According to a Wall Street Journal article from yesterday Cyprus Seen Close to a Request for Bailout, Cyprus (2011 GDP: €18bn approximately) is set to become the fourth Euro Area nation to seek a bailout after Greece, Ireland and Portugal. According to the WSJ:

Late last year, the country negotiated a €2.5 billion ($3.1 billion) bilateral loan from Russia. Now, Cyprus is in talks with China for another bilateral loan, of an undisclosed amount, that looks unlikely to materialize in time.

Had to go into trouble considering that economists have been realizing that the Euro Area problems is an internal balance of payments crisis.

The closest proxy for a nation’s net indebtedness is the net international investment position (as opposed to “external debt” which excludes equity held by nonresidents). Here’s the chart as of 2011: the NIIP is at the end of 2011 and the GDP is the gross domestic product for the whole year.

(click to enlarge)

Note: Greece’s NIIP improved in 2011 (from minus 100% of gdp) due to large revaluation losses suffered by foreigners as Greece financial markets fell in 2011.

The financial markets is now nervous about Spain and Slovakia’s next in the line if the graph is to be believed and it’s external position is in dangerous territory also – at minus 64%.

According to Wynne Godley, anything between 20-40% of net foreign indebtedness can be highly dangerous. Of course his models also show that there is nothing intrinsically stopping such imbalances from continuing and can go on as long as foreigners do not mind but something has to give in – such as slower growth to prevent the imbalances from continuing before foreigners start minding or a crash.

At this point, Slovakia doesn’t seem to be in trouble with its generic 10-year government bond yield at 3.645% – with its public debt at 43.3% of gdp at the end of 2011 according to Eurostat. This of course means that the domestic private sector is a net debtor (i.e., its financial assets is lesser than its liabilities). A more detailed analysis is required on how internal imbalances will play out and spill over to the external sector. Here’s from Statistical Appendix of the “Alert Mechanism Report”.

(click to enlarge)

Moving on to something different:

Heteredox Economics In Playboy!

Via Twitter:

click to view the tweet on Twitter

John Cochrane of Chicago calls heteredox economists “kooks” and claims he and his colleagues use rigorous models!

Martin Wolf has just written an article on FT: Why the Bundesbank is wrong questioning the arguments made by Jens Weidmann, president of the Bundesbank. (This speech: Rebalancing Europe).

This chart is interesting:

(click to enlarge)

Wolf says:

Arguably, the crucial step is to agree on the nature of the illness. On this, progress is now being achieved, at least among economists. It is widely accepted that the balance of payments is fundamental to any understanding of the present crisis. Indeed, the balance of payments may matter more in the eurozone than among economies not bound together in a currency union.

I am not sure how widely accepted or understood this is, but it’s exactly right!

(Also never mind the reference to Werner Sinn in the next line in the original article – although Sinn still had a point in spite of his rather painful analysis)

Unable to make a draft at the central bank, governments are left with less means of protecting themselves in case of failures. Hence nations in a currency union are more directly dependent on the external sector.

Then on Weidmann:

Alas, these remarks confuse productivity with competitiveness. Yet these are distinct: the US, for example, is more productive, but less competitive, than China. External competitiveness is relative. Moreover, at the global level, the adjustment must also be shared. Mr Weidmann knows this. As he says, “of course, surplus countries will eventually be affected as deficit countries adjust”. The question is by what mechanism.

[emphasis: mine]

Martin Wolf knows how economies as a whole work roughly and he has been emphasizing that the solution to the world’s problems lie with the creditor nations. Also, in 2004 he said that America is in a comfortable path to ruin!

