Does it matter? Yes and No. Will have to wait for the markets to open tomorrow, although SPX and EURUSD moved a bit after FT put out the news.

The Euro Area monetary union has designed itself to be dependent on rating agencies. For example, the “Eurosystem Credit Assessment Framework” outlines what kind of collateral are acceptable for borrowing (by banks) from their home National Central Bank. So eligibility and “haircuts” depend on ratings. If a national government’s rating gets downgraded, most private sector securities issued by the nation can be impacted. It is true that for a while, some issuers had their ratings higher than their sovereigns (possible!), time has arrived when they will be impacted too. With a general shortage of collateral, this will make the situation worse.

And of course, if markets start pricing a higher credit risk based on S&P’s opinion, there needn’t be an explanation of how things can go wrong.

Wolfgang Münchau’s strong views are always worth reading. Here’s from today

Click the above to go to the FT page if you have a subscription. Else you can read it via Business Spectator

Münchau says

With five days to go, the world is waiting for a big political signal. What I fear is a fudge, consisting of a multi-annual fiscal retrenchment, no eurobond, at most a temporary debt redemption instrument. The ECB will provide liquidity measures to stabilise the financial sector, and it will also provide a backstop for the bond markets. But I find it hard to see how Mr Draghi can agree an unlimited guarantee in the absence of a political union and a eurobond. A strengthened stability pact is not a fiscal union.

The way the negotiations are going now, I can see a compromise, but no solution.

This is a continuation of posts The Eurosystem: Part 1, Part 2, and Part 3 in which I went through a description of the payment system TARGET2 both domestic and cross-border and the process of how banks obtain reserves from the Eurosystem.

This post will go into the details of the Eurosystem operations. Like all central banks, the ECB simply targets interest rates, in particular the EONIA – the Euro Overnight Index Average . It is “[a] measure of the effective interest rate prevailing in the euro interbank overnight market. It is calculated as a weighted average of the interest rates on unsecured overnight lending transactions denominated in euro, as reported by a panel of contributing banks” according to the ECB website.

It should be noted outright that at some places in the ECB website, there are claims that it controls the money stock. A closer investigation shows no sign of the ECB doing anything of the sort and this claim is just a rhetoric. The Eurosystem is acting just like other central banks, changing short term interest rates and attempting to impact demand. It is impossible for any central bank to control the money stock. I had two posts on money endogeneity: Horizontalism and More On Horizontalism.

Reserve Requirements

Credit Institutions (banks) have an account at their home NCBs and have to maintain a minimum of 2% of their liabilities subject to reserve requirements. The ECB can change this from 2%, but it has never done this so far. Different central banks have different rules on which liabilities are to be included when calculating reserve requirements. For the Eurosystem, overnight deposits, deposits with maturity up to two years are included and so are debt securities with maturity up to two years. Repos, liabilities vis-à-vis other credit institutions including the Eurosystem, debt securities with maturity greater than two years are not included.

Deposits subject to reserve requirements are remunerated at the rate of the main refinancing operations (MROs).

Needless to say, reserve requirements do not reduce banks’ ability to make loans – since loans make deposits and deposits make reserves.

How do banks, as a whole, get the extra (not excess) reserves after they make loans? Either via Standing Facilities, which we consider next or through Open Market Operations.

Standing Facilities

The Eurosystem uses a corridor system for targeting interest rates. Banks can use the deposit facility and are paid interest on excess reserves and can borrow against eligible collateral under the marginal lending facility. For latter, how much? As much as they can, provided they have collateral. According to an old document from the ECB, saying the same:

So the interest rates on the deposit and marginal lending facilities act as a corridor.

In “good times”, banks will lend all their excess reserves to other credit institutions. Since the Eurosystem is adjusting the amount to reserves to hit its interest rate target, some banks may fall short of reserves which they can easily borrow from other banks. Because of uncertainty, some banks will be driven to the marginal lending facility and the Eurosystem will try to fine tune to reduce this. In may also be the case that the banking system as a whole is left with excess reserves and the Eurosystem may try to fine tune this in reverse direction (and will in “good times”). We will see how this happens in the next section.

For what happens during the day, see the end of Part 1 of this series.

