This is a nice interview of Marc Lavoie with Marshall Auerback organized by the Institute for New Economic Thinking (INET) in which he talks mainly about his new book Post-Keynesian Economics: New Foundations.

{kind=link}

This is a continuation of the post from the end of 2014, although reading that isn’t necessary.

In a new paper, Marc Lavoie continues his debate with Sergio Cesaratto on whether the Euro Area crisis is a balance-of-payments crisis or not. For the sake of completeness, here’s the list of papers, with references copy-pasted from Marc’s latest paper. Not all links are final versions and some may not be available to read in full).

As mentioned in my part 1, referred to on top of this post, I agree with Sergio Cesaratto.

Sergio Cesaratto with Marc Lavoie (picture credit: Matias Vernengo)

Sergio Cesaratto with Marc Lavoie (picture credit: Matias Vernengo)

Marc Lavoie’s main point in the final paper seems to be that, “Eurozone countries can never run out of TARGET2 balances, which can take unlimited negative values, so that the evolution of the balance of payments cannot be the source of the crisis”.

This is not accurate in my view. Although the rules of the Eurosystem allow unlimited and uncollateralized credit facility between the Euro Area NCBs and the ECB, one has to look at the counterpart to the T2 imbalances. If an economic unit transfers funds across border from country A to country B, this first results in a reduction of balances of banks in country A at their NCB and may result in an intraday overdraft (“daylight overdraft” in U.S. language), usage of the marginal lending facility with the NCB, an MRO, or an LTRO and finally ELA in late stages of a crisis (if capital outflow is large).

Marc himself mentions this point in his latest paper:

If a Eurozone country is running a current account deficit that banks from other Eurozone members decline to finance, or if it is subjected to capital outflows, then all that happens is that the national central bank of that country will be accumulating TARGET2 debit balances at the ECB. There is no legal limit to these debit balances. The national central bank with the debit balances, which pay interest at the target interest rate, has as a counterpart in its assets the advances that it must make to its national commercial banks at that same target interest rate. And the commercial banks can obtain central bank advances as long as they show proper collateral. Why would the size of current account deficits or TARGET2 debit balances worry speculators? There might be a problem with the quality of the loans that have been granted by the banks, or with the size of the government debt, but that as such has nothing directly to do with a balance-of-payments problem.

[italics: mine]

But that is the case! It’s because of balance-of-payments. Nations who had high indebtedness to the rest of the Euro Area saw more capital flight. This is because in times of crisis, there is a home bias and international investors are likely to sell securities abroad and repatriate funds home. Large current account imbalances lead to a large negative net international investment position. (It’s of course also true that revaluations are important, and this is what happened in the case of Ireland). So when non-residents sell securities to domestic investors, banks are likely to get into a bad situation because they have to accommodate these transfer of funds and are losing central bank balances on a large scale.

It is precisely nations which had worse net international investment positions which were affected as charted in my previous post on this.

Now moving on to definitions: what is a balance-of-payments problem? The simplest definition is the problem for residents in obtaining finance from non-residents. Greece precisely has been struggling to obtain funds from non-residents.

So I do not agree with Marc’s view that:

Cesaratto, as others, is adamant that the Eurozone crisis is a balance-of-payments crisis, whereas I believe, as others do, that this is a side issue.

Marc Lavoie also says that the people arguing for this view are implicitly assuming some kind of “excess saving” view on all this:

In discussions with colleagues who support a “current account deficit” view of the Eurozone crisis, I sometimes get the impression that they are also endorsing a kind of “excess saving” view of the economy. They tell me that current accounts deficits are unsustainable within the Eurozone because the core Eurozone countries will refuse to lend to the periphery and will thus prevent these countries from financing economic activity. This seems wrong to me.

I disagree with this. It’s precisely because residents’ liabilities are large compared to their financial assets that they have to rely on non-residents/foreigners. And during the crisis a lot of capital outflow has happened and this precisely shows that non-resident private investors are unwilling to lend again on the same scale as before. This obviously means that to obtain finance, governments of nations affected have to take the help of the official sector abroad, such as from governments, the ECB and the IMF. If TARGET2 alone could do the trick, is the Greek government foolish to go abroad?

