On Horizontalism.

Reserve Requirements

Credit Institutions (banks) have an account at their home NCBs and have to maintain a minimum of 2% of their liabilities subject to reserve requirements. The ECB can change this from 2%, but it has never done this so far. Different central banks have different rules on which liabilities are to be included when calculating reserve requirements. For the Eurosystem, overnight deposits, deposits with maturity up to two years are included and so are debt securities with maturity up to two years. Repos, liabilities vis-à-vis other credit institutions including the Eurosystem, debt securities with maturity greater than two years are not included.

Deposits subject to reserve requirements are remunerated at the rate of the main refinancing operations (MROs).

Needless to say, reserve requirements do not reduce banks’ ability to make loans – since loans make deposits and deposits make reserves.

How do banks, as a whole, get the extra (not excess) reserves after they make loans? Either via Standing Facilities, which we consider next or through Open Market Operations.

Standing Facilities

The Eurosystem uses a corridor system for targeting interest rates. Banks can use the deposit facility and are paid interest on excess reserves and can borrow against eligible collateral under the marginal lending facility. For latter, how much? As much as they can, provided they have collateral. According to an old document from the ECB, saying the same:

So the interest rates on the deposit and marginal lending facilities act as a corridor.

In “good times”, banks will lend all their excess reserves to other credit institutions. Since the Eurosystem is adjusting the amount to reserves to hit its interest rate target, some banks may fall short of reserves which they can easily borrow from other banks. Because of uncertainty, some banks will be driven to the marginal lending facility and the Eurosystem will try to fine tune to reduce this. In may also be the case that the banking system as a whole is left with excess reserves and the Eurosystem may try to fine tune this in reverse direction (and will in “good times”). We will see how this happens in the next section.

For what happens during the day, see the end of Part 1 of this series.

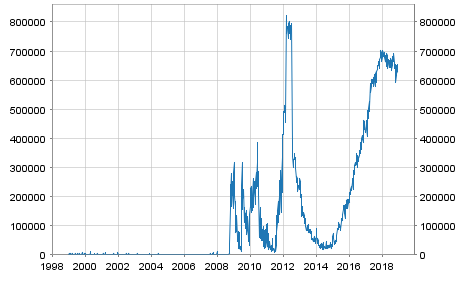

But … the crisis hit, and banks became suspicious of other banks’ creditworthiness and this led to a freeze in the interbank market. Banks were cautious in lending each other and also about their own liquidity needs. Thus, they kept a lot of deposits at their home NCB. So one hears of banks “parking” a lot of funds at the Eurosystem. The following chart from the ECB Statistical Data Warehouse highlights the stress in the interbank markets. The y-axis is in Millions of Euros.

Chart updated 6 Dec 2018, as the previous link was broken.

Before we go into Open Market Operations, a table summarizing the Eurosystem’s operations (from the same document linked above)

Government Deposits

For reasons not clear to me, monetary policy documents do not emphasize an important fine tuning operation – shifting of government deposits between NCBs’ and banking system’s books. Movement of funds into and from the government’s account at its home NCB can cause a lot of errors in forecasting liquidity and can cause fluctuations in the rate at which banks are lending each other overnight. At the same time, if managed sufficiently well, it becomes a good tool for fine-tuning! This link from the ECB’s website has some discussion on this.

Open Market Operations

Via, open market operations, the Eurosystem manages banks’ needs for reserves. It neither controls the money stock in the Euro Area nor controls the amount of reserves in any sense of the usage of the word “control”. It may pursue a non-accommodating or a dynamic policy, where it hikes the interest rate, depending on the growth of the money stock but gone are the days of Monetarism! The Eurosystem is defending its target rate, the main refinance rate, which is usually mid-way between the rates for the deposit facility and the marginal lending facility. In recent times, due to banks’ high credit risk, it has lost control of this.

As per Table 1 above, the Eurosystem categorizes its operations as

main refinancing operations,

longer-term refinancing operations,

fine-tuning operations and

structural operations.