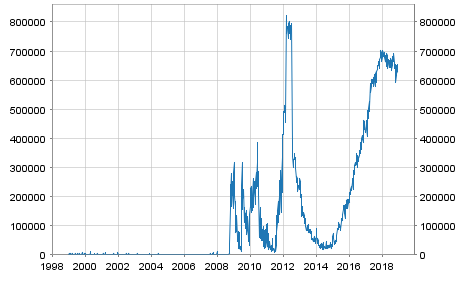

But … the crisis hit, and banks became suspicious of other banks’ creditworthiness and this led to a freeze in the interbank market. Banks were cautious in lending each other and also about their own liquidity needs. Thus, they kept a lot of deposits at their home NCB. So one hears of banks “parking” a lot of funds at the Eurosystem. The following chart from the ECB Statistical Data Warehouse highlights the stress in the interbank markets. The y-axis is in Millions of Euros.

Chart updated 6 Dec 2018, as the previous link was broken.

Before we go into Open Market Operations, a table summarizing the Eurosystem’s operations (from the same document linked above)

Government Deposits

For reasons not clear to me, monetary policy documents do not emphasize an important fine tuning operation – shifting of government deposits between NCBs’ and banking system’s books. Movement of funds into and from the government’s account at its home NCB can cause a lot of errors in forecasting liquidity and can cause fluctuations in the rate at which banks are lending each other overnight. At the same time, if managed sufficiently well, it becomes a good tool for fine-tuning! This link from the ECB’s website has some discussion on this.

Open Market Operations

Via, open market operations, the Eurosystem manages banks’ needs for reserves. It neither controls the money stock in the Euro Area nor controls the amount of reserves in any sense of the usage of the word “control”. It may pursue a non-accommodating or a dynamic policy, where it hikes the interest rate, depending on the growth of the money stock but gone are the days of Monetarism! The Eurosystem is defending its target rate, the main refinance rate, which is usually mid-way between the rates for the deposit facility and the marginal lending facility. In recent times, due to banks’ high credit risk, it has lost control of this.

As per Table 1 above, the Eurosystem categorizes its operations as

main refinancing operations,

longer-term refinancing operations,

fine-tuning operations and

structural operations.

We can also describe them – as done by the “Monetary Policy Implementation” document – as follows:

Reverse transactions: MROs, LTROs, Fine-tuning Reverse Operations and Structural Operations;

Outright Transactions;

Foreign Exchange Swaps;

Issuance of ECB Debt Certificates, Collection of Term-deposits.

Before we get into a description of the above items, it should be made clear from the start, that the reader should keep in mind the similarities and differences between this and the procedures adopted by the Federal Reserves in the United States. As mentioned in Part 1, the Federal Reserve and the banking system can be described as asset-based type, while the monetary system in the Euro Area as an overdraft monetary system. (It should also be made clear that “overdraft” here does not mean national governments have an overdraft facility at their home NCB – they don’t have).

For example, it is easy to confuse MROs and LTROs with the (non-permanent) open market operations done by the Fed. The confusion arises because both MRO/LTROs and the Fed’s open market operations are carried out using repurchase agreements (repos). I will have another blog post on the Federal Reserve procedures, but suffice to say here that the Fed’s repos are more comparable to Fine-tuning Reverse Operations.

Reverse Transactions

As mentioned, earlier banks as a whole in the Euro Area obtain all reserves by directly borrowing from the Eurosystem. An exception is that in recent times, banks have seen their reserves increase due to the ECB’s two programs – Securities Markets Programme and Covered Bond Purchase Programme.

Let us consider MROs first.

Every week, the Eurosystem refinances the liquidity needs of the banking system via this operation. According to the implementation document,

- They are liquidity-providing operations. – They are executed regularly each week. – They normally have a maturity of one week. - They are executed in a decentralised manner by the National Central Banks. - They are executed through standard tenders. – All counterparties fulfilling the general eligibility criteria may submit tender bids for the main refinancing operations. - Both tier one and tier two assets are eligible as underlying assets for the main refinancing operations.

So every week, the Eurosystem lends banks amounting billions of Euros via an auction but these are executed in a decentralised manner by the NCBs as repurchase agreements. (Edit: 21 Dec 2011: A bit incorrect to term MRO/LTROs as “repos”). During the week, funds flow in all directions and banks will borrow from each other.

