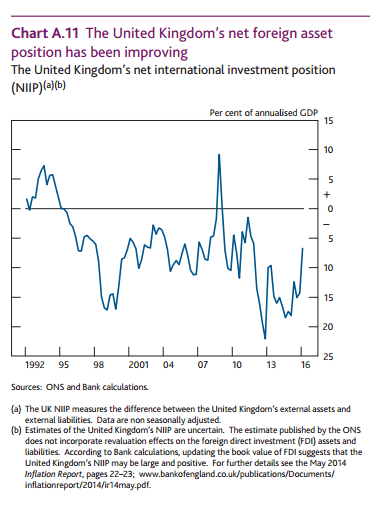

The Bank of England’s financial stability report from July has an interesting discussion on this with this chart.

UK’s net international position. Source: BOE.

with the comment:

The currency composition of the United Kingdom’s external balance sheet does not amplify risks associated with a sterling depreciation.

Currency mismatches in a country’s external balance sheet can amplify risks associated with a large current account deficit, if a depreciation of the currency leads to a deterioration of the external balance sheet position. Although there are no official statistics on the currency composition of the United Kingdom’s external balance sheet, estimates suggest that around 60% of the stock of external liabilities is denominated in foreign currency, compared with more than 90% of the stock of external assets. This means that, other things equal, a fall in the value of sterling should increase the value of external assets relative to liabilities, improving the United Kingdom’s net foreign asset position which was -6.7% of annualised GDP in 2016 Q1 (Chart A.11).

Of course, it is important to keep in mind that while this is true, large movements in liabilities in can affect corporations and systemic risks can arise if a large corporation fails. But at the same time, assuming risks are contained, the above is beneficial to the UK. Risks associated with Brexit and the fall in the value of the Sterling aren’t as bad as presented by economists 🤡 with the opinion that the UK should remain in the EU.

Ashoka Mody, a professor at Princeton and a scholar at Bruegel has a nice articleDon’t Believe What You’ve Read: The Plummeting Pound Sterling Is Good News For Britain for The Independent.

He argues that a lower value for the Sterling will help rebalance the UK 🇬🇧 economy. Mody says:

It is true that with an overvalued pound, the British public could command more foreign goods and services with their currency. But British producers lost competitiveness at home and abroad. Producers’ incentives to invest were weakened, leading to Britain’s poor productivity performance. And that led to a large current account deficit.

and also that:

[The] “elite” group continues to hold the microphones of policymaking and its words reverberate through the financial press. All these years, however, the strong pound hurt job creation and investment in productivity growth. And those who have long been hurt don’t live in London and don’t hold the microphones.

Ashoka Mody also wrote a highly readable and excellent piece EU referendum: Why The Economic Consensus On Brexit Is Flawed before the EU referendum, which you should still read if you didn’t earlier. It was one of the most important pieces in the media before the referendum. It argued how issues such as fiscal constraction aka austerity were sidelined in the debate.

The European Union is founded on the principles of free trade. Dean Baker has a nice blog post on his blog Beat The Press titled, The Value Of The Pound Is Not A Measure Of The Success Or Failure Of Brexit. In that, he comments on Friday’s fall in the exchange rate of the Sterling.

The fall has been claimed to be a failure of the UK 🇬🇧 exiting from the European Union. Dean Baker, although seems to side with the remain-in-the-EU camp, points out:

The Brexit vote was a case where the elites were clearly aligned against the UK leaving the European Union. While they had many good arguments on their side, and much of what the pro-Brexit crew was saying was nonsense, some of the elite gloating now also falls into the nonsense category.

The reason I say this is that he seems to think that there is no economic argument for leaving, while in my opinion, it is quite the opposite. Anyway, I really liked him saying that the elites were aligned against the non-elites. Unfortunately the UK far-right jumped on to this – arguing for exiting the European Union, and it made it easy for the neolibs to thrash arguments for leaving the European Union.

Anyway, the reason for the post is that there’s a frequent claim made around the UK’s current account deficit and the exchange rate in contrast to Baker who says:

Rather than being a negative for the economy, this is a positive development. It is the only plausible mechanism through which the UK can get closer to balanced trade.

Somewhat funnily, the neolibs whose arguments are about the magic of the “market mechanism” are making arguments similar to heterodox economists’ elasticity pessimism. According to the elasticity pessimism view income effects far outweigh the price effects and the market mechanism does not resolve imbalances in balance of payments. The elasticity pessimism view doesn’t claim that price effects do not matter at all.

