FT has published a letter to the editor from some post-Keynesian economists arguing for regulating imbalances in the current account balance of payments, and that such imbalances make wars more likely.

One of the signatory of the letter is Dimitri Papadimitriou, who along with Wynne Godley had been warning about imbalances since the turn of the millennium.

From the letter:

…

A new international economic policy initiative is therefore required to head off the threat of further wars.

A plan is needed to regulate current account imbalances, which draws on John Maynard Keynes’s project for an international clearing union.

…

The current system of free trade has created a deflationary bias in the world economy. A further bias is introduced because the United States is now a large debtor of the world and till the crisis which started in 2007 it was acting as the driver of the world, a role which it still plays but is not as big as before. With such a deflationary bias, countries try to use beggar-thy-neighbour policies, as world output is limited. That creates tensions between countries and the desperation to raise output exacerbates the tensions. So a new international order: a system of regulated/planned trade.

Dimitri B. Papadimitriou, Michalis Nikiforos and Gennaro Zezza have a new report on prospects for the US economy.

They argue that while the US economy would enjoy a boom in the near term because of the large fiscal stimulus, the danger is that because of the large trade imbalance because of the different growth rates of the US and its trading partners implies that the continuation would require a large fiscal deficit or the private sector becoming a net borrower.

In my opinion, soon enough when the US economy starts approaching full employment, there will be shouts to cut the fiscal stance because as Michal Kalecki argued captains of industry don’t like full employment. And/or: continuous growth would require high fiscal deficits but as the public debt will continue to rise relative to gdp, politicians will get nervous.

The US government could try to improve net exports by increasing competitiveness of US firms but such things take time. A combination of trying to improve net exports by industrial policy, tariffs and eventually removing the system of free trade is the way forward. It won’t be easy as economists are attached to dogmas.

There was a conference on the 10th death anniversary of Wynne Godley last year. If you haven’t seen it, the video recordings/presentation/remarks are in that link.

Now, there’s a special issue by the JPKE about the conference with papers as in the cover:

