Recently I commented on a paper, The Financial Crisis In The Eurozone: A Balance-Of-Payments Crisis With A Single Currency? by Eladio Febrero, Jorge Uxó and Fernando Bermejo, published in ROKE, Review Of Keynesian Economics. I hadn’t realised that Sergio Cesaratto has a reply (paywalled) in the same issue.

Sergio Cesaratto. Picture credit: La Città Futura, Sergio Cesaratto

Abstract:

Febrero et al. (2018) criticise the balance-of-payments (BoP) view of the European Economic and Monetary Union (EMU) crisis. I have no major objections to most of the single aspects of the crisis pointed out by these authors, except that they appear to underline specific sides of the EMU crisis, while missing a unifying and realistic explanation. Specific semi-automatic mechanisms differentiate a BoP crisis in a currency union from a traditional one. Unfortunately, these mechanisms give Febrero et al. the illusion that a BoP crisis in a currency union is impossible. My conclusion is that an interpretation of the eurozone’s troubles as a BoP crisis provides a more consistent framework. The debate has some relevance for the policy prescriptions to solve the eurocrisis. Given the costs that all sides would incur if the currency union were to break up, austerity policies are still seen by European politicians as a tolerable price to pay to keep foreign imbalances at bay – with the sweetener of some European Central Bank (ECB) support, for as long as Berlin allows the ECB to provide it.

Sergio carefully responds to all views of Febrero et al. and Marc Lavoie, Randall Wray and also Paul De Grauwe, pointing out that he agrees with most of their views except that their dismissal of this being a balance-of-payments crisis with their claims that the problem could have been addressed by the Eurosystem/ECB lending to governments without limits. He points out that, “The austerity measures that accompanied the ECB’s more proactive stance are clearly to police a moral hazard problem”. It is true that the ECB, the European Commission and the IMF overdid the austerity but it doesn’t mean that Sergio’s opponents’ claims are accurate.

… But more disturbing still is the notion that with a common currency the ‘balance or payments problem’ is eliminated and therefore that individual countries are relieved of the need to pay for their imports with exports.

Quite the reverse: the existence or a common currency makes a country more directly dependent on its ability to sell exports and import substitutes than it was before, particularly as it will then possess no means whereby it can (in the broadest sense) protect itself against failure.

– Wynne Godley, Commonsense Route To A Common Europe, inThe Observer, 6 January 1991.

Greece had large negative current account balance of payments and Germany had the opposite over the lifetime of the Euro.

Yet, there are some economists who argue that the Euro Area crisis is not a balance of payment crisis. Of course there are other aspects to the crisis as well but this in my view is the main issue. There was a debate between Sergio Cesaratto and Marc Lavoie on this. Now there is a new paper in the most recent issue of ROKE (Review of Keynesian Economics) by Eladio Febrero, Jorge Uxó and Fernando Bermejo which discusses this. The Wayback Machine/Internet Archive link is here if you are reading it after the journal puts the paywall again.

The authors seem to be against Sergio Cesaratto view. Since I agree with Cesaratto, I thought I should comment on it.

The fundamental problem of the Euro Area is that it doesn’t have a central government. If there had been a central government like the US federal government, with large fiscal powers, the Euro Area crisis would have been far less deeper. This is because weaker regions would have been recipients of “fiscal transfers”, i.e., receive more government expenditure than what they send in taxes.

Fiscal transfers can be seen transactions in the balance of payments of Euro Area countries if the EA had a central government. The way to do balance of payments for monetary and political unions is explained in the IMF Balance of Payments and International Investment Position manual. Take a country like Greece. The Euro Area government would be considered external to Greece. Same for other countries. But for the Euro Area as a whole, the central government would be considered inside the Euro Area.

So government expenditure would appear in Greek exports in the goods and services account and transfers in the secondary income account. Taxes would appear only in the latter.

