Recently I commented on a paper, The Financial Crisis In The Eurozone: A Balance-Of-Payments Crisis With A Single Currency? by Eladio Febrero, Jorge Uxó and Fernando Bermejo, published in ROKE, Review Of Keynesian Economics. I hadn’t realised that Sergio Cesaratto has a reply (paywalled) in the same issue.

Sergio Cesaratto. Picture credit: La Città Futura, Sergio Cesaratto

Abstract:

Febrero et al. (2018) criticise the balance-of-payments (BoP) view of the European Economic and Monetary Union (EMU) crisis. I have no major objections to most of the single aspects of the crisis pointed out by these authors, except that they appear to underline specific sides of the EMU crisis, while missing a unifying and realistic explanation. Specific semi-automatic mechanisms differentiate a BoP crisis in a currency union from a traditional one. Unfortunately, these mechanisms give Febrero et al. the illusion that a BoP crisis in a currency union is impossible. My conclusion is that an interpretation of the eurozone’s troubles as a BoP crisis provides a more consistent framework. The debate has some relevance for the policy prescriptions to solve the eurocrisis. Given the costs that all sides would incur if the currency union were to break up, austerity policies are still seen by European politicians as a tolerable price to pay to keep foreign imbalances at bay – with the sweetener of some European Central Bank (ECB) support, for as long as Berlin allows the ECB to provide it.

Sergio carefully responds to all views of Febrero et al. and Marc Lavoie, Randall Wray and also Paul De Grauwe, pointing out that he agrees with most of their views except that their dismissal of this being a balance-of-payments crisis with their claims that the problem could have been addressed by the Eurosystem/ECB lending to governments without limits. He points out that, “The austerity measures that accompanied the ECB’s more proactive stance are clearly to police a moral hazard problem”. It is true that the ECB, the European Commission and the IMF overdid the austerity but it doesn’t mean that Sergio’s opponents’ claims are accurate.

… But more disturbing still is the notion that with a common currency the ‘balance or payments problem’ is eliminated and therefore that individual countries are relieved of the need to pay for their imports with exports.

Quite the reverse: the existence or a common currency makes a country more directly dependent on its ability to sell exports and import substitutes than it was before, particularly as it will then possess no means whereby it can (in the broadest sense) protect itself against failure.

– Wynne Godley, Commonsense Route To A Common Europe, inThe Observer, 6 January 1991.

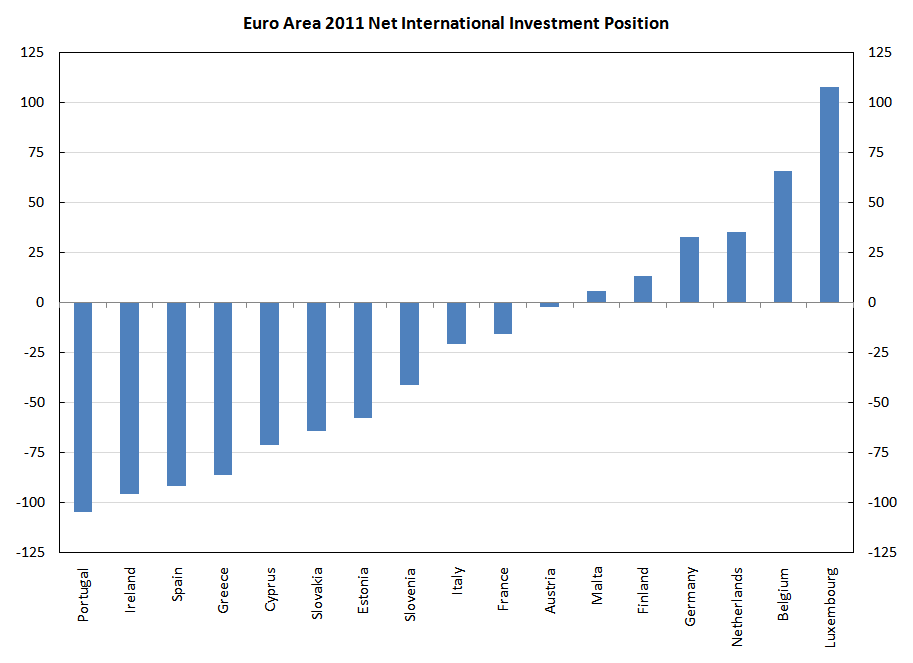

Greece had large negative current account balance of payments and Germany had the opposite over the lifetime of the Euro.

Yet, there are some economists who argue that the Euro Area crisis is not a balance of payment crisis. Of course there are other aspects to the crisis as well but this in my view is the main issue. There was a debate between Sergio Cesaratto and Marc Lavoie on this. Now there is a new paper in the most recent issue of ROKE (Review of Keynesian Economics) by Eladio Febrero, Jorge Uxó and Fernando Bermejo which discusses this. The Wayback Machine/Internet Archive link is here if you are reading it after the journal puts the paywall again.

The authors seem to be against Sergio Cesaratto view. Since I agree with Cesaratto, I thought I should comment on it.

The fundamental problem of the Euro Area is that it doesn’t have a central government. If there had been a central government like the US federal government, with large fiscal powers, the Euro Area crisis would have been far less deeper. This is because weaker regions would have been recipients of “fiscal transfers”, i.e., receive more government expenditure than what they send in taxes.

Fiscal transfers can be seen transactions in the balance of payments of Euro Area countries if the EA had a central government. The way to do balance of payments for monetary and political unions is explained in the IMF Balance of Payments and International Investment Position manual. Take a country like Greece. The Euro Area government would be considered external to Greece. Same for other countries. But for the Euro Area as a whole, the central government would be considered inside the Euro Area.

So government expenditure would appear in Greek exports in the goods and services account and transfers in the secondary income account. Taxes would appear only in the latter.