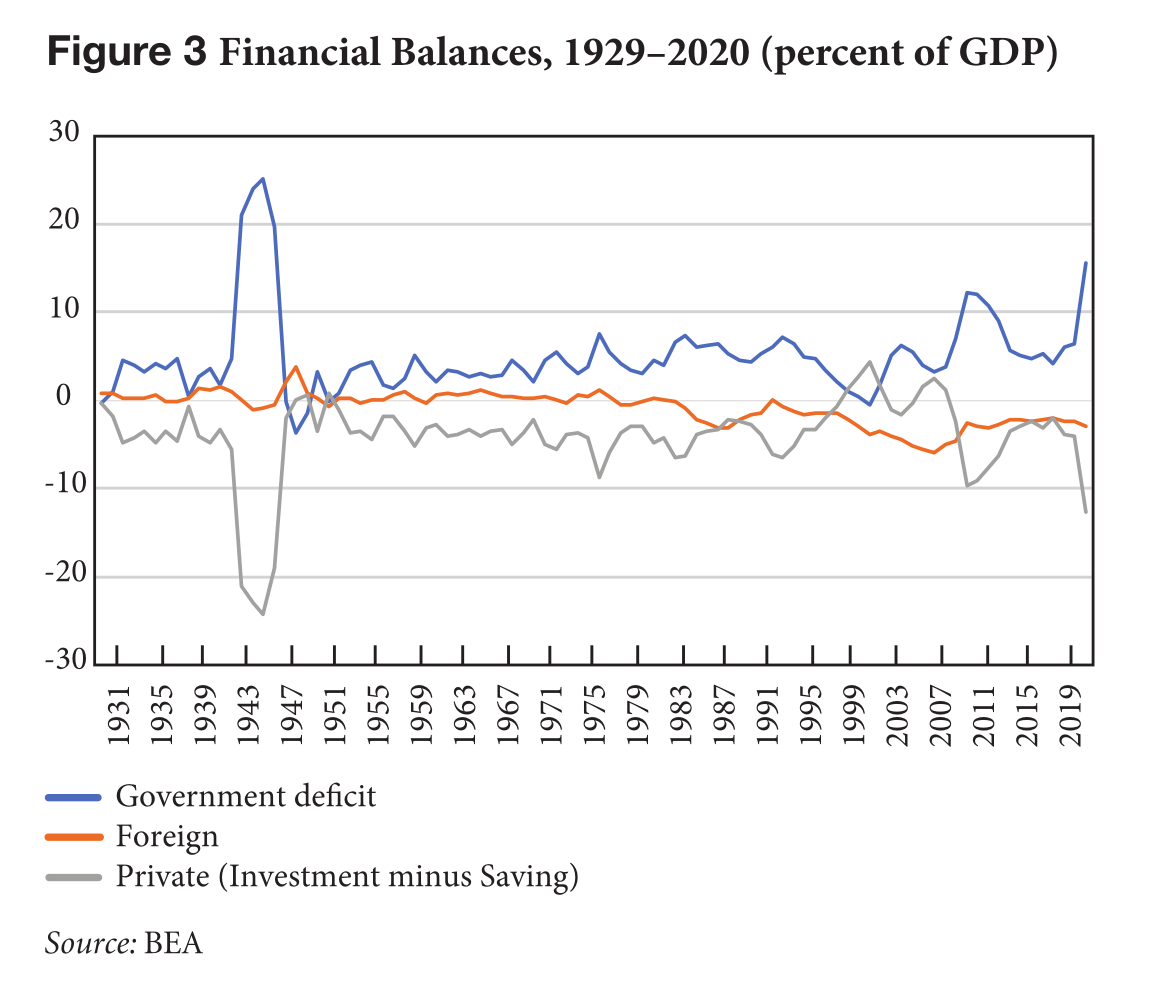

The latest Strategic Analysis report from Levy Institute.

Interesting chart and explanation:

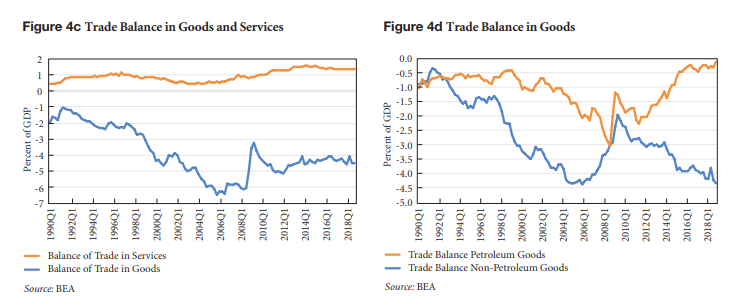

The main reason for the relative stability of the trade and current account balances is presented in Figure 4d. Since the beginning of the recovery, the trade deficit in goods except for petroleum products has been following its precrisis trend.3 At the end of 2018 it reached its precrisis peak—and for that matter its historical peak—of around 4.4 percent. However, at the same time this increase has been counteracted by the improvement in the trade balance of petroleum goods, related to shale gas extraction. The trade deficit of petroleum goods is now close to zero, compared to 2.2 percent of GDP when shale gas extraction started in 2011 and 3 percent before the crisis. It is not then hard to calculate that, had it not been for this improvement in the petroleum products trade balance, the overall trade deficit of the US economy would be close to 7 percent, or more.

…

Notes

…

To be more precise, the trade balance of non-petroleum goods started slowly improving in 2006, more than a year before the economy officially entered the recession. This improvement had to do with two main factors: (1) the slowdown of the US economy that had started already in 2006, and (2) the significant depreciation of the dollar that started in 2002 and continued up until 2008.

The US economy is only 8.8 percent above the pre-crisis peak.

The Levy Institute has a new Strategic Analysis publication titled Fiscal Austerity, Dollar Appreciation, And Maldistribution Will Derail The US Economy in which they identity three main structural characteristics of the economy of the United States that stand in the way of the recovery:

(1) the weak performance of net exports, (2) pervasive fiscal conservatism, and (3) high income inequality

They show that in their baseline scenario, if the projections of the Congressional Budget Office’s outlook hold, their model simulations imply that the private sector’s net lending would turn negative by the end of 2017 and hence the private sector would be in a financial deficit, which is not sustainable.

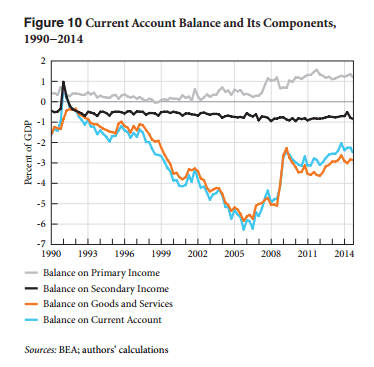

The publication has some nice charts about the US balance of payments. One is the components of the current account of balance of payments with attention on the primary income balance:

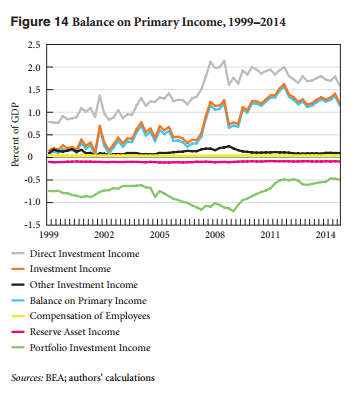

Note how the balance on primary income has grown during the recent crisis. Another chart gives a further breakdown:

So direct investment income is the main component.