So there is an improvement in the current account balance of payments for regions compared to the case when there is no central government. Current account balances accumulate to the net international investment of the whole country. A country which has persistent imbalances would have negative net international investment position, i.e., indebtedness to other countries.

So fiscal transfers keep all this in check by improving the current account balance. So if the Euro Area had a central government, debts of a country like Greece would be in check.

By joining the half-baked half-way house, Greece got an overvalued exchange rate and easier access for other Euro Area countries into its markets and its external imbalances worsened in its lifetime inside the monetary union.

Nations with high current account deficits will also have higher public debt than otherwise and would need international investors to buy the debt which residents won’t. Normally the price would adjust to bring international investors but as we have seen, sometimes there is no price and a fall in bond prices might lead to expectations of further fall leading external investors to dump the bonds instead of finding them attractive.

The trouble with Febrero et al. is that they seem to think that the European central bank can purchase all government debt of nation. Certainly, the European Central Bank (ECB) has stepped in at various times to ease the pressure on government bond markets. But the trouble with this is that there are under some conditions such as assuming it can impose tight fiscal policy on the governments it is helping.

If the Euro Area treaty is modified to allow countries to have independent fiscal policies, then for stability, the ECB has to buy bonds without limits and can keep accumulating. It is a political mess. A country like Germany could argue that it is writing an open cheque to Greece.

A political union wouldn’t have such problems. National level governments such as the Greek government would have fiscal rules on them, and hopefully not the supranational government. This is like the United States where state governments have rules on their budgets.

In contrast, if the ECB guarantees Greece’s debt, it has to impose some rules and since Greece is not recipient of any equalisation payments—the fiscal transfers—its performance is still dependent on its competitiveness. This is because competitiveness would affect the Greece government’s fiscal balance and hence put a deflationary pressure on Greece’s fiscal stance.

On the other hand, a Euro Area with a central government would imply Greece is recipient of substantial equalisation payments and its competitiveness isn’t so binding.

An argument of the economists arguing that the European monetary system has this thing called TARGET2 and that the intra-Eurosystem balances (i.e., automatic credits offered by one national central bank to another) can rise without limit is used in this paper. This is highly misleading. It is true but one should look at the changes in debits and credits elsewhere. Suppose a country like Greece sees a large private financial outflow. While T2 can absorb a lot of this—much more than anyone imagined—in the late stages, Greece banks become heavily indebted to their national central bank, The Bank of Greece. When they run out of collateral, the rules under ELA, Emergency Liquidity Assistance, is triggered. So TARGET2 or more accurately the Eurosystem cannot absorb everything.

In summary, the Euro Area cannot do without a central government in the long run. Anyone who thinks that the ECB or the Eurosystem can buy whatever residual debt private investors doesn’t understand that in such a system, Euro Area governments are given an open cheque.

The difference between not having a central government and a central government is that in the former, there is no equivalent income flow as in the latter. The Eurosystem purchases would affect the financial account of balance of payments, not the current account.

One of the noticeable assertions of the paper is:

With T2, there is just one currency. This means that if foreign exchange markets did not exist, there could not be a BoP crisis, so that the cause of the crisis should be found elsewhere.

The trouble with this is that it sees it only as a currency crisis. But the fact is that countries whose external position were weak were the ones running into trouble in the Euro Area. Had current account deficits not blown up, countries would have had better fiscal balance since the current account balance and the budget balance are related by an identity and even behaviourally as can be seen in stock-flow consistent models. In crisis times, foreign investors are more likely to shift their funds in their home countries. With better balance of payments, public debt would be held more internally and there would have been less pressure on government bonds.

There are comments in the paper about too much credit etc. This is true, but then the Euro Area crisis would have looked more like the economic and financial crisis affected the United States.