It is of course true that the design of the Euro Area was faulty. But that still leaves open the question about why Germany is not facing a crisis as severe as Greece. The design view cannot explain this. Any country (or all countries) in the Euro Area could have faced a crisis. There is a pattern here and that is where balance-of-payments comes in.

This debate is an interesting one. Both Sergio Cesaratto and Marc Lavoie agree on almost everything, except this BIG thing.

Of course this also spills over to policy proposals. Marc Lavoie believes that the European Central Bank can guarantee that all nations can have independent fiscal policies (by promising to buy all government debt which the financial markets isn’t interested in purchasing). Sergio Cesaratto is clear on this (and I agree very much) – in another paper Alternative Interpretation of a Stateless Currency Crisis:

A more resolute role of the ECB as lender of last resort accompanied by fine-tuned expansionary fiscal policies can only be imagined in a different political and institutional framework, quite close to that of a political union.

Let’s consider what happens if there is no federal government and if the ECB is the main supranational authority (ignoring other supranational institutions which have limited powers). Suppose the ECB were to guarantee the debt of governments of all Euro Area nations. There’s nothing to prevent, say, the government of Finland to increase the compensation of its employees every year by a huge percentage and thereby affecting Finnish corporations’ compensation of its employees. This will result in a reduction of competitiveness of Finnish producers and Finnish resident economic units will rely more on goods and services produced abroad. This will raise Finland’s net indebtedness to the rest of the Euro Area and the world. If someone believes that this debt is not a problem, how about the inflationary impact of this rise in demand on the rest of the Euro Area?

So the solution lies in bringing down the balance-of-payments imbalances (both negative and positive ones such as that of Germany). This requires a supranational institution, which is a central government. National governments would have rules on their budgets but the central government — since its goals and objectives are different — wouldn’t be bound by any rules. Wage rises would need to be coordinated. And as I argue in this post, fiscal transfers also plays a role of keeping imbalances in check.

Of course there are many other economists who also argue that the Euro Area problem is a balance-of-payments problem, but with a different motive. Their argument is to blame the nations in crisis instead of taking a humanist approach.

To summarize, the Euro Area problem wouldn’t have been a balance-of-payments problem had the official sector promised to act as a lender of the last resort to national Euro Area governments without any condition. As long as there are conditions, it is a balance-of-payments problem. One cannot pretend that the European Central Bank has or can be given such powers to lend without any condition. And hence the Euro Area crisis is a balance-of-payments problem.

In an Op-Ed for The New York Times, Japan’s Economy, Crippled by Caution, Paul Krugman is seen using a highly Monetarist language:

As I said, you might think that ending deflation is easy. Can’t you just print money? But the question is what do you do with the newly printed money (or, more usually, the bank reserves you’ve just conjured into existence, but let’s call that money-printing for convenience). And that’s where respectability becomes such a problem.

When central banks like the Federal Reserve or the Bank of Japan print money, they generally use it to buy government debt. In normal times this starts a chain reaction in the financial system: The sellers of that government debt don’t want to sit on idle cash, so they lend it out, stimulating spending and boosting the real economy. And as the economy heats up, wages and prices should eventually start to rise, solving the problem of deflation.

…

… When you print money, don’t use it to buy assets; use it to buy stuff. That is, run budget deficits paid for with the printing press.

Now, there are several things wrong about this. The most important one is the implicit assumption in the “model” that fiscal expansion via increased government expenditure is about neutral and that domestic demand is boosted only because of the way in which the government debt is financed – i.e., central bank purchases of government debt. In other words, Krugman is saying that if there is deflation and if there is an expansion of fiscal policy via a rise in say government expenditures, it will have little effect when the central bank doesn’t purchase government debt. Put it in another way, it is saying that the government expenditure multiplier effect acts mainly because of central bank purchase of government debt and not because of the increase in government expenditure per se.