But funnily, the anti-Brexit people seem to use this view since it suits their political purposes and what’s interesting is that even taking the view that price effects aren’t there! So they are claiming that the exchange rate movement can’t improve the UK balance of payments. Now an analysis of how much exchange rate movements have affected the UK’s exports and imports is difficult but instead of taking an empirical approach, let me make some theoretical arguments.

The claim is that wide movement of exchange rates hasn’t improved the UK current account balance. But that doesn’t mean it doesn’t matter. It just means that the income effects have far outweighed price effects. The depreciation of the Sterling should help the UK. To illustrate my point imagine this (numbers are just for illustration, aren’t actual):

Scenario: The UK current account deficit rises from 7% of GDP in 2016 to 8% of GDP in 2017.

This 1% rise might be explained by:

1.3% due to income effects: i.e. change in GNI at home and abroad, changes in non-price competitiveness.

minus 0.3% due to price effects i.e., changes in the exchange rate and changes in price competitiveness.

So just superficially looking at empirical data might lead us to conclude that the fall in the exchange rate of the Sterling has had no improvement, but that’s not the case. The fall has helped but income effects have outweighed. If the exchange rate hadn’t changed, the current account deficit would have risen to 8.3% of GDP.

But if the UK current account balance of payments doesn’t improve, what is the point of all this you may ask. Well, for one a depreciated exchange rate helps at the margin but the more important effects—which depend on trade negotiations—tariffs etc, would depend on how the UK government manages to help its domestic industry and improve its non-price competitiveness. Leaving the EU would also mean that the UK regulates migration and this would help improve wages, employment and output.

It’s an extreme view that price effects do not matter. China, for example has a highly undervalued exchange rate obtained by official management by PBOC, China’s central bank. Elasticity pessimists do not think that price effects do not matter, only that income effects matter more typically and that the market mechanism does not resolve imbalances. Elasticity pessimism is not an extreme view but it is ironic to see the neolibs who have argue in favour of a common market to take an extremized version of the elasticity pessimism view.

There is even more irony in this. Not joining the European Union was a respectable view in the 70s when Nicholas Kaldor used to argue against joining the EU. But in recent times, it has been hijacked by the nationalists making it easier for neoliberals to claim victory. They just have to argue how the nationalists are wrong (which is true) but it doesn’t mean that the neoliberal project is correct.

Lastly, does it not matter if a currency has a run. Of course it does matter. Just that the Sterling’s fall can’t be called that and the UK is not really in danger because of the fall in the exchange rate. There are no expectations building around the Sterling like what happens to third-world nations’ currencies many times.

In this interview (linked below) with The New York Times, Joseph Stiglitz points out the response of the EU to the UK EU referendum vote and its authoritarianism. He says that after the Brexit vote, Jean-Claude Juncker, who is the President of the European Union said that the EU will act tough on the UK to make sure other European Union members do not leave. Stiglitz then says that you want to believe that people want to stay in the EU because it brings benefits to them but, no, that is not the way Juncker is thinking. He wants people to stay because of fear and is issuing a threat.

click the picture to see the video on NYT’s Facebook page.

Discussion around 19:00

Another important point Stiglitz makes about the Euro Area is about a system of progressive taxation. This point is often less discussed. If France raises taxes, it makes it easier for economic units to move to another place inside the Euro Area and hence it is difficult to create a system of progressive taxation.

I find it disappointing that many heterodox economists support the European Union. Will the Juncker threat make them realize?

In this interview, Steve Keen talks of Europe post the UK EU Referendum (“Brexit”).

Steve Keen talks of various things such as the importance of manufacturing etc. In the first four minutes, he also refers to Wynne Godley’s 1992 LRB articleMaastricht And All That.

click the picture to see the video on MoneyWeek’s website.

Nice interview.

A few complaints. Although Steve Keen is correct about the importance of debt, he is still holding on to his equation, “aggregate demand = gdp + change in debt”. Also in the interview Keen talks of quantitative easing is about banks selling bonds to the Fed. Although banks in their role as primary dealers do sell the bonds to the Federal Reserve, the counterfactual is not banks holding all the bonds.

I also do not believe in debt jubilees (except in exceptional case such as farmers with huge debt in India). Debt jubilee is unfair to the people who didn’t go into debt. Good initiatives are things such as forgiving medical debt as done by John Oliver.