So there is an improvement in the current account balance of payments for regions compared to the case when there is no central government. Current account balances accumulate to the net international investment of the whole country. A country which has persistent imbalances would have negative net international investment position, i.e., indebtedness to other countries.

So fiscal transfers keep all this in check by improving the current account balance. So if the Euro Area had a central government, debts of a country like Greece would be in check.

By joining the half-baked half-way house, Greece got an overvalued exchange rate and easier access for other Euro Area countries into its markets and its external imbalances worsened in its lifetime inside the monetary union.

Nations with high current account deficits will also have higher public debt than otherwise and would need international investors to buy the debt which residents won’t. Normally the price would adjust to bring international investors but as we have seen, sometimes there is no price and a fall in bond prices might lead to expectations of further fall leading external investors to dump the bonds instead of finding them attractive.

The trouble with Febrero et al. is that they seem to think that the European central bank can purchase all government debt of nation. Certainly, the European Central Bank (ECB) has stepped in at various times to ease the pressure on government bond markets. But the trouble with this is that there are under some conditions such as assuming it can impose tight fiscal policy on the governments it is helping.

If the Euro Area treaty is modified to allow countries to have independent fiscal policies, then for stability, the ECB has to buy bonds without limits and can keep accumulating. It is a political mess. A country like Germany could argue that it is writing an open cheque to Greece.

A political union wouldn’t have such problems. National level governments such as the Greek government would have fiscal rules on them, and hopefully not the supranational government. This is like the United States where state governments have rules on their budgets.

In contrast, if the ECB guarantees Greece’s debt, it has to impose some rules and since Greece is not recipient of any equalisation payments—the fiscal transfers—its performance is still dependent on its competitiveness. This is because competitiveness would affect the Greece government’s fiscal balance and hence put a deflationary pressure on Greece’s fiscal stance.

On the other hand, a Euro Area with a central government would imply Greece is recipient of substantial equalisation payments and its competitiveness isn’t so binding.

An argument of the economists arguing that the European monetary system has this thing called TARGET2 and that the intra-Eurosystem balances (i.e., automatic credits offered by one national central bank to another) can rise without limit is used in this paper. This is highly misleading. It is true but one should look at the changes in debits and credits elsewhere. Suppose a country like Greece sees a large private financial outflow. While T2 can absorb a lot of this—much more than anyone imagined—in the late stages, Greece banks become heavily indebted to their national central bank, The Bank of Greece. When they run out of collateral, the rules under ELA, Emergency Liquidity Assistance, is triggered. So TARGET2 or more accurately the Eurosystem cannot absorb everything.

In summary, the Euro Area cannot do without a central government in the long run. Anyone who thinks that the ECB or the Eurosystem can buy whatever residual debt private investors doesn’t understand that in such a system, Euro Area governments are given an open cheque.

The difference between not having a central government and a central government is that in the former, there is no equivalent income flow as in the latter. The Eurosystem purchases would affect the financial account of balance of payments, not the current account.

One of the noticeable assertions of the paper is:

With T2, there is just one currency. This means that if foreign exchange markets did not exist, there could not be a BoP crisis, so that the cause of the crisis should be found elsewhere.

The trouble with this is that it sees it only as a currency crisis. But the fact is that countries whose external position were weak were the ones running into trouble in the Euro Area. Had current account deficits not blown up, countries would have had better fiscal balance since the current account balance and the budget balance are related by an identity and even behaviourally as can be seen in stock-flow consistent models. In crisis times, foreign investors are more likely to shift their funds in their home countries. With better balance of payments, public debt would be held more internally and there would have been less pressure on government bonds.

There are comments in the paper about too much credit etc. This is true, but then the Euro Area crisis would have looked more like the economic and financial crisis affected the United States.

Here’s the the NIIP of Euro Area countries in 2011.

Doesn’t this explain why Germany was in a better position than Greece when the crisis started heating up? Or that Netherlands was in a better position than Portugal?

Recently, Mario Draghi—in a letter responsing to questions about TARGET2 imbalances to two members of the European Parliament—says the following:

If a country were to leave the Eurosystem, its national central bank’s claims on or liabilities to the ECB would need to be settled in full.

Since many years many economists, led by Karl Whelan have refused to accept this. There has been a denial via various arguments. The main argument of this camp has been that TARGET2 assets of the ECB doesn’t really matter, presumably because central banks create money and can be capitalized using a bookkeeper’s pen. That is a strange argument because if a country were to leave the Eurosystem and cannot settle its claims to the ECB, the ECB will take a loss. It has less interest earning asset than otherwise and since the ECB’s profits ultimately get distributed to national treasuries, treasuries’ income doesn’t matter according to this argument.

Another way to see this argument is wrong is to think of the international investment position of the remaining region if a country leaves. It’s net international investment position falls. Does international investment position not matter?

Yet another argument. Suppose the day before a country leaves the Euro Area and the Eurosystem, the ECB were to buy that country’s government bonds. The leaving country’s NCBs’ liabilities to the rest of the Eurosystem will fall and its government’s liability will rise. This transaction is a purely financial account transaction in international accounts. How it is that one is debt and the other not debt? Those who claim that the intra-Eurosystem debts do not matter seem to believe that it’s not debt.

Of course, Mario Draghi’s position can be legally challenged. There’s hardly any mention in the legal documents of the Euro Area explicitly stating what happens. But since intra-Eurosystem claims (i.e., NCB TARGET2 balances) earn or pay interest, this makes the case for the settlement of the claims. In law, the reasons why they were created are sometimes used if something is not explicitly stated.

There’s a discussion on Nick Rowe’s blog about the interpretation of TARGET2 balances of the NCBs in the Euro Area’s Eurosystem. How do we interpret this? My answer is the headline.