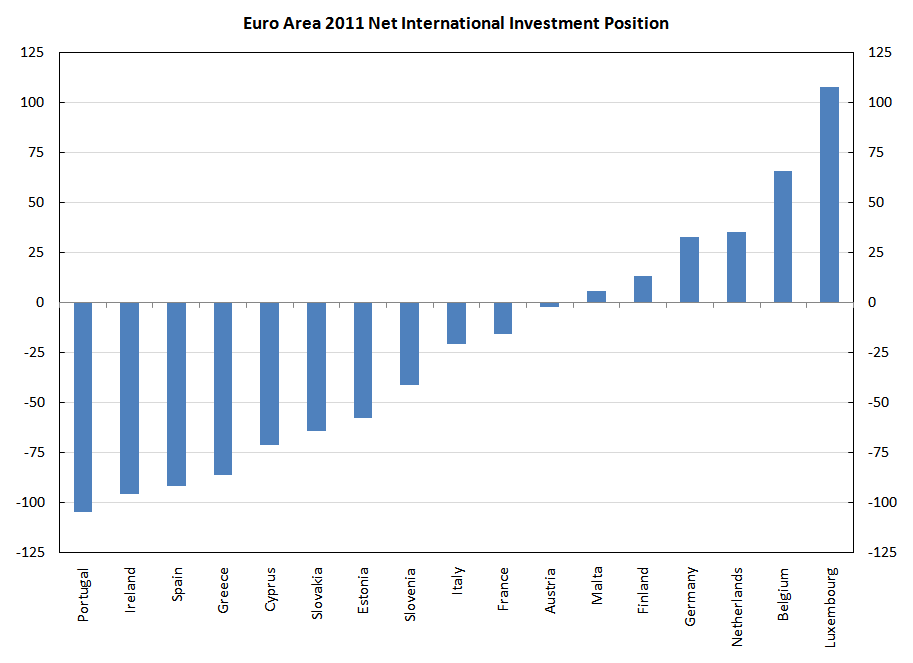

Here’s the the NIIP of Euro Area countries in 2011.

Doesn’t this explain why Germany was in a better position than Greece when the crisis started heating up? Or that Netherlands was in a better position than Portugal?

This mini-post is more intended for my own reference, so that I remember this and don’t forget.

After all these years, Mario Draghi has finally said it. After repeatedly insisting Euro Area governments do “structural reforms”, Draghi has conceded that Germany should do a fiscal expansion.

Draghi: Counties that have fiscal space should use it. Germany has fiscal space

Post-Keynesians have always maintained that “surplus” countries put a burden on “deficit” countries. Since Germany has a high positive current account balance, and sells its product abroad, it isn’t unfair to ask its government to expand domestic demand via fiscal policy and reduce imbalances.

In a recent article for VOX, Paul De Grauwe and Yuemei Ji write about potential fiscal effects of a possible asset purchase program by the Eurosystem (European Central Bank and the National Central Banks in the Euro Area). In that the authors take an extreme stand suggesting that a default by a Euro Area government on bonds held by the Eurosystem doesn’t even matter.

JKH has written a fantastic critique of the VOX article by De Grauwe and Ji.

JKH says:

De Grauwe goes on to say that because bonds held by the ECB –defaulted or otherwise – are “eliminated” on consolidation, it doesn’t matter what they were valued at on the ECB balance sheet in the first place. They may as well have been valued at zero – because they have effectively been eliminated and replaced by ECB liabilities (assumed by implication to be permanently interest free).

…

Thus, the balance sheet implication of De Grauwe’s treatment is that some portion of future currency issued by the ECB will be “backed” on its own balance sheet by an asset of zero value – the defaulted Italian bond. The problem is that this currency would have been issued in any event according to the demand that will arise naturally from the growth of the European economy over time (notwithstanding current depressed conditions). And so ECB seigniorage will have been reduced from what it would have been had it included the effect of good interest on Italian bonds. That reduction in seigniorage due to default is a real fiscal cost, because it reduces the profit remittance of the ECB from what it would have been in the non-default counterfactual. And the fact that the reduced seigniorage gets distributed to the residual capital holders means that there has been a fiscal transfer to the defaulting sovereign from the remaining capital holders. So De Grauwe is simply wrong on this point.