The commentary after the EU Referendum has moved into a consensus from economists claiming that “Brexit” will make the UK poorer. So we hear it from Paul Krugman:

Yes, Brexit will make Britain poorer

Krugman’s thoughts are also echoed by Simon-Wren Lewis. First SWL claims that:

Calculating the size of this effect is an exercise in trade economics not macroeconomics

I don’t understand this. Calculation is both an exercise in trade economics and macroeconomics. So in stock-flow consistent models of the open economy, you see such a thing. It’s both macroeconomics and trade. Trade is automatically incorporated in a macroeconomic model.

This is not just a minor point in semantics. In stock-flow-consistent models, one cannot avoid some parts and talk of the rest. One is forced to incorporate trade, not just in goods and services but also financial assets. Something which models which SWL uses isn’t sophisticated enough to handle.

Moving on, SWL claims that the UK’s exit from the EU makes the UK poorer. He says:

This decline in trade leads to a loss in productivity which makes UK citizens poorer over the medium term. It also means that the real value of sterling has to fall to make up for the fall in net exports. Other things being equal, this fall in sterling will happen immediately, as indeed it already has. This will make people poorer immediately, because imported goods cost more. But here the macroeconomics gets complicated. The hit to trade from leaving the single market will evolve gradually, but the fall in sterling is immediate. (The reason is something economists call UIP.) That means that trading firms might get a short term competitiveness boost, even though this will evaporate in the medium term. This may or may not be enough to compensate for the short term impact of rising prices on consumption spending.

Unfortunately that is not all that happens in the short term. Uncertainty about future arrangements will hold back investment, and it may also add to the depreciation in sterling. For this and other reasons the short term impact on aggregate demand is likely to be negative, although measuring its size is difficult. We then need to think about whether the MPC will raise or cut interest rates. The National Institute’s analysis is very readable on all this.

[underlying: mine]

So the claim that it will make the UK poorer. In effect, SWL’s model is telling him that real GDP will fall as well as real wealth as well fall in real household expenditure. There are several ways in which it happens. Productivity falls. Fall in productivity leads to a less than rapid increase in production. Consumer prices rising means lower real expenditure and so on.

Now, in Kaldorian story the causalities in the real story of actual economic dynamics are almost reverse than the ones presented above. Faced will less free trade, the UK government is less constrained to expand domestic demand and output. It can protect its manufacturing industry. Rising production leads to rising productivity, reverse of what is implied by SWL’s model. True, imported goods will be costlier, but it also reduces import penetration which allows domestic demand to be expanded and hence output and hence real national income and household income so that consumers are more than compensated for imports being made more expensive.

Of course, all this depends on whether the UK government reduces austerity and expands domestic demand. But some effects can be seen, although uncertain. This is because the foreign trade multiplier is improving and the fiscal policy multiplier improves, even if the fiscal stance is not changed. Higher wages if immigration is controlled also provides a boost to demand.

At any rate, the important point in this post is that the remain campaign’s economics is a model which is completely erroneous about causalities and how economies work.

In the previous post, I highlighted Nicholas Kaldor’s view on the EU. I want to quote Wynne Godley’s views as well. Wynne Godley was highly influenced by Nicholas Kaldor so it is not surprising his views were similar.

In an article Wynne Godley Asks If Britain Will Have To Withdraw From Europe, written for London Review Of Books, written in October 1979, Godley writes:

The implications for Britain of EEC membership are rapidly becoming so perversely disadvantageous that either a major change in existing arrangements must be made or we shall have, somehow, to withdraw.

I strongly support the idea of Britain’s membership of the Common Market for political and cultural reasons. I would also support co-ordinated economic policies which were mutually advantageous to all the member countries. But this is not what we have got at the moment.

…

So we are all to be losers. The taxpayer through the Budget contribution, the consumer through higher food prices, the farmer through costs rising more than selling prices, and the manufacturer through rapidly rising import penetration.

…

… And if we may also take into account the dynamic effects, our balance of payments would be better by several thousand million pounds than it is at present. This would by itself have had a favourable effect on real national income and output, but, more important, it would have enabled the Government to pursue a less restrictive fiscal and monetary policy. According to preliminary estimates, the real national income could have been at least 10 per cent higher than at present and the rate of price inflation several points lower than if we had never joined the EEC.