So here’s an unsuccessful attempt to prove Martin Wolf doesn’t “get it” from Bill Mitchell: So near but so far … from comprehension. This was a critique of an article written by Martin Wolf where he showed that the creditor status of Japan is hugely helpful to its recovery in spite of having a huge public debt . . . Martin Wolf’s right in spite of Mitchell’s assertion that he is wrong 🙂

My last post was on U.S. net income payments from abroad and how it continues to be in the favour of the United States. The late Wynne Godley had been analyzing this since 1994. In an article titled U.S. Trade Deficits: The Recovery’s Dark Side?, written with William Milberg, he had a section called “Foreign indebtedness and the foreign income paradox” where he said:

So far, the practical consequences of the United States having become “the world’s largest debtor” have not been all that significant… But it would be an error to suppose that, because the net return on net assets has been negligible in the recent past, the same thing will be true in the future…

… Why did the net foreign income flow remain positive for so long after 1988? In order to understand this apparent paradox, it is essential to disaggregate stocks of assets and liabilities and their associated flows, and to distinguish (in particular) between financial assets and direct investments… The reason that net foreign income remained positive for so long can now be understood (at least up to a point) by making a comparison of the flows shown in Figure 3 with the stocks shown in Figure 2. The net inflow that arises from direct investment has been roughly equal to the net outflow on financial assets in recent years, even though the stock of financial liabilities has been about five times as large as the market value of net foreign investments. In other words, the rate of return on net direct investments far exceeded the rate on net financial liabilities

Figure 2 referred to is below:

and Figure 3:

which is what I redrew with updated data in my previous post. But as we saw the net income payments from abroad continues to be positive (!!) even till date but the reason is similar. Foreign direct investment in the United States has risen to $2.8T at the end of 2011 as per Federal Reserve’s Z.1 Flow of Funds while U.S direct investment abroad rose to $4.8T – significantly higher (even as a percent of GDP) than in the mid-90s.

The net direct investment has seen huge returns (both via income and holding gains) and so this killing has brought in good fortunes for the United States. Of course with the whole current account of balance of payments in deficit, the external sector bleeds the circular flow of national income in the United States and contributes to weak demand there.

So a current account deficit is bad for the United States but financing this deficit has been easy for the United States given that the US Dollar is the reserve currency of the world. Why do nations require reserve assets? The late Joseph Gold of the IMF gave a nice description in his book Legal and Institutional Aspects of the International Monetary System: Selected Essays:

click to view on Google Books

What makes the US dollar the reserve currency of the world is difficult to argue. However it cannot be taken for granted that the United States may enjoy this exorbitant privilege given that the Sterling was once the darling of the financial markets and central banks.

Their argument is similar – direct investments have made huge returns for the domestic private sector of the United States and gives a good account of the external sector. Here’s a graph of the United States’ net international investment position using data reported by the Federal Reserve’s Z.1 Flow of Funds Accounts as well as the BEA’s International Investment Position:

Why the difference is a topic for another post. I don’t know it yet. Gourinchas and Rey have some answers. The Federal Reserve’s data is till 2011 end and quarterly (and seasonally adjusted) while BEA data is yearly and available till 2010.

So, from the graph above, the United States became a net debtor of the world around 1986. The indebtedness has been rising mainly due to the huge current account deficits the nation manages to run and is partly offset by “holding gains”.

Here’s a graph of the current account deficit plotted with other “financial balances” (since they are related by an identity)

By the way, the U.S. was a creditor of the world when the Bretton Woods system of fixed exchange rates collapsed. Some authors describe this collapse by saying that money has become fiat since 1971 – whatever that means!

Gourinchas and Rey point out – correctly in my opinion:

The previous discussion points to a possible instability, even in an international monetary system that lacks a formal anchor. The relevant reference here is Triffin’s prescient work on the fundamental instability of the Bretton Woods system (see Triffin 1960). Triffin saw that in a world where the fluctuations in gold supply were dictated by the vagaries of discoveries in South Africa or the destabilizing schemes of Soviet Russia, but in any case unable to grow with world demand for liquidity, the demand for the dollar was bound to eventually exceed the gold reserves of the Federal Reserve. This left the door open for a run on the dollar. Interestingly, the current situation can be seen in a similar light: in a world where the United States can supply the international currency at will and invests it in illiquid assets, it still faces a confidence risk. There could be a run on the dollar not because investors would fear an abandonment of the gold parity, as in the 1970s, but because they would fear a plunge in the dollar exchange rate. In other words, Triffin’s analysis does not have to rely on the gold-dollar parity to be relevant. Gold or not, the specter of the Triffin dilemma may still be haunting us!