I like the way the authors explain this: it is a symptom of the crisis. From the article:

An interesting question is whether this improvement in net primary income receipts is sustainable or just symptomatic of the crisis. In our view, it is most likely the latter.

According to the authors Dimitri Papadimitriou, Gennaro Zezza and Greg Hannsgen,

The results of our simulation are reported in Figure 4. The government deficit falls rapidly, but if we want to achieve the CBO’s projected growth path, the private sector has to start borrowing again, switching to a deficit position. Under this scenario, we would return to a situation not so different from the one we had before the 2007–09 recession.

In Figure 5 we report the path of household and non-financial business debt, relative to GDP. Both of these sectors must become more indebted, given our scenario 1 assumptions. If this is the path the US economy takes, it will not be long before another crisis hits, if only because of heavy private sector indebtedness.

Here’s private indebtedness in the assumed CBO scenario of growth and lower budget deficits.

So this implies that the United States still has cracks in the foundations of growth (as per a title of the Institute’s Strategic Analysis piece before the crisis) and policy needs to change.

The Institute’s Strategic Analysis articles have always pointed out logical inconsistencies in the CBO’s projections (from mid 1995 onward) and presented more realistic scenarios on growth with solid suggestions on how to run the economy. Here’s from April 2007 in a report titled The U.S. Economy – What’s Next:

The authors said:

In Figure 3, we translate the debt-to-GDP ratios in Figure 2 into flows of lending relative to GDP simply by subtracting from each quarter’s debt the previous quarter’s debt. One striking feature of Figure 3, not at all obvious from inspection of Figure 2, is that net lending was already falling rapidly from the beginning of 2006. The lower line for the post-2006 period shows what would happen to the net lending flow if the debt-to-income ratio were to level off: net lending would continue to fall rapidly, though not so far or fast as happened in 1980. The projections in the figure also show the enormous gap between the leveling-off scenario, in which we are inclined to believe, and the (implied) CBO scenario, in which we don’t believe at all.

In reaching provisional conclusions about the future growth rate of output and the future configuration of the three financial balances, we have used revised assumptions about output in the rest of the world because of lower U.S. growth than in the CBO scenario (based on the solution of a world model) and the performance of the stock market. The major conclusion is that output growth slows down almost to zero sometime between now and 2008 and then recovers toward 3 percent or thereabouts in 2009–10. However, by the end of the period, the level of output is still far (about 3 percent) below that in the CBO’s projection, which implies that unemployment starts to rise significantly and does not come down again.

Of all the economists, Wynne Godley had the rarest of rare ability to model and imagine the economic dynamics of the whole world. “… a full macroeconomic model in his head, which, by some sort of subconscious process, he computed.” as his obituary from FT said.

In the recent INET conference paper, Dirk Bezemer discusses Wynne Godley’s approach (among others’) and also refers to his paper Seven Unsustainable Processes from 1999.

I obtained this original scanned copy of the paper Seven Unsustainable Processes – Medium Term Policies For The United States And The World by Wynne Godley from 1999 from the Levy Economics Institute and thought that since this version is missing for some reason from the levyinstitute.org website, I’ll post it here (after asking them if I may post).

Click to see the pdf.

Seven Unsustainable Processes from 1999

Here’s the link to the updated version of the paper from the year 2000. The original had a typo. Two columns in Table 1 appeared with incorrect headings (should have been the reverse).

Wynne Godley at the Levy Institute

Godley warns of the private sector indebtedness:

… Moreover, if, per impossibile, the growth in net lending and the growth in money supply growth were to continue for another eight years, the implied indebtedness of the private sector would then be so extremely large that a sensational day of reckoning could then be at hand.

Wynne Godley never liked the chimerical and primitive view of economists where anything and everything is traded in the markets via supply and demand. So,

The difference between the consensus view and that put forward here could not exist without a profound difference in the view of how the economy works. So far as the author can observe, the underlying theoretical perspective of the optimists, whether they realize it or not, sees all agents, including the government, as participants in a gigantic market process in which commodities, labor, and financial assets are supplied and demanded. If this market works properly, prices (e.g., for labor and commodities) get established that clear all markets, including the labor market, so that there can be no long-term unemployment and no depression. The only way in which unemployment can be reduced permanently, according to this view, is by making markets work better, say, by removing “rigidities” or improving flows of information. The government is a market participant like any other, its main distinguishing feature being that it can print money. Because the government cannot alter the market-clearing price of labor, there is no way in which fiscal or monetary policy can change aggregate employment and output, except temporarily (by creating false expectations) and perversely (because any interference will cause inflation).

No parody is intended. No other story would make sense of the assumption now commonly made that the balance between tax receipts and public spending has no permanent effect on the evolution of the aggregate demand. And nothing else would make sense of the debate now in full swing about how to “spend” the federal surplus as though this were a nest egg that can be preserved, spent, or squandered without any need to consider the macroeconomic consequences.