Another way to look at it is by looking at the international investment position. A default by a nonresident on a claim on held by residents is a reduction in the net international investment position and a reduction in the wealth of the geographic region. (The wealth of a nation is the sum of the value of its non-financial assets plus the net international investment position). International investment position matters as a sounder position implies that there is higher potential to raise output.

De Grauwe has another article for The Economist from today. He writes:

Since Milton Friedman we have all become monetarists. In order to raise inflation it will be necessary to increase the growth rate of the money stock. This requires that the ECB increase the money base. And to achieve the latter there is only one practical instrument, ie, an open-market purchase of government bonds. There is no other way to raise inflation than through an increase in the money base and a bond-buying programme is the time-tested way to achieve this.

It is sad that Monetarism is still alive today, despite being repeatedly been shown to be incorrect. But more importantly for the current discussion about risks, De Grauwe repeats his stand again and states it more explicitly:

This confusion between accounting losses and real losses is unfortunate. It has led to long hesitation to act. It also leads to bad ideas and wrong proposals.

So losses do not even matter!

The problem with a Eurosystem asset purchase program of Euro Area government bonds is that it achieves little. It is not a coordinated Euro Area wide fiscal expansion which is badly needed. The ECB already has the OMT program which has helped government bond yields from rising and leading to a crisis, so a QE will hardly achieve much except having an impact on prices of financial market securities. QE just diverts attention from important challenges for a unified Europe. Challenges such as how to move toward the formation of a central government.

Recently Mario Draghi, the European Central Bank President, has been going around telling everyone that “fiscal consolidation” is the absolutely essential to resolve the Euro Area crisis, given some positive developments. Although, this view of his is known and this has had a big influence on policy, he has become more and more vocal about it in recent weeks. He has also signalled a “positive contagion” – a phrase he seems to have coined.

Here is Mario Draghi talking at the recent annual conference at Davos to John Lipsky. (Link no longer works)

If Draghi is to be believed, “fiscal consolidation” is an absolute necessity for the Euro Area to come out of the crisis.

In a recent press conference from January 10, Draghi said the same:

Question: Could Outright Monetary Transactions (OMTs) lose their magical effect in the markets if no country asks for them?

Second question: Jean-Claude Juncker has said that too much fiscal consolidation could have a negative effect on countries like Spain, because unemployment is so high. What can you say about that?

Draghi: On your first question, you do not have to ask me, ask the markets.

On the second, many comments of this type have been made about several countries in the euro area. My answer to this is that so much progress has already been made, accompanied by so many enormous sacrifices. So reverting to a situation which has been found to be untenable would not be right. We should not forget that this fiscal consolidation is unavoidable, and we certainly are aware that it has short-term contractionary effects. But now that so much has been done I do not think it is right to go back.

[emphasis: mine]

Back in July 2012, when Spanish government bond prices were plunging, Mario Draghi came up with a plan to save the Euro Area by first announcing on July 26 in a conference in London that “Within our mandate, the ECB is ready to do whatever it takes to preserve the euro,” and after a pause, “And believe me, it will be enough.”. In the monetary policy meeting on September 6, he outlined a plan by the Eurosystem to buy government bonds without any ex-ante quantitative limits, provided the nations asking this facility agree to terms and conditions – mainly on fiscal policy.

This was greeted with great optimism and the “state of confidence” of the financial markets greatly improved in the next few months. Mario Draghi eventually became the FT Person Of The Year. The fact that nations have a backstop meant that the financial sector has been more willing to finance the governments and the nations actually haven’t felt the need to use the facility so far.

At the time, there was an urgent need to do something and the European Central Bank responded positively to prevent a financial and economic collapse.