What about LTROs?

These are almost similar to the MROs, except that they are executed every month and normally have a maturity of three months. In recent times, the ECB has been more accommodative and has offered LTROs with longer maturities such as six months.

Since the frequency of MROs is one week, there needs to be some tool for the Eurosystem during the week to fine tune reserves so that interbank lending rates do not deviate from the target. So Fine-tuning Reverse Operations. These need not have fixed maturities and can be done in short notice but executed in a decentralised manner by the NCBs. About Structural Reverse Operations, I have nothing to say!

Outright Transactions, FX Swaps, ECB Debt Certificates & Term Deposits

In addition, the Eurosystem may employ other tools to provide or remove liquidity such as outright purchases or sales of domestic securities or entering into foreign exchange swaps with financial institutions. These are generally decentralised i.e, executed by the NCBs but the ECB may sometimes be involved. Collection of term deposits and issuance of ECB debt certificates absorb liquidity (i.e., reserves). The former is executed by the NCBs. Debt certificates are settled in a decentralised manner by the NCBs. Another difference between the two is that the former is not marketable, while the latter is.

Conclusion

A bit boring, wasn’t it? Haven’t yet covered ELA (Emergency Loan Assistance), SMP (Securities Markets Programme) and CBPP (Covered Bond Purchase Programme). My aim was to detail out the monetary operations so that we know what the Eurosystem does, what it doesn’t and what it can do (and what it cannot do!). Probably ELA, SMP & CBPP for the last part in the series – Part 5.

Addendum

How does the ECB change short term interest rates in normal times? By a simple announcement. Banks will automatically start lending each other at the target rate. MROs are done weekly, and there will be no additional MRO that needs to be done post/pre the announcement. Neither do fine-tuning reverse operations change in volume because of the decision.

John Cassidy of The New Yorkercomments on the failed austerity policies in the UK:

During the past eighteen months, a callow and arrogant Chancellor of the Exchequer, empowered by a hands-off Prime Minister and backed by the bulk of the country’s financial and media establishment, has needlessly brought Britain to the brink of another recession by embracing draconian spending cuts that hark back to the early nineteen-thirties. Rather than changing course and taking measures to boost growth, the Conservative-Liberal coalition is doubling down on austerity. On Tuesday, it announced plans to extend its cuts for two more years, until 2016-2017. “Until now, we had been thinking of four years of cuts as unprecedented in modern times,” Paul Johnson, the director of the non-partisan Institute for Fiscal Studies, said. “Six years looks even more extraordinary.”

The following was written in The Guardian in early 1981. Click to enlarge. And click again to enlarge.

According to FT,

In the early 1980s, when recovery from global recession was slow, the jobless rate more than doubled, soaring from 5.3 per cent in August 1979 to 11.9 per cent in 1984.

Seems nothing has changed in the last 30 years! Although, the Bank of England has dropped the bank rate to 0.5%, the present budget policies of the UK Government is a hangover of Thatcherism.

The Bank of England released the semiannual Financial Stability Report, December 2011 today. Complete book here. These reports have a lot of information, in addition to being well-written, well-formatted and colourful.

The following graph shows how international banks’ funding from US Money Market Mutual Funds changed during the year.

It also plots the Net International Investment Position (the negative of a nation’s debt) – which I have plotted many times in this blog (see here and here for example) and linked to other sources who have plotted it recently and is the reason for my writing this post!

It also has a chart on global imbalances with a focus on EA imbalances

Nice report. Go read.

Update: FT Alphaville’s post BoE charts, UK banks’ gloom also discusses some (different) charts from the report.

In the previous post in this series The Eurosystem: Part 2, I discussed cross-border flows within the Euro Area. With exceptions, most of these flows are current balance of payments and balance of payments financing flows. Of course there are other flows with the world outside the EA17 and these flows flow via the correspondent banking arrangements banks have put in place and not the topic of discussion in this series.

The cross-border flows are important for the Euro Area since as a whole, the Euro Area’s balance of payments is almost in balance.