This is silly intuition and the cause of this is the notion that fiscal policy is more or less neutral except in special circumstances.

In reality, it is the other way round. If the government expenditure rises, and if the central bank purchases government debt, the rise in output is mainly attributable to the former. This can of course be seen in a stock-flow consistent model but can also be seen by simple accounting and flow of funds. A rise in government expenditure on goods and services raises output directly and also via the multiplier effect. The central bank has a huge control over interest rates and the additional debt is simply absorbed by the bond markets easily. There’s no competition with other borrowers as the wealth of the private sector rises. In addition, if the central bank purchases government debt, it is hardly clear if households know if inflation is going to rise and increase their consumption because of “inflation expectations”. Even if they think that if inflation is set to rise, they might reduce consumption as inflation might reduce their real wealth.

Which is not to say that asset purchase programs of the central bank or “quantitative easing” has no effect on demand and output. It works via capital gains in wealth leading to higher consumption and the feedback effects of this. It also works if economic units shift their portfolios to buying non-financial assets. The effect of all this is unclear. In addition, as mentioned earlier, casual Monetarism like the language used by Paul Krugman mixes up correct attributions of government expenditure and central bank government debt purchases on output, misleading everyone.

Simply say “raise government expenditures”. Why all this casual Monetarism with “printing presses”?

Cullen Roche – in response to Paul Krugman – says Keynesians should learn to love tax cuts. His argument is that since Keynesians believe in the principle of effective demand and that since tax rate cuts boosts domestic demand and hence output, it is surprising to find Paul Krugman not favouring tax cuts.

Tax cuts raise output by increasing disposable incomes of economic units who will raise their expenditures in response. This via a multiplier effect will raise output. But it’s not as if tax rate cuts is the only tool available to the government.

Let’s see 4 different ways the government can boost domestic demand:

The expansionary nature of the first three ways above is obvious. For the fourth, it depends on the numbers. So if the government raises tax rates from say 25% to 30% and increases government expenditure by 1%, it is likely contractionary. Instead, if the government increases its expenditure by 25%, it is expansionary.

These are not the only ways available for demand management. The government by coordinating with the central bank can reduce interest rates. It can make lending/borrowing easier by other ways. It can give guarantees to bonds issued by corporations, thus giving an incentive for corporations to increase expenditures. It can raise tariffs on imports. There are several ways but here those things are less relevant for now.

Each of the four ways above has a different effect on output and the distribution of income. Tax cuts usually favour economic units who earn more. Richer economic units such as rich households have a lower propensity to consume and hence this will have a smaller multiplier effect. If Keynesians favour tax cuts, they’d favour it for low earning households than for corporations.

Of course, the multiplier effect is not a complete argument in itself as the opponents might argue “So cut taxes even more according to your logic”. But at any rate, let’s see how it works.

In stock-flow-consistent models, there’s the concept of a fiscal stance toward which GDP converges for a given government expenditure G and a tax rate θ. So we have

GDP = G/θ

With that,

dGDP/GDP = dG/G − dθ/θ

So a percentage rise in government expenditure will have the same multiplier effect as a percentage fall in tax rate.

This of course is the long-run output. For the short run, the expression in the simplest Keynesian model:

GDP = G/(1 − α1·(1 − θ))

α1 < 1

The parameter α1 is the propensity to consume.

In this case, i.e., for the short run,

dGDP/GDP = dG/G − [α1·θ/(1 − α1·(1 − θ))2]·dθ/θ

By taking some values such as 0.6 for α1 and 25% for θ, you can convince yourself that a proportional rise in government expenditure is more effective than a proportional fall in tax rates. Of course, this is not a complete argument but illustrative. If a tax rate cut of x% doesn’t achieve a $1 rise in government expenditure, one can make the case for a higher tax rate cut to achieve a similar result.