Gourinchas and Rey’s arguments depend on estimating a tipping point – the point where the net income payments from abroad turn negative. This of course depends on various assumptions but let us look at it.

The gross assets of the United States held abroad and liabilities to foreigners keep changing as the nation is able to increase its liabilities and use it to make direct investments abroad. The reserve currency status has provided the nation with this privilege as central banks around the world are willing to hold dollar-denominated assets. The positive return (as well as revaluation gains from the depreciation of the dollar – when it depreciates) helps reduce the net indebtedness but the current account deficit contributes to increasing it.

The following is the graph of gross assets and liabilities – using the Federal Reserve’s Z.1 Flow of Funds Accounts data and also BEA’s data for the ratio:

So assuming assets held abroad A make a return rA and liabilities L to foreigners lead to payments at an effective interest rate rL income payments from abroad will turn negative whenever

rA · A − rL · L < 0

So A and L are changing due to the current account deficits and revaluation gains on assets and liabilities. Meanwhile, the effective interest rates are themselves changing in time because of various things such as short term interest rates set by the central banks, market conditions, state of the economy etc. Also, if the private sector of the United States makes more direct investments abroad, this will contribute to increase rA (if successful) and the process can go on with net income payments from abroad staying positive for longer. The tipping point is defined by Gourinchas and Rey as the ratio L/A beyond which the the net income payments turn negative. According to their analysis (based purely on historical data), this is 1.30.

If the net income payments from abroad turns negative, international financial markets and central banks may start suspecting the future of the exorbitant privilege according to the authors. Of course, it may be the case that even if it turns negative, the United States’ creditors don’t mind – this has been the case of Australia. The following is from the page 18 of the Australian Bureau of Statistics release Balance of Payments and International Investment Position, Australia, Dec 2011 and in their terminology – which is the same as the IMF’s – it is called “net primary income”)

(Australia’s Q4 2011 GDP was around A$369bn for comparison) and the above graph is quarterly.

So, to conclude the process can continue as long as foreigners do not mind. It shouldn’t be forgotten however that Australian banks had funding issues during the financial crisis and the RBA used its line of credit at the Federal Reserve via fx swaps to prevent a run on Australian banks and it is difficult to design policy without keeping in mind the possibility of walking into uncharted territory.

Once net primary income turns negative, the process can quickly run into unsustainable territory due to the magic of compounding of interest unless the currency depreciates in the favour of the nation helping exports. Else demand has to be curtailed to prevent an explosion but this hurts employment. Other policy options include promotion of exports and asking trading partners to increase domestic demand by fiscal expansion.

The world economy has grown over the last so many years with the United States acting as the importer of the last resort. However, the U.S. current account deficit acts to bleed the circular flow of national income and weakens demand in the States. The nation still grew because of a huge lending boom.

Today, the U.S. Bureau of Economic Analysis came out with the Q4 report on the U.S. International Transactions. According to the release,

The U.S. current-account deficit—the combined balances on trade in goods and services, income, and net unilateral current transfers—increased to $124.1 billion (preliminary) in the fourth quarter of 2011, from $107.6 billion (revised) in the third quarter. Most of the increase in the current account deficit was due to a decrease in the surplus on income and an increase in the deficit on goods and services.