While the condition that governments asking for the ECB’s help have to meet is unavoidable for any such plan, Mario Draghi seriously misunderstands the nature of the problem. While it is true that there needs to be structural reforms so that struggling Euro Area countries become more competitive relative to their partners and aim to improve their exports to reduce imbalances within the Euro Area, a Euro-Area wide fiscal contraction will fail to achieve this in any sustainable way. Structural reforms aka wage cuts, will further deflate demand in those nations as Michal Kalecki taught us.

Take Spain for example. Its current account is coming back to balance but this has been the result of a huge deflation of domestic demand and no wonder its unemployment rate hit 26% recently. Statements such as “fiscal consolidation is unavoidable” put all the burden on weaker nations. The Euro Area actually needs a fiscal expansion in creditor nations and although a relatively tighter fiscal policy in the debtor nations compared to creditor nations, an expansion compared to the present state nonetheless. In the long term it needs to form a political union – not like the ones floated by European leaders.

The weaknesses of the Euro Area going forward has been highlighted by Charles Goodhart in a recent appearance in the Economic and Financial affairs session of the UK Parliament. Here is the link to the video.

Also, in December 2012, Draghi and the EU leaders presented a planTowards A Genuine Economic And Monetary Union. Again this approach has the same errors as the plans floating around since decades and debunked by Nicholas Kaldor in 1971 in one of the most prescient articles ever written. See this post Nicholas Kaldor On European Political Union. The European leaders are seriously mistaken to think of any of their plans as “genuine”.

Somehow, the Monetarist counterrevolution of the 1970s seems to have forever distorted the vision of economists and economic advisers to politicians even if they do not think they are Monetarists.

As leaked earlier by Bloomberg, Mario Draghi in a press conference today, presented his big plan to save the world.

This will involve OMTs (Outright Monetary Transactions) – in which a Euro Area nation central government requesting aid from the EFSF/ESM will also be provided help by the ECB. Under this plan, when a nation’s government asks for financial aid (and a big if), the ECB/Eurosystem may buy government bonds in the open markets to bring the yields down.

The Eurosystem will buy bonds with maturities between one and three years and will accept credit risk on these bonds and will not ask for a seniority status in case of default. Of course, this will come with strict conditions – the government asking for aid would need to commit to a tighter fiscal policy and promise supply side reforms. There will be no upper limit to the amount of bonds purchased by the Eurosystem.

During the press conference (actually a bit before as well – after Bloomberg leaked a part of the plan), government bond yields had huge moves (e.g, Spanish ten year yields decreased 39bp). Now, if the yields do not reverse and deteriorate again soon, governments requiring help may just delay asking for aid. However, sooner or later bond yields may rise again – especially if foreigners holding the bonds start to get nervous.

My own view is that this plan significantly reduces the risk of an exit by a Euro Area member. Unlike previous plans (SMP, EFSF, ESM) this has no limit on the amount of funds needed. There is no need to wait for parliaments and courts to approve any transaction or aid.

Of course this is not a happy set of affairs. Forcing governments into retrenchment will lead to economic conditions deteriorating further. One however needs to realize that an independent fiscal policy for the troubled nations – while it (an expansion) increases national income and output – will have the adverse effect of deteriorating the balance of payments – resulting in the public debt and the nation’s net indebtedness to foreigners (and the latter is already high for troubled nations) rising without limit relative to output. The plan will look good in retrospect if it is supposed to be a bridge toward a political union with a central government.

Some bonds of the Greek government mature on March 20. The total principal amount is €14.5bn.

The focus in the financial markets is what will happen to these securities and everyday we read about negotiations with the creditors on “private sector involvement (PSI)”. For the latest see this WSJ article Greece Private-Sector Creditors Meet in Paris.