Apart from that there are other implicit assumptions of the model: there is no income inequality in the simplest Keynesian models. So rich economic units will have a lower propensity to spend: households working as employees of firms with higher compensation will have lower propensity to consume. Households may have an even lesser propensity to consume out of other incomes such as interest and dividends.

So the multiplier analysis illustrates that a tax cut for richer economic units is not the same as the poorer units because the multiplier in the short run depends on the propensities to spend.

The correct stand hence is about the distributional effects of fiscal policy and the effect on output. So the correct stand is to argue for a rise in government expenditure and fair rates of taxes for economic units. Many economic units will have to pay higher taxes in this view. What’s fair of course is debatable but at least in this line of argument, souls believing in the principle of effective demand needn’t love “tax cuts”.

There is another argument for not promoting lower tax rates. This is because once tax rates are reduced, it is politically difficult to raise it if needed.

Brian Romanchuk has a nice post on how the case for productivity is something which is overstated by economists. There’s less discussion in the econoblogosphere on this. Here I’ll add a few things with a slightly different perspective.

Sometime in the historic past, nations’ economies started diverging. Some nations’ fortunes rose while others lagged behind. Nations which became rich saw high rises in productivity. It’s easy to then conclude that productivity is the raison d’être for the success or failure of nations. In fact this is what Greg Mankiw says in his textbook Principles Of Macroeconomics, 7th Edition, page 13:

The differences in living standards around the world are staggering …

What explains these large differences in living standards among countries and over time? The answer is surprisingly simple. Almost all variation in living standards is attributable to differences in countries’ productivity—that is the amount of goods and services produced by each unit of labor input. In nations where workers can produce a large quantity of goods and services per hour, more people enjoy a high standard of living; in nations where workers are less productive, most people endure a more meager existence. Similarly, the growth rate of a nation’s productivity determines the growth of its average income.

The fundamental relationship between productivity and living standards is simple, but its implications are far-reaching. If productivity is the primary determinant of living standards, other explanations must be of secondary importance … some commentators have claimed that increased competition from Japan and other countries explained the slow growth in U.S. incomes during the 1970s and 1980s. Yet the real villain was not competition from abroad but flagging productivity growth in the United States.

[bold in original, italics mine]

So although it cannot be denied that rich nations have seen rise in productivity, the above story entirely misses the reverse causality – i.e., from production to productivity. And because of that, it entirely misses the cause of success and failure of nations.

Nicholas Kaldor rediscovered the relation between rise in output and rise in productivity (which can be attributed to Petrus Johannes Verdoorn) in 1966 and interpreted the causality right: from rate of growth of production to the rate of growth of productivity. The main reason given was “learning by doing”.

This still leaves open the question about what determines production itself. Unlike the supply-side models of neoclassical theory, Kaldorians tell a story about a demand-led growth and the balance of payments constraint being the most important determinant of economic growth. Some nations had the fortune of growing fast earlier in history and in this process of cumulative causation became more competitive in the process. This not only increased their fortunes but immiserated other nations. This is because poor nations would get stuck with a balance of payments constraint and this would affect their competitiveness. Competitiveness can either be price-competitiveness or non-price competitiveness. Price competitiveness depends on pricing goods and services in international markets. This in turn depends on productivity. So nations which got an early lead in history saw rise in production and hence productivity via the Kaldor-Verdoorn process and also gained in price-competitiveness.

There is a feedback effect here. Do you see it? That’s circular and cumulative causation. The effect can be better understood by writing a model such as as done by Mark Setterfield in his chapter titled Endogenous Growth: A Kaldorian Approach in the book The Oxford Handbook Of Post-Keynesian Economics, Volume 1, Theory And Origins.

Usually the story is told with price-competitiveness. I am unaware of any model which also includes non-price competitiveness in the story.

Anyway, to conclude, cheering for productivity is not going to help the world economy. The solution is to increase production: productivity will rise when production rises. The standard story as told in Mankiw’s textbook is erroneous.

Some economic commentators, in trying to point out the importance of government deficits and debt, go for the overkill.