We can also describe them – as done by the “Monetary Policy Implementation” document – as follows:

Reverse transactions: MROs, LTROs, Fine-tuning Reverse Operations and Structural Operations;

Outright Transactions;

Foreign Exchange Swaps;

Issuance of ECB Debt Certificates, Collection of Term-deposits.

Before we get into a description of the above items, it should be made clear from the start, that the reader should keep in mind the similarities and differences between this and the procedures adopted by the Federal Reserves in the United States. As mentioned in Part 1, the Federal Reserve and the banking system can be described as asset-based type, while the monetary system in the Euro Area as an overdraft monetary system. (It should also be made clear that “overdraft” here does not mean national governments have an overdraft facility at their home NCB – they don’t have).

For example, it is easy to confuse MROs and LTROs with the (non-permanent) open market operations done by the Fed. The confusion arises because both MRO/LTROs and the Fed’s open market operations are carried out using repurchase agreements (repos). I will have another blog post on the Federal Reserve procedures, but suffice to say here that the Fed’s repos are more comparable to Fine-tuning Reverse Operations.

Reverse Transactions

As mentioned, earlier banks as a whole in the Euro Area obtain all reserves by directly borrowing from the Eurosystem. An exception is that in recent times, banks have seen their reserves increase due to the ECB’s two programs – Securities Markets Programme and Covered Bond Purchase Programme.

Let us consider MROs first.

Every week, the Eurosystem refinances the liquidity needs of the banking system via this operation. According to the implementation document,

- They are liquidity-providing operations. – They are executed regularly each week. – They normally have a maturity of one week. - They are executed in a decentralised manner by the National Central Banks. - They are executed through standard tenders. – All counterparties fulfilling the general eligibility criteria may submit tender bids for the main refinancing operations. - Both tier one and tier two assets are eligible as underlying assets for the main refinancing operations.

So every week, the Eurosystem lends banks amounting billions of Euros via an auction but these are executed in a decentralised manner by the NCBs as repurchase agreements. (Edit: 21 Dec 2011: A bit incorrect to term MRO/LTROs as “repos”). During the week, funds flow in all directions and banks will borrow from each other.

What about LTROs?

These are almost similar to the MROs, except that they are executed every month and normally have a maturity of three months. In recent times, the ECB has been more accommodative and has offered LTROs with longer maturities such as six months.

Since the frequency of MROs is one week, there needs to be some tool for the Eurosystem during the week to fine tune reserves so that interbank lending rates do not deviate from the target. So Fine-tuning Reverse Operations. These need not have fixed maturities and can be done in short notice but executed in a decentralised manner by the NCBs. About Structural Reverse Operations, I have nothing to say!

Outright Transactions, FX Swaps, ECB Debt Certificates & Term Deposits

In addition, the Eurosystem may employ other tools to provide or remove liquidity such as outright purchases or sales of domestic securities or entering into foreign exchange swaps with financial institutions. These are generally decentralised i.e, executed by the NCBs but the ECB may sometimes be involved. Collection of term deposits and issuance of ECB debt certificates absorb liquidity (i.e., reserves). The former is executed by the NCBs. Debt certificates are settled in a decentralised manner by the NCBs. Another difference between the two is that the former is not marketable, while the latter is.

Conclusion

A bit boring, wasn’t it? Haven’t yet covered ELA (Emergency Loan Assistance), SMP (Securities Markets Programme) and CBPP (Covered Bond Purchase Programme). My aim was to detail out the monetary operations so that we know what the Eurosystem does, what it doesn’t and what it can do (and what it cannot do!). Probably ELA, SMP & CBPP for the last part in the series – Part 5.

Addendum

How does the ECB change short term interest rates in normal times? By a simple announcement. Banks will automatically start lending each other at the target rate. MROs are done weekly, and there will be no additional MRO that needs to be done post/pre the announcement. Neither do fine-tuning reverse operations change in volume because of the decision.

In the previous post in this series The Eurosystem: Part 2, I discussed cross-border flows within the Euro Area. With exceptions, most of these flows are current balance of payments and balance of payments financing flows. Of course there are other flows with the world outside the EA17 and these flows flow via the correspondent banking arrangements banks have put in place and not the topic of discussion in this series.