So the current account balance also consists of “income payments from abroad” – a bit of wrong phrasing because all items are income/expenditure flows. The net income payments from abroad continues to surprise analysts because in spite of the net indebtedness position of the United States, this continues to be positive and in recent times has increased! (although it fell the last quarter). Many hold the belief that the United States has lower interest rates and this is the consequence of that. While it is true that interest rates outside the U.S. are in general higher, and there is some truth to the above argument, it gives one the wrong impression that it will always be the case that net income from abroad will always be positive.

The following graph shows that this intuition is misleading. Most of the contribution to the net income is due to direct investments abroad which has made a killing for the private sector and the reverse – direct investment receipts for foreigners has made next to nothing. The remaining – income from financial assets held abroad less interest/dividend paid to foreigners’ holding of U.S. financial assets is already negative!

The red line has reduced in recent times due to lower interest rates in the U.S. presumably. But the more the U.S. continues to run large current account deficits, the deeper the red line will grow – pulling the black line to zero and into the negative territory.

The net income payments from abroad is more a result of the huge killing the U.S. domestic private sector has made abroad than because of lower interest rates. For example, excluding FDI, the data from BEA suggests that the “effective interest rate” on U.S. liabilities was 1.42% in 2010, while that on U.S assets held abroad is 1.65%. This differential will not be sufficient to keep the income payments to foreigners bounded. I used the 2010 data because the International Investment Position is available only till 2010 and the one for end of 2011 will be released only mid-2012.

To understand this, consider the case when the U.S net indebtedness grows to something about 100% of GDP due to the continuous current account deficits – if market forces allow the whole process to go on(!). This is an involved analysis involving some growth assumptions and the fiscal stance in the U.S. and the rest of the world. For example, people frequently forget that a higher growth in the U.S. will also bring in higher current account deficits. But it can easily be shown that the red and the black lines above grow into a negative territory if the United States wants to quickly achieve full employment by fiscal policy alone.

Of course the above graph shows that there is a lot fiscal expansion can achieve in the medium term for the United States.

These numbers look “small” and can lead one into believing that “all is well”. And this is another mistaken view. For example if there is a drastic relaxation of fiscal policy by the U.S. government, the current account deficit will soon hit 6-8% of GDP which may require further relaxation of fiscal expansion to compensate the leakage of demand due to the current account deficit and with income payments turning negative due to higher indebtedness, this will turn into an unsustainable path because the current account deficits and net indebtedness will keep increasing relative to GDP. This will need interest rate hikes to attract foreigners but turns the whole process unsustainable unless one believes in the foreign exchange market doing the trick. Also currently the interest rates are low because the Federal Reserve has kept them artificially low and foreigners do not mind holding U.S. dollar assets at this rate. As William Dudley says interest rates will be raised at some point by the Federal Reserve and this will increase payments to foreigners. See this post William Dudley On U.S. Sectoral Balances

Of course, this is not the only scenario and there’s a lot fiscal policy can achieve in the medium term but it is important to keep in mind that something needs to be done with the external sector to bring the external sector in balance to achieve full employment.

Found this graph at this hilarious blog which quotes Diapason Research. The graph plotted by the researchers uses cumulative current account balances from IMF’s data. I instead directly used the Net International Investment Position at the end of Q3 2011 from Eurostat.

The blue bars plot the net indebtedness of each EA17 nation (with signs reversed) and the red line is cumulative from left to right. It does not sum to zero because the Euro Area as a whole is a net debtor of the rest of the world.

The indebted European nations owe their creditors €2.2tn – which is almost 40% of the gdp of these nations as a whole.

An alternative way to plot the NIIP- in ascending/descending order as a percent of gdp. Readers of the Concerted Action blog will know that I love the NIIP! I just found a nicer way to plot this. The alternative graph is below:

In yesterday’s post Spain’s Sectoral Balances, I briefly discussed the sectoral balances of Spain and its connection with demand, income and output. Here’s the original graph from the Banco de España again with my viewpoints in the previous post.