TARGET2 balances arise because of cross-border payment flows within Euro Area countries. Instead of going through how these arise, I assume the reader knows them. I have covered it many times in my blog and many others have written it.

Let’s work here in the approximation that the Euro Area is the world and there’s no economic activity outside it. Since cross-border flows within the Euro Area banking system and the Eurosystem are transactions between resident economic units and non-resident units, these flows will give rise to entries in the balance of payments of each nation within the Euro Area.

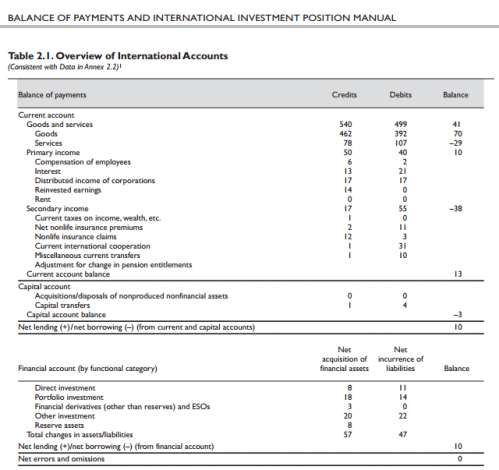

In the new balance of payments terminology, such as as in the sixth edition of the Balance Of Payments And International Investment Position Manual, (BPM6), there’s an identity:

current account balance + capital account balance = net lending (financial account balance).

For terminologies see this table from the guide:

This is an identity but suggestive of some behaviour. The question is what is the residual in this. The current account consists of things such as exports, imports, interest payments between resident and non-resident units and so on. The capital account consists of acquisitions and disposals of non-produced non-financial assets and capital transfers. The financial account consists of things such as direct investment flows, portfolio investment flows and so on. Other than that, there’s also “reserve assets” and “other investment”.

[accommodative capital flows] take place only because the other items in the balance of payments are such as to leave a gap of this size to be filled … [while] autonomous payments … take place regardless of other items in the balance of payments.

Strictly, this distinction makes sense in fixed exchange rate regimes. In floating exchange rate system, the two—accommodative and autonomous—can’t be clearly be separated.

Anyway, coming back to the Euro Area, before the crisis started, the banking system was working fine. So there would be flows in both the current account and the financial account. The goods and services balance in the current account depends on domestic demand and output at home and abroad and relative competitiveness. There’s no reason for this to be zero. Economic units engaged in the financial markets would buy and sell securities and these affect the financial account of the balance of payments of the two nations involved in the transaction. There’s no reason for balance of things such direct investment, portfolio investment (and financial derivative flows) to balance or to equal the current account balance. Since flows typically are via TARGET2, this affects banks’ balances at their NCBs. So it’s possible toward the end of the day for banks in Spain 🇪🇸 as a whole to find themselves in need for reserves (or settlement balances) and banks in say Germany 🇩🇪 to be in a situation where they have excess funds. So banks in Spain will likely contact banks in Germany to borrow funds, either for one day or more. This is because they will get a cheaper interest rate. If they borrowed from their NCB, the interest rate is slightly higher.

These borrowings and lendings give rise to other investment in balance of payments of the two nations. So in Meade’s language, this is an accomodative flow. Not all other investment items are accommodative flows and similarly, not all accommodative items are other investment items.

But as the financial crisis began in 2007, the interbank system froze. Banks didn’t lend each other much. Hence the residual was balances between the NCBs. This would arise automatically. So these flows can be said to be accommodating. The counterpart of this is banks borrowing from their NCBs.

There’s a technicality: somewhere around mid-2000s, the system was changed so that the bilateral balances of NCBs were assigned to the ECB on a daily basis.

Since the TARGET2 balance of NCBs is a stock and not a flow, they can be hence thought of as the cumulative accommodative item. Since the crisis, a lot of things have happened. The European Central Bank has taken various steps, so that banks have sufficient liquidity. Banks have been given facilities to borrow huge amounts from their NCBs for collateral at cheap rates. Later the ECB also started its asset purchase program in which it bought government bonds, ABS and covered bonds. Some of these were already in existence when the interbank markets froze. So even as interbank markets opened, they didn’t feel the need to borrow funds from banks abroad.

The IMF’s guide BPM6 says in Appendix 3 that these intra-Eurosystem claims (the TARGET2 balances) are to be recorded in Other Investment:

Intra-CUNCBs and CUCB balances

A3.46 Transactions and positions corresponding to claims and liabilities among CUNCBs and the CUCB (including those arising from settlement and clearing arrangements) are to be recorded for the central bank under other investment, currency and deposits or loans (depending on the nature of the claim) in the balance of payments and IIP of member economies. If changes in these intra-CU claims and liabilities do not arise from transactions, relevant entries are to be made under the “other adjustment” column of the IIP. Remuneration of these claims and liabilities is to be recorded in the balance of payments of CU member economies as income on a gross basis under investment income, other investment.

where CUCB and CUNCB are abbreviations for currency union central bank and currency union national central bank, respectively.

There is some similarity with “reserve assets” in the financial account of the balance of payments and the international investment position when comparing all this to a fix exchange rate regime. In the latter, when autonomous flows aren’t sufficient, the central bank may sell gold or foreign reserves in the markets. It may also engage in borrowing funds in foreign currency. These are also accommodative flows. In the Euro Area case however, the inter-NCB claims (and the assignment to the ECB) happens automatically. Also “reserve assets” don’t go below zero, while TARGET2 balances can be negative in the sense that they are in liabilities of some NCBs instead of being in assets.

The conclusion of all this is that TARGET2 is a sort of a residual finance to a whole nation which arises automatically. Some have interpreted this to conclude that this is unlimited. This is however not the case. Since the counterpart to these are banks’ borrowing from their NCBs, this is limited to how much collateral banks can provide the Eurosystem, with or without the help of their government.