The cross-border flows are important for the Euro Area since as a whole, the Euro Area’s balance of payments is almost in balance.

So the Euro Area current account was in a deficit of €11.7bn in 2011Q3 and a net indebtedness of €1.35tn to the rest of the world at the end of Q3, or 14.5% of GDP. So most of external imbalances of the EA17 nations are within the Euro Area.

Back to TARGET2 flows: there was a debate among some economists on various matters related to these flows. Some even went on to suggest that these flow affect credit in Germany because the nation was financing the current account of the other nations. From an exogenous money viewpoint, this reduces banks’ ability to provide loans to their customers! (which is incorrect because money is not exogenous). The replies tried to disprove it by using the argument that attempted to prove that the NCBs were not financing the current account. Sorry no links.

This is a small post and my point is to show that since TARGET2 is designed to automatically change the balance sheets of the NCBs, the debate whether the NCBs finance the flows or not is a bit counterproductive. Of course having said this, I wish to highlight the fact that the item “Claims within the Eurosystem” (in either assets or liabilities) is definitely recorded in the balance of payments and the international investment position as can be seen below for the case of Spain.

Of course, the “Claims Within the Eurosystem” is just one item in the financial account and the international investment position, so not the whole of the current account deficit is financed this way. One minor advantage is that this part of the gross indebtedness of a whole deficit nation is at the ECB’s main refinancing rate, which is much lower than the effective interest rate deficit EA nations are paying on their gross liabilities to foreigners. This is not worthy of further attention, though.

How long can these flows continue? As long as the banks have sufficient collateral to provide to their home NCB. When banks run out of collateral (eligible for borrowing from the Eurosystem), emergency measures have to be taken and a future post in this series will discuss the Emergency Loan Assistance Program (ELA) used by NCBs.

[I welcome your comments. I have a “Zero Comments Policy” as opposed to a “No Comments Policy”. I like being notified of a comment.]

In a post last week – The Eurosystem: Part 1, I went into the Euro Area payment system TARGET2 and touched upon domestic payments and implementation of monetary policy in the Euro Area. This post takes off from their to discuss cross-border flows. There are two reasons for looking into this is:

to understand the flow-of-funds in the Euro Area – in particular current balance of payments and balance of payments financing flows;

to understand how the Eurosystem – the ECB and the 17 National Central Banks (NCBs) work together.

Suppose a Firm F (F for France) banking at BNP Paribas wants to send a payment of €1m to a Firm G (G for Germany) banking at Deutsche Bank. How do the funds flow? In Part 1, I discussed how funds flow for domestic payments, but here two nations are involved and hence is likely to be more complicated. The various institutions involved in this transaction are

Firm F

BNP Paribas

Banque de France, France’s NCB

Deutsche Bundesbank, Germany’s NCB

Deutsche Bank

Firm G

European Central Bank (ECB)

To work out how the funds flow and what effects it has on the balance sheets of these institutions, it is again useful to get into the Eurosystem legal framework as we did in Part 1.

According to the Guideline of European Central Bank of 30 December 2005 on a Trans-European Automated Real-time Gross settlement Express Transfer system (TARGET) (ECB/2005/16) Article 4(b)1&2 (link):

and according to Article 4(c)2:

Further, according to Article 4(d)2:

So the NCBs and the ECB have accounts at each other and grant each other unlimited and uncollateralized credit! i.e., they allow all funds to go through. This was shocking when I first discovered this from the same document but later realized it makes sense. There is one more rule that is still missing – how the NCBs settle with each other.