Exhibit:

Accounting: bank lending doesn’t increase aggr HH net worth. +HH assets, +HH liabs. Gov def spending does.

— Steve Roth (@asymptosis) August 23, 2015

Sorry for picking Steve Roth, who is generally a nice person. But this is counterproductive. If you see the comments below, a commentator who claims to be a trained accountant also agrees with Steve Roth. The bait involves saying that this argument is “technically right”. It can be technically right for several reasons but outright misleading and commentators should stop doing this. So it could be true because the act of bank loan making itself creates an asset and liability equally, so there is no increase in net assets of either households or the private sector as a whole by just one transaction. But this is not just the argument. The argument seems to be that it doesn’t increase household net worth at all even if another transaction is involved, such as a house purchase because a firm sells the house not a household and in national accounts firms are distinct from households. So much click baiting.

In this post, I show how a household’s net worth rises on sale of a house. Let’s assume that I (Household 2) am a sole proprietor of a house building firm (Firm P) and hence the ownership of the firm is not publicly traded in a stock exchange. Suppose I sell a house worth $1mn to you (Household 1). The house is sold from my firm’s inventory of houses and becomes a sale. You buy this after taking a loan from Bank A.

Now, we need some good national accounting. A good way is to just pick up Wynne Godley’s stock-flow consistent models in which he values inventories at current cost of production. See Godley and Lavoie’s book Monetary Economics, Edition 1, page 29.

Let’s suppose the current cost of production is $400,000.

Now we need another concept: own funds at book value from the 2008 SNA, Paragraph 13.71d-e:

d. Book values reported by enterprises with macrolevel adjustments by the statistical compiler. For untraded equity, information on “own funds at book value” can be collected from enterprises, then adjusted with ratios based on suitable price indicators, such as prices of listed shares to book value in the same economy with similar operations. Alternately, assets that enterprises carry at cost (such as land, plant, equipment, and inventories) can be revalued to current period prices using suitable asset price indices.

e. Own funds at book value. This method for valuing equity uses the value of the enterprise recorded in the books of the direct investment enterprise, as the sum of (i) paid-up capital (excluding any shares on issue that the enterprise holds in itself and including share premium accounts); (ii) all types of reserves identified as equity in the enterprise’s balance sheet (including investment grants when accounting guidelines consider them company reserves); (iii) cumulated reinvested earnings; and (iv) holding gains or losses included in own funds in the accounts, whether as revaluation reserves or profits or losses. The more frequent the revaluation of assets and liabilities, the closer the approximation to market values. Data that are not revalued for several years may be a poor reflection of market values.

The accounting entries are simple (I am considering increases/decreases here, so “= +” is understood as an increase in the thing on its left.)

For Household 1:

Assets | Liabilities and Net Worth |

House = +$1mn | Bank Loan = +$1mn |

For Bank A:

Assets | Liabilities and Net Worth |

Loan to Household 1 = +$1mn | Deposits of Firm P = +$1mn |

For Firm P:

Assets | Liabilities and Net Worth |

Deposits = +$1mn | Own Funds = +$0.6mn |

For Household 2:

Assets | Liabilities and Net Worth |

Own Funds at Firm P = +$0.6mn | Net Worth = +$0.6mn |

So, my (Household 2’s) net worth has risen by $600,000 by selling you (Household 1) a house.

I have in this example, intentionally chosen a privately owned firm to score a point. If the firm had been publicly owned, the house sale would have increase the firm’s net worth and my (Household 2’s) net worth would increase when the firm’s net worth reflects in the share price (which is not immediate). But I just had to show one example. It’s not just academic – many firms are family owned.

Steve Roth’s claim are similar to claim made by Neochartalists who claim that the private sector can only save if the government runs deficits and so on. All counterproductive.

The case for fiscal expansion can be made quite strongly, but not by these click bait claims.