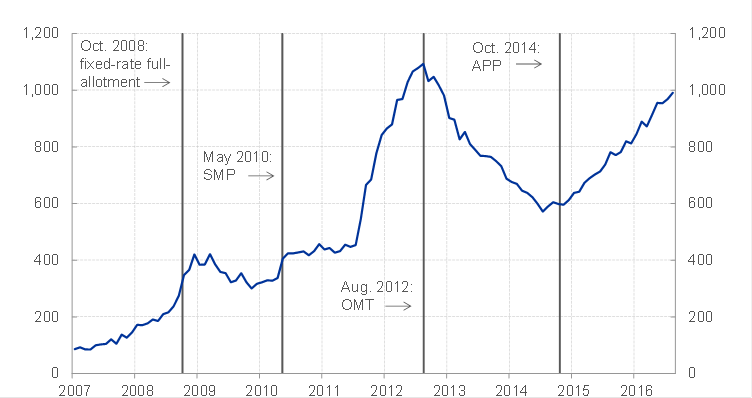

During the crisis which started in 2007 and especially around mid-2011, TARGET2 liabilities of some National Central Banks (NCBs) of the Eurosystem increased drastically (chart below) and led to heated discussion among economists and became a political subject.

Recently, the (im)balance has been increasing again but it seems that it’s mostly because of what some call QE recycling.

Peter Praet, Member of the Executive Board of the ECB explained this in his speech yesterday.

First the chart from his talk:

Sum of all positive TARGET2 balances. Source: ECB.

As Praet shows using T-accounts, what happens if Banco de España purchases securities from a German counterparty, Bundesbank’s TARGET2 assets—claims on the rest of the Eurosystem—will rise and so will Banco de España’s TARGET2 liabilities to the rest of the Eurosystem.

Once the German counterparty sells the securities to Banco de España, it will try to find the nearest substitute which may not be a Spanish security. So this is nothing to be worried about unlike earlier where TARGET2 balances were symptomatic of capital flight from some countries threatening financial meltdown.

Of course one has to be careful. Not all the recent rise may be attributed to the QE effect. But at the same time this analysis should throw some light on the topic.

This is a continuation of the post from the end of 2014, although reading that isn’t necessary.

In a new paper, Marc Lavoie continues his debate with Sergio Cesaratto on whether the Euro Area crisis is a balance-of-payments crisis or not. For the sake of completeness, here’s the list of papers, with references copy-pasted from Marc’s latest paper. Not all links are final versions and some may not be available to read in full).

Cesaratto, S. 2013. “The Implications of TARGET2 in the European Balance of payments Crisis and Beyond.” European Journal of Economics and Economic Policy: Intervention 10, no. 3: 359–382. link

Lavoie, M. 2015. “The Eurozone: Similarities to and Differences from Keynes’s Plan.” International Journal of Political Economy 44, no. 1 (Spring): 3–17. link

Cesaratto, S. 2015. “Balance of Payments or Monetary Sovereignty?. In Search of the EMU’s Original Sin–Comments on Marc Lavoie’s The Eurozone: Similarities to and Differences from Keynes’s Plan.” International Journal of Political Economy 44, no. 2: 142–156. link

Lavoie, M. 2015. “The Eurozone Crisis: A Balance-of-Payments Problem or a Crisis Due to a Flawed Monetary Design?” International Journal of Political Economy 44, no. 2: 157-160. (abstract)

As mentioned in my part 1, referred to on top of this post, I agree with Sergio Cesaratto.

Sergio Cesaratto with Marc Lavoie (picture credit: Matias Vernengo)

Marc Lavoie’s main point in the final paper seems to be that, “Eurozone countries can never run out of TARGET2 balances, which can take unlimited negative values, so that the evolution of the balance of payments cannot be the source of the crisis”.

This is not accurate in my view. Although the rules of the Eurosystem allow unlimited and uncollateralized credit facility between the Euro Area NCBs and the ECB, one has to look at the counterpart to the T2 imbalances. If an economic unit transfers funds across border from country A to country B, this first results in a reduction of balances of banks in country A at their NCB and may result in an intraday overdraft (“daylight overdraft” in U.S. language), usage of the marginal lending facility with the NCB, an MRO, or an LTRO and finally ELA in late stages of a crisis (if capital outflow is large).

Marc himself mentions this point in his latest paper:

If a Eurozone country is running a current account deficit that banks from other Eurozone members decline to finance, or if it is subjected to capital outflows, then all that happens is that the national central bank of that country will be accumulating TARGET2 debit balances at the ECB. There is no legal limit to these debit balances. The national central bank with the debit balances, which pay interest at the target interest rate, has as a counterpart in its assets the advances that it must make to its national commercial banks at that same target interest rate. And the commercial banks can obtain central bank advances as long as they show proper collateral. Why would the size of current account deficits or TARGET2 debit balances worry speculators? There might be a problem with the quality of the loans that have been granted by the banks, or with the size of the government debt, but that as such has nothing directly to do with a balance-of-payments problem.

[italics: mine]

But that is the case! It’s because of balance-of-payments. Nations who had high indebtedness to the rest of the Euro Area saw more capital flight. This is because in times of crisis, there is a home bias and international investors are likely to sell securities abroad and repatriate funds home. Large current account imbalances lead to a large negative net international investment position. (It’s of course also true that revaluations are important, and this is what happened in the case of Ireland). So when non-residents sell securities to domestic investors, banks are likely to get into a bad situation because they have to accommodate these transfer of funds and are losing central bank balances on a large scale.

It is precisely nations which had worse net international investment positions which were affected as charted in my previous post on this.

Now moving on to definitions: what is a balance-of-payments problem? The simplest definition is the problem for residents in obtaining finance from non-residents. Greece precisely has been struggling to obtain funds from non-residents.