It’s the United Kingdom European Union membership referendum tomorrow. In my opinion, the UK should leave the EU.

When discussing the Euro Area, it is emphasized frequently that Euro Area governments do not have the power to make expenditures by making drafts at the central bank as argued by Wynne Godley in 1992:

It needs to be emphasised at the start that the establishment of a single currency in the EC would indeed bring to an end the sovereignty of its component nations and their power to take independent action on major issues. As Mr Tim Congdon has argued very cogently, the power to issue its own money, to make drafts on its own central bank, is the main thing which defines national independence. If a country gives up or loses this power, it acquires the status of a local authority or colony. Local authorities and regions obviously cannot devalue. But they also lose the power to finance deficits through money creation while other methods of raising finance are subject to central regulation. Nor can they change interest rates.

The Euro Area was formed because Europeans wanted to come together and create a union which is big and powerful enough to be not affected by financial markets. The original intent was right but soon the whole idea came to be influenced by neoliberalism. The thing which was hugely missing (“the incredible lacuna” in Wynne Godley’s words in the above cited article) was the absence of central government of the Euro Area itself, which will have the power to collect taxes from Euro Area economic units and make expenditures. After some years of boom, the Euro Area found itself in crisis and could not deal with it well because there was no central government and fiscal policy to the rescue. The European Central Bank tried to save the monetary union but isn’t as powerful enough as a central government. More importantly, the Euro Area was brought into existence with the idea of free trade. Not only was power taken away from relatively economically weaker nations such as Greece but free trade was imposed by bringing their producers compete in the common market. In summary, there were two reasons why some Euro Area nations suffered.

The monetary arrangement

The common market.

Typically the former is emphasized more than the latter. Perhaps the reason is simple. It is easier to explain the former than the latter. In my experience, the latter is more difficult for people to understand and appreciate. Very few have emphasized it. Few exceptions are: Nicholas Kaldor, Wynne Godley.

Because economic growth is “balance of payments constrained”, free trade is devastating. The Euro Area could have had free trade if it had a central government which keeps imbalances in check because of fiscal transfers and regional policies.

Which brings us to the European Union itself and Britain’s membership. Although the UK government neither didn’t surrendered its sovereignty to make drafts at the central bank nor irrevocably fix the exchange rate in 1999, the nations’ producers still compete in the common market. It is better off leaving the European Union and have powers to impose tariffs on imports. Free trade is destructive to trade and one needs a lot of protection – at least the power of the optionality to impose such things any time a nation needs.

It was surpising to see less heterodox noise on this.

Nicholas Kaldor wrote a lot on this in the 1970s before the United Kingdom European Communities membership referendum in 1975. In his Collected Economics Essays, Volume 7, Nicky wrote (Introduction, page xxvi, October 1977) :

The final section of this volume, Part III, reproduces papers written in the course of the “Great Debate” on the question of British Membership of the Common Market in 1970 and 1971, and includes as a postscript a lecture on Free Trade written in 1977. As this debate came to an end when Britain entered the market, a decision which was later confirmed in popular referendum with a 2:1 majority, the reproduction of these papers may strike as otiose and serving little purpose other than somewhat ignoble one of self-vindication in the eyes of future historians. However, if the long-run effects of our membership turn out to be as disastrous as I feared they would be in 1971—and nothing that has happened has caused me to change my views—I think it is of the utmost importance that the true arguments against membership should be accessible to successive generations of students, the more so since the political debate continues to be dominated by issues (such as our effects of membership on the cost of food, on our agriculture, or the net budgetary cost of membership) which I regard as secondary and which could be brushed aside if the long-run effects on Britain’s manufacturing industry and on our capacity to provide employment were favourable.

…

[page xxviii] … the last essay of this volume, “The Nemesis of Free Trade”, which recounts the arguments in the great debate on Free Trade and Protection conducted at the beginning of this century between Herbert Asquith and Joseph Chamberlain. The points made on both sides seem to have lost none of their freshness or relevance in the intervening years. What has changed is our freedom to act. In 1905 we were free to decide whether to continue with the policy of free imports or to protect our industries. In 1977 the choice is no longer open to us, except at a political cost of withdrawing from the Common Market, an act which few people would contemplate seriously so soon after accession.

But after so many years, here is the chance to undo all this and withdraw from the EU. The UK should leave the EU.