Oh boy! Krugman could not have been more wrong about Macroeconomics than what he said recently in his blog The Conscience Of A Liberal for The New York Times. In a blog post, Competitiveness And Class Warfare, he concludes:

International competition is a mostly bogus notion; …

In a sense it is not surprising. Paul Krugman has done enough to push free trade. With that position, one is forced to take a position that competitiveness doesn’t matter (or that free trade will lead to a convergence between successful and unsuccessful nations).

The notion that balance of payments does not matter is as old as Monetarism. If it is understood that competitiveness does matter and that for a nation it hurts domestic producers and hence one needs some sort of protectionist measures goes against the notion of free trade. For neoclassical economists other than Paul Krugman, competitiveness does matter but in a different sense. They would argue that it there is divergence in performance of nations because of “loose fiscal policy” or “fiscal profligacy” and so on and that once the government balances its budget and behaves the way as per a standard textbook model, there’ll be convergence in performance because market mechanisms will do the trick. But Krugman is different. During the crisis, he has understood that fiscal policy is important and that it is not impotent as claimed by his colleagues.

There are of course other factors at play in the examples Krugman provides. Japanese producers are highly competitive but at the same time, the government of Japan didn’t expand domestic demand by fiscal expansion and so the performance of the economy of Japan has suffered. But that doesn’t mean that the competitiveness of Japanese producers doesn’t matter. Had they been less competitive, Japanese exports would have been lower than otherwise and Japan would have imported more because foreign producers would beat them at their home. Moreover, a weaker current account balance of payments would have led to a bigger government deficit and the Japanese government would have (incorrectly) tightened fiscal policy in response, with the result that both balance of payments and fiscal policy would have reduced domestic demand and hence output.

So while there are other factors affecting economic performance, none of it ever means that competitiveness doesn’t matter.

Cambridge economists were clear on this. Here’s Wynne Godley in a 1993 article Time, Increasing Returns And Institutions In Macroeconomics, in S. Biasco, A. Roncaglia and M. Salvati (eds.), Market and Institutions in Economic Development: Essays in Honour of Paolo Sylos Labini, (New York: St. Martins Press), page 79:

… In the long period it will be the success or failure of corporations, with or without active help from governments, to compete in world markets which will govern the rise and fall of nations.

In trying to defend the importance of fiscal policy, some economists such as Paul Krugman become forceful in their views about the way the world works and underplay the importance of matters such as international competitiveness. They seem to falsely believe that this strategy would work for them because accepting the importance of competitiveness would give enough chance for their opponents to argue against worldwide fiscal expansion. It is a sad and counterproductive strategy.

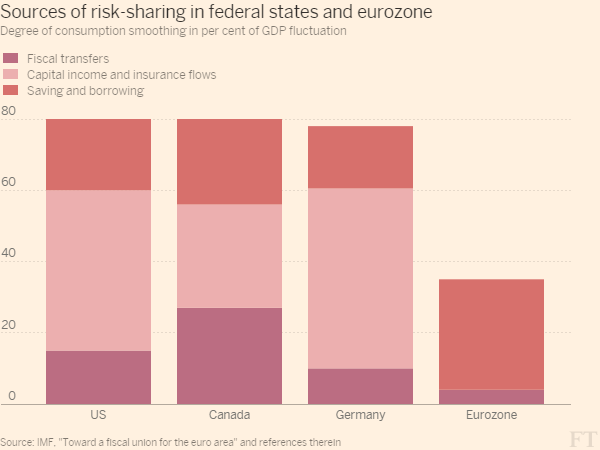

The Financial Times has a column titled Europe’s Fiscal Union Envy Is Misguided. The author echoes a recent article in The New York Times (referred here in my blog). According to the FT columnist, in the United States,

… The bulk of the risk-sharing happens through credit and capital markets – that is to say, private lending, borrowing and investment returns do most of the job of evening out regional shocks.

and,

… The best thing the eurozone can do to promote risk-sharing is to stop flirting with its own disintegration: as long as investors suspect politicians might let the currency unravel, they will hunker down behind national borders. Next, get cracking on developing the capital markets union – where there is much more reason to envy the Americans.