So I do not agree with Marc’s view that:

Cesaratto, as others, is adamant that the Eurozone crisis is a balance-of-payments crisis, whereas I believe, as others do, that this is a side issue.

Marc Lavoie also says that the people arguing for this view are implicitly assuming some kind of “excess saving” view on all this:

In discussions with colleagues who support a “current account deficit” view of the Eurozone crisis, I sometimes get the impression that they are also endorsing a kind of “excess saving” view of the economy. They tell me that current accounts deficits are unsustainable within the Eurozone because the core Eurozone countries will refuse to lend to the periphery and will thus prevent these countries from financing economic activity. This seems wrong to me.

I disagree with this. It’s precisely because residents’ liabilities are large compared to their financial assets that they have to rely on non-residents/foreigners. And during the crisis a lot of capital outflow has happened and this precisely shows that non-resident private investors are unwilling to lend again on the same scale as before. This obviously means that to obtain finance, governments of nations affected have to take the help of the official sector abroad, such as from governments, the ECB and the IMF. If TARGET2 alone could do the trick, is the Greek government foolish to go abroad?

It is of course true that the design of the Euro Area was faulty. But that still leaves open the question about why Germany is not facing a crisis as severe as Greece. The design view cannot explain this. Any country (or all countries) in the Euro Area could have faced a crisis. There is a pattern here and that is where balance-of-payments comes in.

This debate is an interesting one. Both Sergio Cesaratto and Marc Lavoie agree on almost everything, except this BIG thing.

Of course this also spills over to policy proposals. Marc Lavoie believes that the European Central Bank can guarantee that all nations can have independent fiscal policies (by promising to buy all government debt which the financial markets isn’t interested in purchasing). Sergio Cesaratto is clear on this (and I agree very much) – in another paper Alternative Interpretation of a Stateless Currency Crisis:

A more resolute role of the ECB as lender of last resort accompanied by fine-tuned expansionary fiscal policies can only be imagined in a different political and institutional framework, quite close to that of a political union.

Let’s consider what happens if there is no federal government and if the ECB is the main supranational authority (ignoring other supranational institutions which have limited powers). Suppose the ECB were to guarantee the debt of governments of all Euro Area nations. There’s nothing to prevent, say, the government of Finland to increase the compensation of its employees every year by a huge percentage and thereby affecting Finnish corporations’ compensation of its employees. This will result in a reduction of competitiveness of Finnish producers and Finnish resident economic units will rely more on goods and services produced abroad. This will raise Finland’s net indebtedness to the rest of the Euro Area and the world. If someone believes that this debt is not a problem, how about the inflationary impact of this rise in demand on the rest of the Euro Area?

So the solution lies in bringing down the balance-of-payments imbalances (both negative and positive ones such as that of Germany). This requires a supranational institution, which is a central government. National governments would have rules on their budgets but the central government — since its goals and objectives are different — wouldn’t be bound by any rules. Wage rises would need to be coordinated. And as I argue in this post, fiscal transfers also plays a role of keeping imbalances in check.

Of course there are many other economists who also argue that the Euro Area problem is a balance-of-payments problem, but with a different motive. Their argument is to blame the nations in crisis instead of taking a humanist approach.

To summarize, the Euro Area problem wouldn’t have been a balance-of-payments problem had the official sector promised to act as a lender of the last resort to national Euro Area governments without any condition. As long as there are conditions, it is a balance-of-payments problem. One cannot pretend that the European Central Bank has or can be given such powers to lend without any condition. And hence the Euro Area crisis is a balance-of-payments problem.

In a recent article for VOX, Paul De Grauwe and Yuemei Ji write about potential fiscal effects of a possible asset purchase program by the Eurosystem (European Central Bank and the National Central Banks in the Euro Area). In that the authors take an extreme stand suggesting that a default by a Euro Area government on bonds held by the Eurosystem doesn’t even matter.

JKH has written a fantastic critique of the VOX article by De Grauwe and Ji.

JKH says:

De Grauwe goes on to say that because bonds held by the ECB –defaulted or otherwise – are “eliminated” on consolidation, it doesn’t matter what they were valued at on the ECB balance sheet in the first place. They may as well have been valued at zero – because they have effectively been eliminated and replaced by ECB liabilities (assumed by implication to be permanently interest free).

…

Thus, the balance sheet implication of De Grauwe’s treatment is that some portion of future currency issued by the ECB will be “backed” on its own balance sheet by an asset of zero value – the defaulted Italian bond. The problem is that this currency would have been issued in any event according to the demand that will arise naturally from the growth of the European economy over time (notwithstanding current depressed conditions). And so ECB seigniorage will have been reduced from what it would have been had it included the effect of good interest on Italian bonds. That reduction in seigniorage due to default is a real fiscal cost, because it reduces the profit remittance of the ECB from what it would have been in the non-default counterfactual. And the fact that the reduced seigniorage gets distributed to the residual capital holders means that there has been a fiscal transfer to the defaulting sovereign from the remaining capital holders. So De Grauwe is simply wrong on this point.

Another way to look at it is by looking at the international investment position. A default by a nonresident on a claim on held by residents is a reduction in the net international investment position and a reduction in the wealth of the geographic region. (The wealth of a nation is the sum of the value of its non-financial assets plus the net international investment position). International investment position matters as a sounder position implies that there is higher potential to raise output.

De Grauwe has another article for The Economist from today. He writes:

Since Milton Friedman we have all become monetarists. In order to raise inflation it will be necessary to increase the growth rate of the money stock. This requires that the ECB increase the money base. And to achieve the latter there is only one practical instrument, ie, an open-market purchase of government bonds. There is no other way to raise inflation than through an increase in the money base and a bond-buying programme is the time-tested way to achieve this.