The seven unsustainable processes were:

(1) the fall in private saving into ever deeper negative territory, (2) the rise in the flow of net lending to the private sector, (3) the rise in the growth rate of the real money stock, (4) the rise in asset prices at a rate that far exceeds the growth of profits (or of GDP), (5) the rise in the budget surplus, (6) the rise in the current account deficit, (7) the increase in the United States’s net foreign indebtedness relative to GDP.

As it happened, the United States went into a recession but recovered quickly because of further deregulations and low interest rates which led to more borrowing, and a fiscal stimulus which put a floor on the downfall. However, the private sector went back into deficits and its indebtedness kept rising relative to income. The current balance of payments also went deeply in deficit rising to about 6.43% at the end of 2005 – hemorrhaging the circular flow of national income at a massive scale. See the related post here: The Un-Godley Private Sector Deficit.

Not only did Godley see the crisis coming, he also figured out that the United States will soon run into policy issues and will have less room to come out of a crisis. In this 2005 strategic analysis paper The United States And Her Creditors – Can The Symbiosis Last? he and his collaborators (Dimitri Papadimitriou, Claudio Dos Santos and Gennaro Zezza) pointed out that:

The range of strategic policy options for the United States is beginning to narrow … As the normal equilibrating forces (changes in exchange rates) are being subverted, it is very far from obvious what the United States can do on her own …

The prospects for the U.S. economy have become uniquely dreadful, if not frightening. In this paper we argue, as starkly as we can, that the United States and the rest of the world’s economies will not be able to achieve balanced growth and full employment unless they are able to agree upon and implement an entirely new way of running the global economy.

Stressing the need for concerted action (from which I got the title of my blog!), the authors said:

… Fiscal policy alone cannot, therefore, resolve the current crisis. A large enough stimulus will help counter the drop in private expenditure, reducing unemployment, but it will bring back a large and growing external imbalance, which will keep world growth on an unsustainable path …

… What must come to pass, perhaps obviously, is a worldwide recovery of output, combined with sustainable balances in international trade. Since this series of reports began in 1999, we have emphasized that, in the United States, sustained growth with full employment would eventually require both fiscal expansion and a rapid acceleration in net export demand. Part of the needed fiscal stimulus has already occurred, and much more (it seems) is immediately in prospect. But the U.S. balance of payments languishes, and a substantial and spontaneous recovery is now highly unlikely in view of the developing severe downturn in world trade and output … By our reckoning (which is put forward with great diffidence), if the United States were to attempt to restore full employment by fiscal and monetary means alone, the balance of payments deficit would rise over the next, say, three to four years, to 6 percent of GDP or more—that is, to a level that could not possibly be sustained for a long period, let alone indefinitely …

… It is inconceivable that such a large rebalancing could occur without a drastic change in the institutions responsible for running the world economy—a change that would involve placing far less than total reliance on market forces.

There are two new books in honour of Wynne Godley and they are out now

The first one – edited by Marc Lavoie and Gennaro Zezza – has selected articles and papers by Wynne Godley, and carefully chosen.

It’s available at amazon.co.uk, but not yet on amazon.com

Here’s the book’s website on Palgrave Macmillan. The book also contains the full bibliography of Godley’s papers, books, working papers, memoranda (such as to the UK expenditure committee), magazine/newspaper articles, letters to the editor etc.

Here’s a picture I took of Marc at Levy Institute in May when he was deciding on the cover.

The is second book written in honour of Wynne Godley contains proceeding of the conference held in May at the Levy Institute (the same place the above photograph was taken)

The death of Wynne Godley silences a forceful and very often critical voice in macroeconomics. Wynne’s own strong view, that although his work was representative of the non-mainstream Keynesian approach to economics and especially economic policy was important nevertheless, has been confirmed time and time again as evidenced in the fortunes of the UK, US and Eurozone economies. His writings, reflecting the sharpness of his mind and intellectual integrity, have had a considerable impact on macroeconomics and have aroused the interest of scholars, economic journalists and policymakers in both mainstream and alternative thought. In a review of Wynne’s last book with Marc Lavoie (2007), Lance Taylor had this to say: ‘Wynne’s important contributions are foxy – brilliant innovations… that feed into the architecture of his models’

I also like Wynne’s stand on the current account imbalance of the United States:

Bibow finds that Godley’s diagnosis of the looming economic and financial difficulties ahead of their occurrence was prescient with regard to US domestic developments – a theme that came up in the chapters by Wray and Galbraith. But Bibow takes issue with Wynne’s assessment of the US external balance being unsustainable. He notes that the US investment position and income flows are more or less in balance and he attributes this phenomenon to the safety of the US Treasury securities and the dollar functioning as the reserve currency.

Dimitri then says

Even if this is so, it cannot continue indefinitely, Wynne would have replied.