I learned some GIMP from a friend some time ago and thought I’ll use it for some fun.

I consider two scenarios:

Suppose the Spanish government relaxes its fiscal policy (independent of other Euro Area governments’ policies) or does not tighten it. How do the sectoral balances look? Here’s a likely scenario:

(may not sum to zero because of drawing discrepancies)

The “projection” – not to scale since I had limited availability for space – implies the government deficit keeps rising and this is the result of the rising current account deficit. A higher fiscal stance leads to a slightly higher income and employment but the flip side of this is a rising indebtedness to the rest of the world caused due to the current account deficits. The public sector is incurring almost all the change in net indebtedness – i.e., its contribution to net borrowing from the rest of the world is the highest.

Of course, this process cannot go on forever as a rising indebtedness implies foreigners have to be attracted by hook or crook and interest rate paid on government debt and consequently all private sector debts will also keep rising leading to a deflationary bust at some stage.

Also note, the causality here is a bit opposite of what was described in the previous post! The causalities between the balances of the “three sectors” is complex and not so straightforward. Here a higher fiscal stance leads to a higher income and expenditure and a widening of the current account deficit which in turn widens the budget deficit.

To prevent such possible instabilities – at least their smell of such instabilities – the European leaders have imposed the “fiscal compact” on nations.

What do they aim to achieve? The following “projection” is a possible answer:

The above describes the possible outcome of a tight fiscal stance of the Spanish government. A tight fiscal policy leads to lower income and hence a lower current account deficit – because of lower expenditure on foreign products – but it is achieved via lower output and employment.

The above projections are not based on a specific model for the Spanish economy but some analysis based on familiarity with SFC modelling.

Macroeconomics is not so easy – there are so many constraints – and governments have to strive to achieve the best optimal outcome. “Market forces” do not do that.

The second scenario can also be achieved by a coordinated fiscal expansion by the Euro Area nations. The sectoral balances may behave similar to the second scenario but in the expansionary scenario, output and hence employment is higher. Unfortunately there is no mechanism or institutional means by which fiscal policies are coordinated within the Euro Area (the exception is the recent “fiscal compact” which unfortunately misses the point). Even if there is an agreement on fiscal expansion, there is nothing to make sure that there is a constant management of the whole process – i.e., there are chances of failure.

There are various ideas one sees on proposing a solution to end the Euro crisis but almost none appreciate the real problems. In my opinion, there is no alternative to moving ahead with a European integration and granting more fiscal powers to the European powers – making it a central government – which is involved in fiscal transfers and a mandate to achieve full employment.

The Banco de España released its Quarterly Economic Bulletin today and it had an interesting chart on the sectoral balances of the Spanish economy.

With a net indebtedness of €994.5bn – i.e., close to €1 trillion – as compared to the gross domestic product of €1.06tn (2010 figure) Spain has limited choices. Except via the possibility of expanding by another private sector led credit expansion which is highly unlikely, the Spanish economy faces the prospects of low output and demand. Increasing exports is another option but with all Euro Area nations’ governments being forced by a “fiscal compact” to contract, this is unlikely because of low demand in the rest of Europe.

The chart is really interesting as it illustrates some of the many causalities associated with the financial balances identity

NAFA = PSBR + BP

where NAFA is the Net Accumulation of Financial Assets of the domestic private sector, PSBR is the Public Sector Borrowing Requirement or the deficit and BP is the current balance of payments.

When the domestic private sector tries to increase its saving, there is a contraction of demand, income and output (unless exports increase). As a result imports too reduce (because income is lower). The higher propensity to save also leads to an increase in the government’s budget balance.

So in the chart you see a dramatic fall in the current account deficit and a huge increase in the government’s budget deficit. (The term “Nation” is used in the chart because the current balance of payments is the difference between the incomes and expenditures of all domestic sectors of a nation).