It is sad that Monetarism is still alive today, despite being repeatedly been shown to be incorrect. But more importantly for the current discussion about risks, De Grauwe repeats his stand again and states it more explicitly:

This confusion between accounting losses and real losses is unfortunate. It has led to long hesitation to act. It also leads to bad ideas and wrong proposals.

So losses do not even matter!

The problem with a Eurosystem asset purchase program of Euro Area government bonds is that it achieves little. It is not a coordinated Euro Area wide fiscal expansion which is badly needed. The ECB already has the OMT program which has helped government bond yields from rising and leading to a crisis, so a QE will hardly achieve much except having an impact on prices of financial market securities. QE just diverts attention from important challenges for a unified Europe. Challenges such as how to move toward the formation of a central government.

So Karl Whelan wrote another article on TARGET2 claiming once more that a loss of TARGET2 claims of the Bundesbank does not matter at all to Germany. He has a new paper as well. Earlier he was arguing there was no loss at all.

His argument roughly is that since there is no longer trade settlement in gold, money is thence fiat and the loss does not matter.

Closed economy monetary economics is confusing enough for most monetary economists but when matters of open economy are discussed, it is a Herculean task for them to make sense of simple things. Some economists are better but end up making a mess.

First there is this story of “fiat money”. Supposedly after 1973 – when the Smithsonian Agreement broke down – money or currencies became fiat according to many theories. I guess this is generally the notion made popular by Austrian economists as far as I can tell and (is the root of all evil in this story). But this is strange. If “fiat money” has any meaning to it, money was equally fiat before – either during the Bretton Woods system or in any monetary institutional setups before that. So the US Dollar was as fiat as in 1920 as in 2012. There’s no meaning to saying that currencies became fiat suddenly.

Of course, in the Bretton Woods system, nations’ governments were required to redeem official foreign balances either in gold (till 1968), SDRs (after 1968) or in the currency of the member making the request (if any). In addition, there was a system of market convertibility in addition to official convertibility. In addition, the US volunteered to convert official foreign balances to gold till 1971.

So one could say that international trade was settled in gold. However, since money is credit, international trade would also settle by borrowing from foreigners – not just the official sector borrowing but other resident sectors borrowing from foreigners. The proper way to understand this is to study how balance of payments accounting is done and it was no different now than what it used to be.

A nation which runs a trade deficit need not lose gold reserves because the current account deficit could be financed via the financial account. If there is a problem in inflow, changes in interest rates by the central bank would attract funds from foreign financial centers.

More generally as always, it is income changes which works to bring imbalances back to balance. Sometimes things get out of hand, leading to a loss of gold reserves and the need for international financial help for exceptional financing of the balance of payments. But even in the supposedly new fiat world, things can get out of hand and require exceptional financing transactions.

Before Bretton Woods, nations had less formal agreements and typically the central bank and/or the government would promise to convert currency notes into gold at the request of the holder and not just official balances. It was thought that this made currencies acceptable and that the central bank should not issue more currency notes than the amount of gold they held. This story however, has no empirical support. It was however thought that the amount of currency notes is some multiple of the amount of gold and perhaps this is the origin of the story of the multiplier. But this is a troublesome story and there is some sort of view that money is exogenous in such monetary setups but endogenous otherwise – which makes no sense at all. Money is always credit-led and demand-determined and hence endogenous.

[To be more complete, some nations do not have a legal tender of their own and use other currencies as per law]

Now, economists argued that in the era of fixed exchange rates, an outflow of gold would lead to an automatic contraction of the money stock – the underlying theory being that of the money multiplier. This is presented as the Mundell-Fleming approach. Wages would reduce and this will lead to more competitiveness in international markets and bring the trade imbalance back into balance. This didn’t work because the whole notion was based on ideas of the money multiplier and notions such as that. (In addition it ignores the crucial aspect of non-price competitiveness).

So Emperor’s New Clothes – economists figured that floating exchanges would do the trick. Even a great economist such as Nicholas Kaldor believed so (while he was warning about troubles with the Bretton Woods system in the 1960s) but he was the first to point out that it doesn’t do the trick – soon in the 1970s.

More troublesome is the notion that if a nation is indebteded to foreigners in the domestic currency, it doesn’t owe foreigners anything and that this debt is just technical. The reason given is that nations are relieved to convert balances of foreign governments and/or central banks in the new era (the ones floating their exchange rates). But this is highly mistaken. While it is untrue (official convertibility still exists), it ignores the more important concept of market convertibility. The “reason” is dubious. It is true that it doesn’t cost the central bank anything if banks ask for currency notes to satisfy the demand for their customers, it doesn’t mean much. The private sector net wealth and aggregate demand is affected by net government expenditures and precisely when the nation has a balance of payments crisis, does the government have less power. It however is useful to have the government to make expenditures and take other emergency actions to handle a crisis in the external sector (with the exception of governments in a monetary union and nations which have “dollarization”). Debt denominated in domestic currency is useful for another reason. Assuming foreigners do not repatriate funds abroad when the currency is depreciating, it prevents a revaluation loss on liabilities. Indebtednesss in foreign currency on the other hand, leads to revaluation losses – implying more is needed from export receipts to prevent the debt from getting out of hand.

The fact that in any monetary setup nations face a balance of payments constraint has led nations to grow via success in international trade. Those who understood this trick early gained market and their success led to more success. This in turn puts a handicap on the rest of the world. The ‘mercantalist’ nations while didn’t believe the invisible hand (according to Keynes) nevertheless gain tremendously from the present system of free trade. As long as free trade is maintained, it is advantageous to nations to have strong external positions – in trade and in claims held on foreigners.

Now to the paper of Karl Whelan.

For Whelan, the external assets of a nation – including the claims of the government on non-residents – does not matter at all.