So the Euro Area current account was in a deficit of €11.7bn in 2011Q3 and a net indebtedness of €1.35tn to the rest of the world at the end of Q3, or 14.5% of GDP. So most of external imbalances of the EA17 nations are within the Euro Area.

Back to TARGET2 flows: there was a debate among some economists on various matters related to these flows. Some even went on to suggest that these flow affect credit in Germany because the nation was financing the current account of the other nations. From an exogenous money viewpoint, this reduces banks’ ability to provide loans to their customers! (which is incorrect because money is not exogenous). The replies tried to disprove it by using the argument that attempted to prove that the NCBs were not financing the current account. Sorry no links.

This is a small post and my point is to show that since TARGET2 is designed to automatically change the balance sheets of the NCBs, the debate whether the NCBs finance the flows or not is a bit counterproductive. Of course having said this, I wish to highlight the fact that the item “Claims within the Eurosystem” (in either assets or liabilities) is definitely recorded in the balance of payments and the international investment position as can be seen below for the case of Spain.

Of course, the “Claims Within the Eurosystem” is just one item in the financial account and the international investment position, so not the whole of the current account deficit is financed this way. One minor advantage is that this part of the gross indebtedness of a whole deficit nation is at the ECB’s main refinancing rate, which is much lower than the effective interest rate deficit EA nations are paying on their gross liabilities to foreigners. This is not worthy of further attention, though.

How long can these flows continue? As long as the banks have sufficient collateral to provide to their home NCB. When banks run out of collateral (eligible for borrowing from the Eurosystem), emergency measures have to be taken and a future post in this series will discuss the Emergency Loan Assistance Program (ELA) used by NCBs.

[I welcome your comments. I have a “Zero Comments Policy” as opposed to a “No Comments Policy”. I like being notified of a comment.]

The OECD released its Economic Outlook recently. The preview is available here but download is for subscribers. Else if you are an FT subscriber, you can get it from FT Alphaville’s Long Room.

A few interesting charts (at least for me):

(click to enlarge)

Most Economists (except a few good ones), following the work of Mundell, Fleming and Friedman believed that in floating exchange rate regimes, the invisible hand will work to remove imbalances. Unfortunately, this has not happened and it has taken the crisis for them (most of them actually!) to realize that there is no mechanism and it is still unclear if they understand this.

There are some dissenters among Post Keynesians, such as Randall Wray, who do not consider current account deficits as an imbalance. See this blog post. Also see Reserve Bank of Australia’s Guy Dibelle’s speech In Defense of Current Account Deficits from July 2011.

An intuition I see often displayed in blogs is that these numbers are small and hence not problematic! My view is that these imbalances are kept low by keeping demand low. More importantly, these imbalances (deficits) add to the stock of external debt (because a deficit in the current account increases net indebtedness to foreigners) and this gets out of control sometimes leading to deflation of demand and/or seeking help from the IMF. So “low” imbalances accumulate to a huge net indebtedness.

There is an informative graph on the financing needs of Greece, Ireland and Portugal:

The report also charts sectoral balances for the Euro Area!

(click to enlarge)

The Euro Area as a whole seems healthy, and it is imbalances within that are causing the troubles.

It seems Italy’s current account is worsening:

Turkey’s current account attracts a lot of attention and challenges look like this:

Turkey’s currency Lira has depreciated a lot recently

In Post Keynesian theory, the exchange rate is determined in a beauty contest in addition to demand and supply for financial assets. Sudden movements can be very painful and hence nations face a balance of payments constraint – success of nations depends on how producers do in international markets. In words of Wynne Godley,

For growth to be sustainable, it is essential that the management of domestic demand be complemented by the management of foreign trade (by whatever policies) in such a way that the net balance of exports less imports contributes in parallel to the expansion of demand for home production.

At the global level, since not everyone can be net exporting, the problem of global imbalances affects everyone, and new changes are required on how the global economy is run.

The UK Office of National Statistics released the 2011 editions of the “Blue Book” and the “Pink Book” recently.

The UK Gross Domestic Product was £1,394 billion in 2009 and £1,458 billion in 2010.