Brokers estimate that of the 14.5 billion euros of these bonds outstanding, the largest holder is the European Central Bank, which bought these securities in 2010 at a price of around 70 cents in an early, ultimately futile attempt to boost Greece’s failing bond market. The brokers say that 4 billion to 5 billion euros of bonds are owned by hedge funds at an average cost of around 40 cents to 45 cents, with some of the larger positions being held by funds based in the United States that have large London offices.

Let us look at what may happen as far as the Eurosystem is concerned on March 20. Let’s assume that the Eurosystem holds €10bn of the maturing issue – €3bn each by De Nederlandsche Bank and the Bank of Greece and €4bn by the European Central Bank. And that the remaining €4.5bn are held by hedge funds.

Let’s assume that the hedge funds will be paid 15 cents for every € of bond held and are issued new restructured debt securities – i.e., €675m (Plus what about the final coupon payment?)

Question: Where does Greece get the €10.675bn from?

The ECB is opposed to losses on the Eurosystem’s holdings as per this Bloomberg report from today so it may get a preferred creditor status.

The Eurosystem and the Greek government cannot roll the debt as it will violate the Treaty. So some official creditor or a group of creditors (EFSF?) will have to purchase €10bn+ of bonds from the Greek government before March 20 who will then pay €3bn each to the De Nederlandsche Bank and the Bank of Greece and €4bn the European Central Bank (plus coupons) on March 20 who will then later purchase the bonds from the group of official creditors!

The same holds even if the Eurosystem takes some loss.

This is the fifth part of the series of posts on the description of the Eurosystem. In this post, I will discuss whatever I had kept postponing in previous posts – except central bank swaps, which I will postpone to Part 6.

The Euro Area is comprised of 17 nations using the Euro as the legal tender and this is referred to as EA17. In addition, 10 more nations potentially can join the Euro, so they refer to “EU27”. In the recent “summit to end all summits”, European leaders believed in Merkels and worked toward changing the Treaty. UK’s Prime Minister David Cameron refused to sign the new European accord – a wonderful thing to do.

[The UK always had an opt-out option and this move effectively divorces the UK from EU. The other nation with an opt-out is Denmark. The remaining 8 are: Bulgaria, Czech Republic, Hungary, Latvia, Lithuania, Poland, Romania and Sweden. The Wikipedia entry Enlargement of the Euro Zone has good details.]

Before the summit of political leaders, the ECB, in its monthly monetary policy meeting, decided to take steps to improve banks’ conditions: It will now conduct two LTROs with a maturity of 36 months and reduced reserve requirements from 2% to 1%. Other than that, it allowed NCBs to accept bank loans satisfying certain criteria as collateral and reduced the ratings threshold on Asset-Backed Securities. Before this, the maximum maturity of LTRO till date was 1 year.

In the press conference that followed, Mario Draghi, the President of the ECB, dashed market hopes of a more aggressive intervention of the ECB in the markets. The press conference transcript is here. However, analysts saw this as a signal from the ECB to force Euro Area governments into agreeing into fiscal contraction ahead of the summit and still expect the ECB to intervene.

Securities Markets Programme

Back in May 2010, the ECB observed that yields of a few “peripheral” government bonds were rising and it looked as if it could become a “self-fulfilling prophecy” and decided to intervene in the markets. In the ECB’s words, the Governing Council decided to:

To conduct interventions in the euro area public and private debt securities markets (Securities Markets Programme) to ensure depth and liquidity in those market segments which are dysfunctional. The objective of this programme is to address the malfunctioning of securities markets and restore an appropriate monetary policy transmission mechanism. The scope of the interventions will be determined by the Governing Council. In making this decision we have taken note of the statement of the euro area governments that they “will take all measures needed to meet [their] fiscal targets this year and the years ahead in line with excessive deficit procedures” and of the precise additional commitments taken by some euro area governments to accelerate fiscal consolidation and ensure the sustainability of their public finances.

In order to sterilise the impact of the above interventions, specific operations will be conducted to re-absorb the liquidity injected through the Securities Markets Programme. This will ensure that the monetary policy stance will not be affected.