In addition, the FT author presents the following graph.

Let’s see how a federal system works.

There are regions with local governments but there is also a federal government which raises taxes from economic units of all regions and spends on the units. Some regions will be net recipients of such flows of funds — the government expenditure toward these regions is higher than what it receives in taxes — while others will pay more taxes than what they receive from the government. These needn’t sum to zero, as the federal government may be in a deficit.

There is one peculiar thing in the way such accounting is done. The federal government is outside all regions when studying balance of payments of each region. However for the whole group, the federal government is inside. The Sixth Edition of the IMF’s Balance Of Payments And International Investment Position Manual (BPM6) does this in a similar way for monetary unions, such as for the Euro Area. In that case, the European Central Bank and the European Parliament and other such supranational institutions are considered to be outside each nation when nations’ balance of payments statistics is produced, but inside when the balance of payments of the whole region is studied.

Now, some regions may see an improvement in their balance of payments compared to the case where there is no federal government. There are four kinds of flows which are important here when thinking about the current account balance of payments of a region:

Of course, expenditure of the federal government in the region itself may be thought of as an export, so exports in the list above is meant to exclude that and include transactions such as a private sector producer selling a car to a household in another region.

So one can roughly identify surplus regions as ones which have higher exports than imports in the definition above and others as deficit regions. These transactions of course also affect the capital and financial accounts of the balance of payments and the “regional investment position”.

Usually, one thinks of “fiscal transfers” as affecting aggregate demand. But from the above analysis, it should be clear that it also affects the regional investment position. Economic units in deficit regions also see an improvement in their net asset position. Economic units in deficit regions in aggregate will typically receive more federal government payments than what they send in taxes. The counterpart to this in the capital and financial account of the balance of payments is an improvement in their net acquisition of financial assets and net incurrence of liabilities, as compared to the case where there is no federal government. This is turn improves the regional investment position.

Of course there is still a possibility that the private sector of a union with a federal government as a whole may turn unsustainable but at least there is a regional mechanism of improvement compared to the case when there is no federal government.

To summarize, the point of the above analysis is that the financial sector as a whole cannot achieve this on its own. It takes a federal government to not only affect demand in all regions but also keep their debts in check. The workings of finances of a federal government affects the asset and liability positions of any region as a whole. The financial sector cannot take up the task of a federal government.

It’s remarkable how some economists were ahead of the time, while others such as Ben Bernanke seem to just catch up. In a recent post on his blog Ben Bernanke gives out some unorthodox ideas to resolve the Euro Area crisis.

Ben Bernanke says:

… Germany’s large trade surplus puts all the burden of adjustment on countries with trade deficits, who must undergo painful deflation of wages and other costs to become more competitive. Germany could help restore balance within the euro zone and raise the currency area’s overall pace of growth by increasing spending at home, through measures like increasing investment in infrastructure, pushing for wage increases for German workers (to raise domestic consumption), and engaging in structural reforms to encourage more domestic demand. Such measures would entail little or no short-run sacrifice for Germans, and they would serve the country’s longer-term interests by reducing the risks of eventual euro breakup.

…

Second, it’s time for the leaders of the euro zone to address the problem of large and sustained trade imbalances (either surpluses or deficits), which, in a fixed-exchange-rate system like the euro zone, impose significant costs and risks. For example, the Stability and Growth Pact, which imposes rules and penalties with the goal of limiting fiscal deficits, could be extended to reference trade imbalances as well. Simply recognizing officially that creditor as well as debtor countries have an obligation to adjust over time (through fiscal and structural measures, for example) would be an important step in the right direction.

That’s in 2015.