Intra-ESCB transactions are cross-border transactions that occur between two EU central banks. Intra-ESCB transactions in euro are primarily processed via TARGET2 – the Trans-European Automated Real-time Gross settlement Express Transfer system (see Chapter 2 of the Annual Report) – and give rise to bilateral balances in accounts held between those EU central banks connected to TARGET2. These bilateral balances are then assigned to the ECB on a daily basis, leaving each NCB with a single net bilateral position vis-à-vis the ECB only. This position in the books of the ECB represents the net claim or liability of each NCB against the rest of the ESCB. Intra-Eurosystem balances of euro area NCBs vis-à-vis the ECB arising from TARGET2, as well as other intra-Eurosystem balances denominated in euro (e.g. interim profit distributions to NCBs), are presented on the Balance Sheet of the ECB as a single net asset or liability position and disclosed under “Other claims within the Eurosystem (net)” or “Other liabilities within the Eurosystem (net)”. Intra-ESCB balances of non-euro area NCBs vis-à-vis the ECB, arising from their participation in TARGET2, are disclosed under “Liabilities to non-euro area residents denominated in euro”.

Using these rules and procedures, we can work out the example presented at the beginning of this post.

At the initiation of the payment of €1m by Firm F, BNP Paribas will debit Firm F’s account €1m, Banque de France will debit BNP Paribas’ account €1m, Deutsche Bundesbank will credit Deutsche Bank’s account €1m and Deutsche Bank will credit Firm G’s account €1m. There remains the settlement between Banque de France and Deutsche Bundesbank and intraday, they settle bilaterally and then settle at the ECB at the end of the day. An important point however is that when NCBs settle with the ECB, they do not need to provide collateral. Also, in principle the overdraft facility provided by the ECB is unlimited.

Some clarifications. How did NCB provide intraday credit to BNP Paribas? The answer is quite simple: Ex Nihilo, at the stroke of a pen, rather automatically via the system’s computers! The same with Deutsche Bundesbank – it provided Deutsche Bank with settlement balances in the same manner, and so did Deutsche Bank provide €1m of extra deposits to its customer Firm G. And finally at the end of the day, the ECB does the settlement between the NCBs on its books.

However, this is not the end of the story. During the day, there are payments in all directions but let us ignore that. So BNP Paribas finds itself with a positive intraday credit of €1m from Banque de France. Intraday overdrafts were discussed in Part 1 and I repeat the relevant part here. Toward the end of the day, banks may want to instead borrow from the rest of the financial system, instead of relying on central bank credit because the latter is free of interest only intraday and is charged an interest rate equal to that of the marginal lending facility overnight. Typically, this poses no problem because some banks may have excess reserves which they may want to lend out because keeping it deposited at the central bank will pay an interest equal to that of the deposit facility which is lower. So typically, banks would retire intraday credit toward the end of the day and borrow funds from the rest of the financial system.

In this case, BNP Paribas would have to borrow abroad because other banks do not have excess reserves in the example. Deutsche Bank will be looking to lend the funds at a higher rate than depositing it at Bundesbank which pays lower interest and we have a situation in which BNP Paribas will borrows funds from Deutsche Bank. The interest rate on this lending/borrowing will likely be the near the ECB main refinancing rate – else, the ECB will intervene to bring the EONIA to the main refinancing rate – its target. It is important to remember that this causes the reversal of the balance sheet changes of the ECB and the NCBs – changes which happened when funds flowed from Firm F to Firm G.

All this is when there is no stress in the markets. During periods of crisis, banks in some affected regions may see deposits flowing out due to worries about credit risk. Banks which are losing funds are unable to borrow funds from abroad and this leaves banks indebted to their home NCBs and the NCBs have a large Other liabilities within the Eurosystem (net).

The Bundesbank Monthly Report March 2011 has a special topic The dynamics of the Bundesbank’s TARGET2 balance on Page 34 and has a good discussion. It has two nice charts, one of them is settlement balances of each NCB in the Eurosystem

This was at the end of 2010 and would have worsened in recent times and shows the amount of stress in the banking system.

In Part 3, I hope to discuss the implementation of monetary policy – i.e., the ECB procedures on setting the interest rate and the differences and similarities with the American system.

Hopefully there is a Part 4 which goes into the “sovereign debt” crisis – which really is a balance of payments crisis worsened by the fact that Euro Area national governments do not have a lender of the last resort.