The outstanding amount held (settled, to be precise) by the Eurosystem as on Dec 2 was about €207bn, as per this link.

This has continued to rise in recent months because of rising yields of government bonds with markets suspecting that the public debts of Spain and Italy are on unsustainable territory. So the Eurosystem intervenes frequently and the market participants quickly figure this out.

Who Buys – NCBs or ECB?

Some people have asked me – who buys the bonds: NCBs or the ECB? The answer – I believe – is both. Someone asked me if there are traders in the ECB building at Frankfurt. I do not know – perhaps a few. Someone pointed out that the ECB may be buying using the NCB as its agent. Possible. There’s another question, which nobody has asked me – does an NCB of country A buy government bonds of country B? I think so. Who decides all this is not an easy question!

For example, according to the Banque de France Annual Report 2010, (page 118 of publication, 108 of pdf)

The total amount of securities held by NCBs of the Eurosystem under the SMP increased to EUR 60,873 million, of which EUR 9,353 million are held by the Banque de France and are shown under asset item A7.1 in its balance sheet. Pursuant to Article 32.4 of the ESCB statute, any risks from the holding of securities under the Securities Markets Programme, if they were to materialise, should eventually be shared in full by the NCBs of the Eurosystem in proportion to the prevailing ECB capital key shares.

Assuming, the Eurosystem didn’t need to buy French government bonds till now, (at least till 2010 end), it seems it has purchased government bonds of other EA17 nations.

What about the ECB? Yes. According to the ECB Annual Report 2010, page 223 (page 224 of pdf):

Compare that to the Eurosystem’s consolidated balance sheet item (7.1 below) which was large compared to €17.9bn above at the end of 2010:

Also, according to Banca d’Italia’s Annual Report 2010 (page 224 of publication, 231 of pdf):

“Securities held for monetary policy purposes” was about €18bn at the end of 2010, of which about €8bn was in government bonds under SMP and the remaining covered bonds.

So to summarize, government debt is purchased by all NCBs and the ECB and the NCB purchase is not restricted to purchasing government bonds of the same nation the NCBs are located.

The same is true with the Covered Bonds Purchase Programme. The latter is somewhat equivalent to the Federal Reserve’s purchase of Agency Mortgage-Backed Securities in the United States. Covered Bonds are somewhat similar to Asset-Backed Securities such as MBS; the former are on balance sheet of the issuing bank, unlike the latter which are moved into Special Purpose Entities. The assets backing covered bonds are clearly identified in a “cover pool” and are “ring-fenced” which means that if the issuing bank closes down due to insolvency, the assets in the covered pool will be used to pay the covered bond holders, before they are available to unsecured creditors including depositors. The reason the ECB has chosen covered bonds instead of ABS is because of the strength of the covered bond lobby in Europe.

Emergency Loan Assistance

Imagine the following. A Euro Area country X’s government bond yields are at rising and the bond markets are highly suspicious of the government’s solvency. Banks are also in a bad situation and funds have made frequent flights out of the country. The banks have provided all collateral they had to their home NCB. (To be technically correct, foreign assets are pledged to the respective foreign NCB who acts as a custodian for the home NCB). The government has €8bn of payments to bond holders this week. The government has enough funds deposited at a local bank, so it can meet its obligations. However, most bond holders are foreigners. When the government pays the bond holders, the payment will go through via TARGET2 and commercial banks will run out of collateral to provide to their home NCB.

The above is one way in which banks can run out of collateral and there are other ways in which the government is not the direct reason for the outflow of funds, such as a simple capital flight. For this reason, some NCBs invented a programme called “Emergency Loan Assistance” which may not have been a terminology used in the Treaty. The relevant article which may provide an NCB with this power is the Article 14.4 of the Statute of the ESCB and of the ECB

14.4. National central banks may perform functions other than those specified in this Statute unless the Governing Council finds, by a majority of two thirds of the votes cast, that these interfere with the objectives and tasks of the ESCB. Such functions shall be performed on the responsibility and liability of national central banks and shall not be regarded as being part of the functions of the ESCB.