Compare that to the conclusion from a 2007 paper titled A Simple Model Of Three Economies With Two Currencies: The Eurozone And The USA written by Wynne Godley and Marc Lavoie for Cambridge Journal Of Economics (journal link):

… it should be noted that balanced fiscal and external positions for all could as well be reached if the euro country benefiting from a (quasi) twin surplus as a result of the negative external shock on the other euro country decided to increase its government expenditures, in an effort to get rid of its budget surplus. This case, where the surplus countries rather than the deficit countries adjust, as many authors have underlined, would eliminate the current downward bias in worldwide economic activity. Now this would require an entirely new attitude towards government deficits. One would need an anti-Maastricht approach, that would run against the Stability and Growth Pact and its neoliberal obsession with fiscal balance and government debt reduction. For instance, one would need a new Pact, that would discourage fiscal surpluses. National governments that ran budget surpluses would pay large proportional automatic levies to the European Union, who would be compelled to spend the sums thus collected in the deficit countries. In this manner, the ‘weak’ and the ‘strong’ members of the eurozone could converge towards a super-stationary state, with balanced budgets and current accounts, through an increase rather than a decrease in government expenditures and economic activity.

Alternatively, the present structure of the European Union would need to be modified, giving far more spending and taxing power to the European Union Parliament, transforming it into a bona fide federal government that would be able to engage into substantial equalisation payments which would automatically transfer fiscal resources from the more successful to the less successful members of the euro zone. In this manner, the eurozone would be provided with a mechanism that would reduce the present bias towards downward fiscal adjustments of the deficit countries. This raises the profound question as to whether in the long term it is possible to have a community of nations which have a single currency which does not have a federal budget of substantial size, and by implication a federal government to run it—a point that was made very early on in Godley (1992).

[italics in original]

Josh Barro writing for The New York Times claims that a fiscal union for the Euro Area will be an enourmous expense for its rich members.

Click to view on Twitter

He cites the example of Connecticut:

But the American fiscal union is very expensive for rich states. According to calculations by The Economist, Connecticut paid out 5 percent of its gross domestic product in net fiscal transfers to other states between 1990 and 2009; that is, its tax payments exceeded its receipt of government services by that amount. This is typical for rich states: They pay a disproportionate share of income and payroll taxes, while government services are disproportionately collected in states where people are poor or old or infirm.

This is blatantly wrong. It assumes that output of individual regions and the whole of the the Euro Area will roughly be the same with or without a fiscal union. It ignores the notion that each region may be better off because a supranational fiscal authority will have powers to raise output via expenditure and taxes which individual regions cannot achieve.

In his 1997 article Curried EMU — The Meal That Fails To Nourish for Observer, Wynne Godley made this point well (link):

A useful comparison can be made with the US. Americans often point that if would make no sense if each US state had its own currency, so what is all the fuss about? But the question should be asked the other way round. How would the US make out with no President, no Congress, no federal budget, and no federal institutions apart from the ‘Fed’ itself, plus a powerful central bureaucracy?

The analogy is useful because the United States does so obviously need a federal budget as well as a federal bank, and the activities of the two authorities have to be co-ordinated. If there is a recession, remedial (expansionary) fiscal policy at the federal level is the only proper response; it is inconceivable that corrective action could be left to component states, which have neither the perspective nor the co-ordinating machinery to do the job. If there is a federal budget there must obviously be a legislative and executive apparatus that executes it and is democratically accountable for it. Moreover, the need for federal institutions extends far beyond economic affairs.

[emphasis added]

So it is incorrect to claim that a fiscal union is highly expensive for rich states. If there is a fiscal union, while rich regions will receive less from the supranational fiscal authority than what they pay in taxes, there’ll be higher output and income than otherwise simply because there is a powerful institution which raises output of each region. Rich nations will be able to net export more than otherwise, for example, compensating for transfers in absolute terms.

Analysis such as by Josh Barro are erroneous usually because of implicit assumptions made such as an aggregate production function, which implies a neutral role for fiscal policy. This can easily be verified: his assumption is that output is determined by other factors, not fiscal policy (because he doesn’t say so) and hence the role of a central government is one which just transfers from rich regions to poor, instead of having any impact on the output of the whole region. Silly.