The situation is not atypical of recent (post crisis) behaviour of other nations’ sectoral balances but the fall in the external sector balance in this case is striking, though the same could be said for various deficit nations in the Euro Area.

The Banco de España – whose short-term projections are usually accurate – also said today that unemployment will hit 23.4% in 2012!

Martin Wolf wrote a blog post yesterday on FT: Understanding sectoral balances for the UK where he compares the sectoral balances for the United Kingdom and the United States.

To me both the similarities and differences are interesting. The following charts are from his post:

The Bank of England released the semiannual Financial Stability Report, December 2011 today. Complete book here. These reports have a lot of information, in addition to being well-written, well-formatted and colourful.

The following graph shows how international banks’ funding from US Money Market Mutual Funds changed during the year.

It also plots the Net International Investment Position (the negative of a nation’s debt) – which I have plotted many times in this blog (see here and here for example) and linked to other sources who have plotted it recently and is the reason for my writing this post!

It also has a chart on global imbalances with a focus on EA imbalances

Nice report. Go read.

Update: FT Alphaville’s post BoE charts, UK banks’ gloom also discusses some (different) charts from the report.

The OECD released its Economic Outlook recently. The preview is available here but download is for subscribers. Else if you are an FT subscriber, you can get it from FT Alphaville’s Long Room.

A few interesting charts (at least for me):

(click to enlarge)

Most Economists (except a few good ones), following the work of Mundell, Fleming and Friedman believed that in floating exchange rate regimes, the invisible hand will work to remove imbalances. Unfortunately, this has not happened and it has taken the crisis for them (most of them actually!) to realize that there is no mechanism and it is still unclear if they understand this.

There are some dissenters among Post Keynesians, such as Randall Wray, who do not consider current account deficits as an imbalance. See this blog post. Also see Reserve Bank of Australia’s Guy Dibelle’s speech In Defense of Current Account Deficits from July 2011.

An intuition I see often displayed in blogs is that these numbers are small and hence not problematic! My view is that these imbalances are kept low by keeping demand low. More importantly, these imbalances (deficits) add to the stock of external debt (because a deficit in the current account increases net indebtedness to foreigners) and this gets out of control sometimes leading to deflation of demand and/or seeking help from the IMF. So “low” imbalances accumulate to a huge net indebtedness.

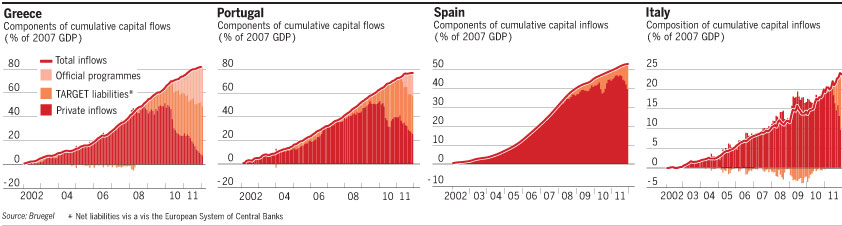

There is an informative graph on the financing needs of Greece, Ireland and Portugal:

The report also charts sectoral balances for the Euro Area!

(click to enlarge)

The Euro Area as a whole seems healthy, and it is imbalances within that are causing the troubles.

It seems Italy’s current account is worsening:

Turkey’s current account attracts a lot of attention and challenges look like this:

Turkey’s currency Lira has depreciated a lot recently

In Post Keynesian theory, the exchange rate is determined in a beauty contest in addition to demand and supply for financial assets. Sudden movements can be very painful and hence nations face a balance of payments constraint – success of nations depends on how producers do in international markets. In words of Wynne Godley,

For growth to be sustainable, it is essential that the management of domestic demand be complemented by the management of foreign trade (by whatever policies) in such a way that the net balance of exports less imports contributes in parallel to the expansion of demand for home production.

At the global level, since not everyone can be net exporting, the problem of global imbalances affects everyone, and new changes are required on how the global economy is run.