When considering the loss of the Bundesbank’s TARGET2 claim, it is important to distinguish between implications that matter and those that don’t. Most of the commentary on this issue has focused on implications for the Bundesbank itself and the need for a hugely costly recapitalisation of the central bank. For example, Burda (2012) argues that “Germany has now become a hostage to the monetary union, since a unilateral exit would imply a new central bank with negative equity.” However, there are a number of reasons why the capital position of the central bank is something of a red herring when considering a break-up scenario.

The first reason for this is that despite the common belief that central banks need to have assets that exceed their notional liabilities, there is no concrete basis for this position. Systems like the Gold Standard required a central bank to “back” the money in circulation with a specific asset but there is no such requirement when operating a modern fiat currency. A central bank operating a fiat currency could have assets that fall below the value of the money it has issued – the balance sheet could show it to be “insolvent” – without having an impact on the value of the currency in circulation. A fiat currency’s value, its real purchasing power, is determined by how much money has been supplied and the factors influencing money demand, not by the central bank’s stock of assets. As discussed in the attached box, close examination reveals little merit to the various arguments that are put forward for the idea that a central bank must have positive capital to achieve its goals.

The second reason the focus on central bank capital is a red herring is that, even if it is decided after a break-up that Germany must recapitalise the Bundesbank, rather than being hugely costly, this recapitalisation would have no impact on either the net asset position of the German state or its budget deficit. Let’s assume the German government recapitalises the Bundesbank by providing it with an interest-bearing government bond. While the government’s gross debt will increase, the government bond becomes an asset of the Bundesbank, so the total public net debt does not change.

Similarly, suppose the new debt provides interest payments of €3.9 billion (equal to the annual interest that would be generated by the September 2012 level of Bundesbank net Intra-Eurosystem claims). This payment would raise the profits of the Bundesbank by this amount, thus raising the amount the Bundesbank can return to the German government by the same amount, resulting in no change in the budget deficit.

So the issue facing Germany in case of a loss of its Intra-Eurosystem claims is not the insolvency of the Bundesbank or the costs associated with recapitalising it. The real issue is simply that the Bundesbank had a large asset and this asset will have disappeared. Still, despite the eye-popping level of the Bundesbank’s TARGET2 claim, the disappearance of the net income from the Intra-Eurosystem claims would have a very modest impact on the annual German budget. At an interest rate of 0.75 percent, the yield of €3.9 billion on the net Intra-Eurosystem claims of €516 billion as of the end of September represents only 0.15 percent of German GDP. Rather than a huge potential loss keeping Germany hostage within the Eurozone, I suspect this is a loss than many Germans would shrug off as perhaps being smaller than the likely costs associated with the sovereign bailout funds aimed at saving the euro.

Although Whelan accepts there is a loss (although he wasn’t earlier), there is hodge-podge here in the whole write-up. Whether there is gold involved in settlement of international debt or if the government promises to convert currency notes into gold (to keep its currency acceptable and which is just an illusion in any case) is an entirely irrelevant issue. The potential of a loss of huge amounts (given that a panic can lead to further losses for the German public sector – to see how see this post) is dreadful to Germany. The seigniorage calculation is hardly useful. It is like telling someone that a $1m loss doesn’t matter because it only earns $2,500 per year – given current interest rates. His point that there is “no change in the budget deficit” if Bundesbank’s foreign assets get replaced by German government debt has a simple calculation mistake – in one case the public sector is receiving interest income from abroad and in the other it isn’t.

(Apologies for misspelling Whelan earlier in some places in earlier version)

The financial and non-financial resources at the disposal of an institutional unit or sector shown in the balance sheet provide an indicator of economic status. These resources are summarized in the balancing item, net worth. Net worth is defined as the value of all the assets owned by an institutional unit or sector less the value of all its outstanding liabilities. For the economy as a whole, the balance sheet shows the sum of non-financial assets and net claims on the rest of the world. This sum is often referred to as national wealth.

This paper was aimed at Hans-Werner Sinn who started ringing alarm bells on the huge TARGET2 claims of the Deutsche Bundesbank. The claim of this post (and some more in the past in this blog) is that while Prof Sinn may be wrong on many issues in the debate, he is right about a few important issues. Needless to say, his prescriptions are not defended by me. I am a fan of Nicholas Kaldor’s ideas as quoted in my post Nicholas Kaldor On The Common Market.

De Grauwe’s argument is slightly more nuanced that others such as Karl Whelan. While Whelan dismisses any argument that a loss of creditor nations’ TARGET2 claims on the periphery Euro Area nations is a loss, De Grauwe modifies this to say that the repatriation of funds by Germans (individual investors and institutions) does not increase Germany’s risks.

So we have this claim in his paper:

Thus the increase in the Target2 claims of the Bundesbank should not be interpreted as an increase of foreign claims of Germany, and thus as an increase of risk from higher foreign exposure. Using the Target claims as a measure of risk incurred by the German population is therefore erroneous. As we have seen earlier, after 2010, the Target claims of Germany (and other Northern countries) increased dramatically and much more than the current account surpluses during this period. This increase in Target2 claims cannot be interpreted as an increase in the foreign exposure (net foreign claims) of Germany, except to the extent that they were the result of current account surpluses. What changed dramatically is the nature of these claims. Prior to 2010, these claims were mainly claims held by private German agents (mainly financial institutions). Similarly the liabilities of the peripheral countries were held by private agents (financial institutions). The eurozone crisis led to a dramatic shift. As a result of the breakdown of the interbank market, a large part of these private claims and liabilities were transformed into (public) Target claims and liabilities (Buiter et al., 2011), without however changing the total net foreign claims and liabilities of these countries. Thus, the explosion of the Target claims of Germany since 2010 cannot be interpreted as an explosion of the risk of foreign exposure for Germany.