The Eurosystem consists of the European Central Bank (ECB) and 17 National Central Banks (NCBs) of the member nations. The purpose of this post (and some that will follow) is to explain how the RTGS payment and settlement system called TARGET2 works in order to understand the flow of funds within the Euro Area. The purpose is also to show that money is endogenous in the Euro Area, that it cannot be otherwise and describe the Euro Area economic dynamics in the money endogeneity framework

First consider payments within a nation, i.e., domestic payments. In the Euro Area, it happens exactly in the way as in any nation. I had a post covering this – Payment Systems And Settlement. An example illustrates this:

Suppose a household A holding deposits in Bank A in Spain wishes to make a payment of €100 to an institution B banking at Bank B. The household A will give an instruction to her Bank A to transfer funds to Bank B. Assuming this goes through, the Spanish central bank Banco de Espana will debit Bank A’s account and credit Bank B’s account. Bank B will credit institution B’s account €100. If Bank A has insufficient funds at Banco de Espana, the latter will provide the former intraday credit free of charge.

So transactions such as the above give rise to payment flows in all directions. To understand how the Eurosystem handles this, it is useful to go into some rules.

The Guideline of European Central Bank of 30 December 2005 on a Trans-European Automated Real-time Gross settlement Express Transfer system (TARGET) (ECB/2005/16) 3(f) 1 says (link)

and 3(f)3 says

and finally 3(f)5 says

So within the day banks can go into overdraft at the home central bank by pledging collateral. In practice, banks have more collateral at the central bank to cover for daily fluctuations. Also, in the Euro Area, banks need to satisfy a reserve requirement of 2% which means that the amount of reserves deposited at the NCB should be at least 2% of the deposit liabilities. How do banks get the reserves when they lose reserves? During the day, the intraday credit itself provide the reserves. (Loans make deposits!). However toward the end of the day, banks may want to instead borrow from the rest of the financial system, instead of relying on central bank credit because the latter is free of interest only intraday and is charged an interest rate equal to that of the marginal lending facility overnight. Typically, this poses no problem because some banks may have excess reserves which they may want to lend out because keeping it deposited at the central bank will pay an interest equal to that of the deposit facility which is lower. So typically, banks would retire intraday credit toward the end of the day and borrow funds from the rest of the financial system.

An exception to the above arises during periods of market stress or crisis, when banks prefer to not lend the excess funds due to credit risks and are happy to keep funds deposited at the central bank despite earning lower interest.

As banks create more money by lending (more credit to be precise), the reserve requirement of the whole banking system would increase. How do banks in the Euro Area get more reserves?

It is useful here to distinguish between two types of monetary systems – overdraft and asset-based. In the former, banks as a whole get all the reserves directly by borrowing from the central bank (provided they pledge good collateral) and in the latter, the central bank would create reserves required by the banking system by engaging in permanent open market operations or outright operations, typically purchasing government bonds. The Euro Area monetary system is best described by the former and Anglo-Saxon monetary systems such as one in the United States is best described by latter. Even in the latter, the Federal Reserve does provide direct credit to banks but these are retired quickly. The distinction can be made by looking at the balance sheet of the central bank.

We are yet to see the Eurosystem being described as a whole, but for our purpose of clarifying how an overdraft system looks, it is sufficient to just take a glance at the consolidated balance sheet to verify. The Eurosystem balance sheet near the end of 2006 looked like this (link):

(click to enlarge)

The item rounded in red is €450, 540 million which is a big proportion of the total size of the balance sheet, and one doesn’t see this for the Federal Reserve (in normal circumstances).

Since the Eurosystem is an overdraft type, the funds obtained have to be provided by direct lending by the Eurosystem. This is done mainly via two types of operations – Main Refinancing Operations (MROs), and Long Term Refinancing Operations (LTROs), where the Eurosystem conducts an auction to lend the whole banking system. For the former, the auctions are held weekly and the lending is for one week. LTROs, it is typically conducted every month and the duration of refinancing is three months. As the names suggest, MROs are used mostly.

This will conclude my post. The posts following this will look at cross-border flows of funds and government accounts. They (either one post or two) will attempt to provide the reader an idea of how cross-border dynamics are important for the Euro Area.

Update: Corrected the discussion on frequency and duration of LTROs in the second last para.