In the last 20-40 years, external assets (and liabilities) have grown to a huge multiples of GDP. Hyman Minsky worried about gross assets and liabilities in addition to net assets/liabilities and showed the importance of “gross”. At the end of 2010, according to the Pink Book, total value of assets held abroad by UK residents was equivalent of £9,961 billion while liabilities to foreigners was £10,159 billion, leaving the United Kingdom with a net asset position of minus £197 billion.

With talks of a Eurocalypse not so unthinkable these days, countries’ exposure to the Euro Area is the natural question to ask. Since London is a financial center and the United Kingdom is close to the Euro Area, it is likely to have more exposure to the Euro Area than other nations. The Pink Book 2011 edition gives the geographic breakdown of assets and liabilities only till 2009, unfortunately. Anyway the statistics below

by type:

(click to enlarge)

and in more detail on countries but consolidated across all resident sectors:

(click to enlarge)

Needless to say, huge!

The column for “Derivatives” shows assets valued less than £1,000 billion but here too there may be hidden exposures, since there can be a lot of netting, even though Derivatives appear in both Assets and Liabilities.

If there are problems in the Euro Area, assets held by residents will be impaired (such as due to defaults) and this is already happening at a lesser scale compared to the “unthinkable”. A depreciation of the Euro to the Pound Sterling will also cause revaluation losses for UK residents. On the other hand, to maintain credit ratings, it will be difficult for the UK to default on its liabilities, increasing UK’s net indebtedness to the rest of the world by a huge amount. It is really difficult to forecast how severe the crisis can be, but these numbers suggest it can be devastating to the extreme.

There are second order effects. For example, UK residents hold assets in the United States and if these assets fall in market value due to a crisis situation, there could be a further deterioration in the gross value of UK Assets held abroad.

With EFSF bonds not appealing to investors even in a flight to quality environment, and European politicians’ plans losing credibility, and the ECB’s Securities Markets Programme losing its effect, the only way forward is for the ECB to put explicit ceilings on government bond yields. The reason it is hesitant in doing it is because it creates a moral hazard problem. (See Mervyn King’s Got A Point).

Of course, there seems to be no alternative (except rumours of a €600 billion bailout for Italy!), so challenging times ahead for the ECB.

Update: Wolfgang Münchau of FT thinks the Eurozone has only a few days! Link

Economists are increasingly recognizing the Euro Area problems as a balance-of-payments crisis, in addition to realizing that the Euro Area national governments cannot finance their deficits by making a draft at the Eurosystem in extreme emergency.

With a few exceptions, the benchmark cost of credit in each euro-zone country is related to the balance of its international debts. Germany, which is owed more than it owes, still has low bond yields; Greece, which is heavily in debt to foreigners, has a high cost of borrowing (see chart 2). Portugal, Greece and (to a lesser extent) Spain still have big current-account deficits, and so are still adding to their already high foreign liabilities. Refinancing these is becoming harder and putting strain on local banks and credit availability.

The higher the cost of funding becomes, the more money flows out to foreigners to service these debts. This is why the issue of national solvency goes beyond what governments owe. The euro zone is showing the symptoms of an internal balance-of-payments crisis, with self-fulfilling runs on countries, because at bottom that is the nature of its troubles. And such crises put extraordinary pressure on exchange-rate pegs, no matter how permanent policymakers claim them to be.

The magazine also had another nice article recently: Is this really the end?. Here is a collection of covers from the magazine in recent times on the Euro.

Paul Krugman has a blog post today titled Death By Accounting Identity, commenting on Martin Wolf’s FT Article Why cutting fiscal deficits is an assault on profits, where Wolf talks about the sectoral balances identity made famous by Wynne Godley. I guess the better way to put it is that Martin Wolf is trying to make the accounting identity famous.

A Damascene Moment

In his book with Marc Lavoie, Wynne Godley wrote in his part of Background memories (by W.G.)