Ignoring the fact that the repatriation of funds by German residents back to Germany puts the risks on the public sector’s books and awards the (ex-) German lender, there is some element of truth to the above claim. The repatriation of funds does not increase Germany’s gross international investment position (assets and liabilities) but just changes the composition. It however ignores the fact that nonresidents also reallocate their portfolios in German assets and this increases Germany’s gross foreign assets and liabilities and in case there is a default by the periphery on the TARGET2 liabilities (in case they leave the Euro Area), Germany suffers a loss. We will see this with an example below. Before that let me highlight one misleading claim in the paper:

The value of the money base is exclusively determined by its purchasing power in terms of goods and services. This value is independent of the value of the assets held by the central bank. In fact in the fiat money system we live in, the central bank could literally destroy the assets without any effect on the value of the money base. In order to stabilize the value of the money base, the central bank should keep the right supply of money base, i.e. a supply that will maintain price stability.

That is Monetarist handwaving. Won’t say anything further!

When the central bank acquires assets, mainly government bonds, it issues new liabilities. The latter take the place of the government bonds in the portfolios of private agents. It is as if the government debt has disappeared. It has been replaced by central bank debt. The central bank could literally put the government bonds in the shredding machine. This would not affect the value of the central bank debt as the central bank has made no promise to redeem its debt (money base) into government bonds. And as long as the central bank maintains price stability, agents will willingly hold the new debt (money base) issued by the central bank.

That is incorrect. The People’s Bank of China cannot shred US Treasuries into a dustbin and claim it does not matter to the Chinese people.

Now to the main point about this post: foreigners shifting funds into assets issued by German residents.

Here is from the Bundebank’s statistical supplement for Germany’s international investment position:

Aktiva is Assets, Passiva is Liabilities and Saldo is Net.

Germany’s assets and liabilities can increase as a result of a nonresident (such as from Spain) buying German Bunds (government bonds). If an institution in Spain liquidates its position in Spanish assets and transfers the funds to purchase Bunds, Bundebank’s TARGET2 claims will increase (in the current scenario).

Let us use these numbers to see how Germany’s IIP changes if there is a purchase of €100bn of German assets by German nonresidents (but residents in Euro Area for simplicity).

Initially,

Germany’s Assets = €6,843bn

(of which TARGET2 claims = €727bn)

Germany’s Liabilities = €5,829bn

NIIP = €1,014bn

Now assuming a nonresident purchases €100bn of German government bonds from a German resident,

Germany’s Assets = €6,943bn

(of which TARGET2 claims = €827bn)

Germany’s Liabilities = €5,929bn

NIIP = €1,014bn

So while Germany’s gross assets and liabilities have increased by €100bn, its net position is the same.

However this is not the end of the story. When nonresidents purchase €100bn worth of German securities, the TARGET2 claims of the Bundesbank (or more generally creditor nation’s TARGET2 claims) increases by €100bn. If there is breakup of the Euro Area position at this point in time, this will leave the creditor EA nations with an additional liability of €100bn (incurred just before the breakup) while at the same time losing the €100bn of assets (TARGET2) acquired (in addition to other assets) and hence an NIIP worse than the case if the transaction had not occurred.

This number can be much higher because when there are tensions building up in the financial markets, foreigners may shift funds into Germany and if a breakup really is forced upon the Euro Area, it will leave Germany with additional liabilities and a lower NIIP than before and a huge loss of wealth.

At any rate, a non-negligible part of the German international investment position can be due to foreigners already having shifted funds in German assets (as the gross assets and liabilities position indicates).

But De Grauwe claims (thanks to JKH for pointing):

It is surprising that these simple principles are not widely understood.

!

Recently, the ECB announced a plan which substantially reduces the risks of a breakup of the Euro Area. In the absence of a breakup, discussions such as these are purely academic. However, the story has new twists and turns, and one can never be sure what is going to happen. It is however counterproductive to claim there is no risk/loss (in select scenarios) when there is indeed one.

Needless to say this analysis is not a defense of the German position either. Free trade has helped them a lot and it is time they increase domestic demand and help reduce global imbalances.

As leaked earlier by Bloomberg, Mario Draghi in a press conference today, presented his big plan to save the world.

This will involve OMTs (Outright Monetary Transactions) – in which a Euro Area nation central government requesting aid from the EFSF/ESM will also be provided help by the ECB. Under this plan, when a nation’s government asks for financial aid (and a big if), the ECB/Eurosystem may buy government bonds in the open markets to bring the yields down.

The Eurosystem will buy bonds with maturities between one and three years and will accept credit risk on these bonds and will not ask for a seniority status in case of default. Of course, this will come with strict conditions – the government asking for aid would need to commit to a tighter fiscal policy and promise supply side reforms. There will be no upper limit to the amount of bonds purchased by the Eurosystem.

During the press conference (actually a bit before as well – after Bloomberg leaked a part of the plan), government bond yields had huge moves (e.g, Spanish ten year yields decreased 39bp). Now, if the yields do not reverse and deteriorate again soon, governments requiring help may just delay asking for aid. However, sooner or later bond yields may rise again – especially if foreigners holding the bonds start to get nervous.

My own view is that this plan significantly reduces the risk of an exit by a Euro Area member. Unlike previous plans (SMP, EFSF, ESM) this has no limit on the amount of funds needed. There is no need to wait for parliaments and courts to approve any transaction or aid.

Of course this is not a happy set of affairs. Forcing governments into retrenchment will lead to economic conditions deteriorating further. One however needs to realize that an independent fiscal policy for the troubled nations – while it (an expansion) increases national income and output – will have the adverse effect of deteriorating the balance of payments – resulting in the public debt and the nation’s net indebtedness to foreigners (and the latter is already high for troubled nations) rising without limit relative to output. The plan will look good in retrospect if it is supposed to be a bridge toward a political union with a central government.

")

{kind=link}