The situation highlighted above happened frequently with Greece during the past few months. The ELA, however was first used by Ireland in 2010. From the Central Bank of Ireland Annual Report 2010

(click to expand)

The item highlighted “Other Assets” contains the balance sheet item for Emergency Loan Assistance. More below, but before this, it is instructive to look at Liabilities:

(click to enlarge)

So, the Central Bank of Ireland’s Liabilities to the rest of the Eurosystem was around €145bn! – which is indicative of how much funds flew out of Ireland and the amount of stress the nation went through. (Ireland’s 2010 GDP was €154bn, btw). I described how funds flow within the Euro Area in Part 2 of this series.

Back to ELA. Page 104 of the publication (106 of the pdf) describes Other in Other Assets as:

This includes an amount of €49.5 billion (2009: €11.5 billion) in relation to ELA advanced outside of the Eurosystem’s monetary policy operations to domestic credit institutions covered by guarantee (Note 1(v)). These facilities are carried on the Balance Sheet at amortised cost using the effective interest rate method. All facilities are fully collateralised and include sovereign collateral as well as a broad range of security pledged by the counterparties involved.

The Bank has in place specific legal instruments in respect of each type of collateral accepted. These comprise: (i) Promissory Notes issued by the Minister for Finance to specific credit institutions and transferrable by deed, (ii) Master Loan Repurchase Deeds covering investment/development loans, (iii) Framework Agreements in respect of Mortgage-Backed Promissory Notes covering non-securitised pools of residential mortgages, (iv) Special Master Repurchase Agreements covering collateral no longer eligible for ECB-related operations and (v) Facility Deeds providing a Government Guarantee. In addition, the Bank received formal comfort from the Minister for Finance such that any shortfall on the liquidation of collateral is made good. Where appropriate, haircuts (ranging from 5.5 per cent to 80 per cent) have been applied to the collateral. Credit risk is mitigated by the level of the haircuts and the Government Guarantee. At the Balance Sheet date no provision for impairment was recognised.

You can find details of these in this blog post Irish Central Bank Comfort at the blog called Corner Turned, which is now inactive.

Oh yeah … How does the Irish NCB provide the loans? Hint: Loans make deposits.

FT Alphaville has two nice posts (among others) on ELA in Greece: Sundry secret Greek liquidity [updated], Hooray for, erm, Greek ELA?. The first one pokes on how the Bank of Greece – Greece’s NCB – hides the item under “Sundry” and the second one one how Greek banks’ net interest income were higher than expected – the reason being that expensive deposits were replaced by cheaper NCB funding!

This concludes this post. In Part 6 – the final one – I will discuss central bank liquidity swap lines with the Federal Reserve.

Mario Draghi is talking to press reporters now, as I write.

The ECB reduced reserve requirements to 1% from 2% and plans to do Long-term Refinancing Operations with maturity up to 3 years (i.e., it will lend banks for a term of three years). It also relaxed collateral standards.

The markets are in absolute roller coaster. Mario said that IMF borrowing from the Eurosystem and lending the governments is a violation of the spirit of the Treaty and repeatedly said monetary financing of governments is not allowed because the Treaty embodies the best tradition of Bundesbank and that fiscal retrenchment will enhance confidence of the markets! Central bankers can’t give up their dogmas, can they?

And to make his point clear, he again repeatedly said “no financing of governments” and while reporters tried no end to get something from him, he said “I wish all our leaders the best, and the ECB is here — which does not mean the ECB will respond” !

Here is FTSE MIB (FTSE’s Index for Italian Stocks)

(Source: Google Finance)

Here’s a chart of EURUSD from my iPhone CitiFX app

{kind=link}

{kind=link}