… In 1970 I moved to Cambridge, where, with Francis Cripps, I founded the Cambridge Economic Policy Group (CEPG). I remember a damascene moment when, in early 1974 (after playing round with concepts devised in conversation with Nicky Kaldor and Robert Neild), I first apprehended the strategic importance of the accounting identity which says that, measured at current prices, the government’s budget deficit less the current account deficit is equal, by definition, to private saving net of investment. Having always thought of the balance of trade as something which could only be analysed in terms of income and price elasticities together with real output movements at home and abroad, it came as a shock to discover that if only one knows what the budget deficit and private net saving are, it follows from that information alone, without any qualification whatever, exactly what the balance of payments must be. Francis Cripps and I set out the significance of this identity as a logical framework both for modelling the economy and for the formulation of policy in the London and Cambridge Economic Bulletin in January 1974 (Godley and Cripps 1974). We correctly predicted that the Heath Barber boom would go bust later in the year at a time when the National Institute was in full support of government policy and the London Business School (i.e. Jim Ball and Terry Burns) were conditionally recommending further reflation! We also predicted that inflation could exceed 20% if the unfortunate threshold (wage indexation) scheme really got going interactively. This was important because it was later claimed that inflation (which eventually reached 26%) was the consequence of the previous rise in the ‘money supply’, while others put it down to the rising pressure of demand the previous year. …

I believe Wynne Godley discovered this identity while working for the British Treasury in the ’60s – at least the identity relating two sectors – domestic private sector and the government sector, but the damascene moment happened in 1974. The accounting identity is also used heavily in his 1983 book Macroeconomics, with Francis Cripps.

Charles Goodhart

Charles Goodhart also seems to be making use of the accounting identity (and a mental model built around this identity) in his recent Voxeu post Europe: After the Crisis. The difference is that in Charles Goodhart’s writing, fiscal policy is given less importance than monetary policy.

He talks of three implicit and incorrect assumptions:

The first, and most important, incorrect assumption was that a private-sector deficit in any country, matched by a capital inflow (current account deficit), should not be potentially destabilising.

The thinking was that the private sector must have worked out how to repay its debts before incurring them.

The second misguided assumption was that, in a single monetary system, local current account conditions not only cannot be calculated, but do not matter.

The third was that the public sector deficit of a member country is just as damaging when it is matched by a national private sector surplus, as by capital inflows.

I think each of these points is really insightful.

The first assumption is reminiscent of the economic agent in models who has a perfect foresight. The agent must have seen the future very well and would have calculated well in advance that things will go well. Consolidate all agents and we have the first assumption.

The second assumption is extremely well presented. People, especially economists asked – if the states in the United States used the same currency, why not Europe? The pitfall in this assumption is assuming away the U.S. Federal Government which makes fiscal transfers without anyone noticing.

The third assumption has to do with the lack of understanding the various causalities linking the three financial balances.Goodhart also goes into providing ideas for the design of “The fiscal counterpart to a monetary union”. One point I liked was on transfer dependency:

For a stabilisation instrument to be pure and effective, three principles are key (see Goodhart and Smith 1993 for details):

The instrument should be triggered following changes in economic activity but its intervention should be halted as soon as no further changes occur, irrespective of the level at which the economy has again become stable.

Otherwise, the instrument would perform not only a stabilisation function, but also play a redistributive role. Such an ‘impurity’ is typical for traditional fiscal policy measures, but should be avoided in the Community context as it may perpetuate adjustment problems and induce transfer dependency.

….

Goodhart also makes a nice point on Japan – something (a part of it) you can see me writing in the Chartalists’ blogs’ comments section:

This analysis implies that the Eurozone needs a wholesale reorientation of the stability conditions. They must be refocused towards concern with external debt, and deficit, conditions and much less single-minded focus on the public sector finances.

If a member country is in a Japanese condition with a huge public-sector debt, but fully financed domestically, with a current-account surplus and large net external assets, then its debt should entirely be its own concern, and not subject to censure or control by any outside body, whether in a monetary union, or not. Of course, such greater attention to external, especially current-account, conditions needs to be more nuanced, since deficits, and external debts, incurred to finance tradeable goods production subsequently should provide the extra goods to sell to pay off such debts.

Japan’s public debt of 200% of GDP is quoted in rhetoric about public debt, but it is forgotten that Japan is a creditor nation and hence not always great to compare it with other nations.

Another recent article by Goodhart starts off well:

There are two main problems to be faced in any attempt to improve the architecture of international macro‐economic and financial oversight. The first is structural; the second is analytical. The first difficulty resides in the discord between having a system of national sovereignty at the same time as an international market economy, …