If you believe economists and commentators, you’d get the impression that the US economy is at full employment.

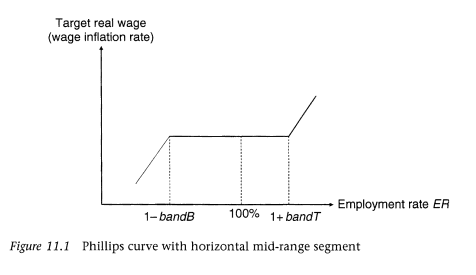

Commentators till recently have been pointing out that the Phillips curve is flat. The curve can be thought in various ways and one way is a plot of wage rate in the y-axis and the employment rate in the x-axis, as in stock-flow coherent models.

One would think it has a positive slope as higher employment would mean better wage bargaining. Or like this as in Figure 11.1, page 387 from Monetary Economics, Ed. 1 written by Wynne Godley and Marc Lavoie.

Economists using the neoclassical paradigm however think of it without any flat segments.

But till recently, many economists had been claiming that the Phillips curve is flat, as in flat not only in a segment but just flat.

This might look welcome but it is a deceit. It’s ironic that economists using the neoclassical paradigm are claiming this as typically they would accuse heterodox of assuming a flat Phillips curve.

The reason it is a deceit is that it induces the reader into thinking that full employment has been achieved and that there’s no need to do anything such as a fiscal expansion.

But recently wages have risen a bit. Now economists and commentators such as Alan Blinder, Paul Krugman, Justin Wolfers and many more have been claiming that the US economy is at full employment.

Full employment?

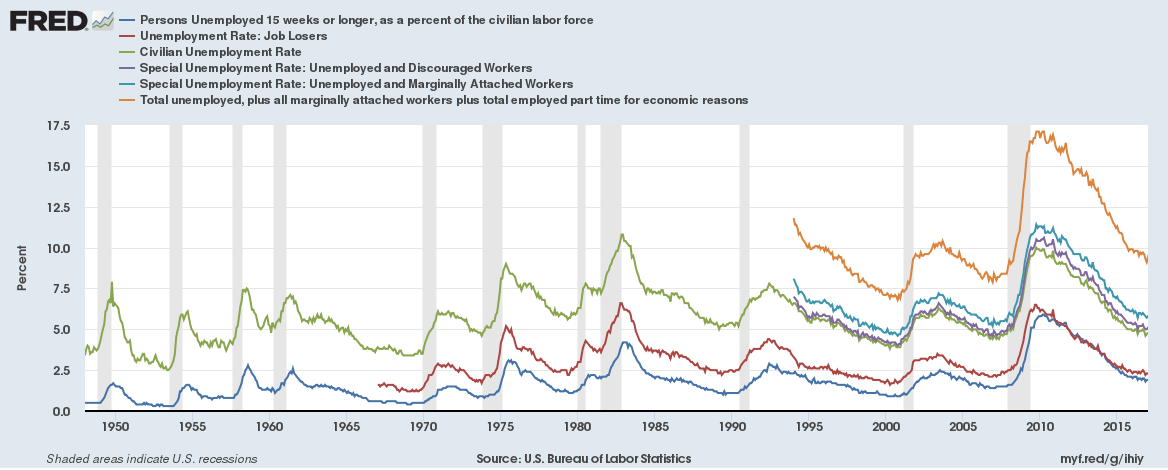

The headline unemployment rate of the United States is 4.1%. That is infinitely far from than 0%. How is that full employment or near full employment?

But not only that, that’s what is called the U-3 unemployment rate. The U-6 unemployment rate is 8.2%.

The differences are explained in this Federal Reserve Economic Data (FRED) blog here.

This is the real picture:

click to expand

So the twin deceits are: shifting positions on the Phillips curve to make it look like the US economy has achieved full employment and now claiming that the US economy is already at full employment. This is to promote the idea that nothing needs to be done.

There is no branch of economics in which there is a wider gap between orthodox doctrine and actual problems than in the theory of international trade.

– Joan Robinson, written in 1970, in The Need For A Reconsideration Of The Theory Of International Trade in Contributions To Modern Economics, published in 1978.

Sometimes, when critiquing free trade, economists and leftists frequently point out to damaging clauses in free trade agreements, such as the ISDS (Investor State Dispute Resolution). While this is fine, and it’s accurate to say that these help powerful corporations and hurt poor nations badly, it’s not a full critique. The important thing to understand is that even without these things which are pushed, free trade (as oppose to free trade agreements) itself is damaging.

Instead of leading to convergence in the fortunes of nations and making everyone better off, free trade creates polarisation. As Kaldor argues in his 1980 article Foundations And Implications Of Free Trade Theory, written in Unemployment In Western Countries – Proceedings Of A Conference Held By The International Economics Association At Bischenberg, France:

Traditional theory, both classical and neoclassical, asserts that free trade in goods between different regions is always to the advantage of each trading country, and is therefore the best arrangement from the point of view of the welfare of the trading world as a whole, as well as of each part of the world taken separately.1 However, these propositions are only true under specific abstract assumptions which do not correspond to reality. Under more realistic assumptions unrestricted trade is likely to lead to a loss of welfare to particular regions or countries and even to the world as a whole – that is to say that the world will be worse off under free trade than it could be under some system of regulated trade.

1 The latter part of this proposition abstracts from the possibility that a particular country possesses some degree of monopoly power and thereby can turn the terms of trade in its favour by means of a tariff even after retaliation by other countries is taken into account.

[emphasis in original, boldening mine]

Somehow economists seem to not understand the case that free trade can be bad to the world as a whole. It’s not difficult to understand why. In the absence of any market mechanism to resolve imbalances in a system of free trade, nations facing balance of payments problems are forced to deflate demand and output. The successful nations don’t expand domestic demand enough because of orthodoxy about fiscal policy.

Some economists understand that free trade leads to winners and losers and argue for compensation for losers. While it’s true that losers need to be compensated, the argument is incorrect because it implicitly assumes that nations’ fortunes aren’t diverging. There are no winning and losing nations in this picture. Perhaps the economist who observes this empirically would blame it on domestic policies and not on rules of international trade or history as colonialism or imperialism. Free trade is the holy cow of economics. It’s a sin to critique it. That’s the economists’ attitude.

In a recent article, What Do Trade Agreements Really Do?, Dani Rodrik repeats various orthodoxies. Despite claiming frequently to be dissenter, it’s clear to see that he is a fan of free trade:

When economists teach the gains from trade, they emphasize that free trade is good for each nation on its own. (What it means to say “good for the nation” in the presence of losers as well as gainers is, if course, a thorny issue, but I will leave that aside, in keeping with the standard treatment.) Ricardo’s (1817) demonstration of the principle of comparative advantage — free trade expands a nation’s consumption possibilities frontier even if it has an absolute productivity advantage in producing every good – remains one of our profession’s most significant intellectual achievements.

[emphasis: mine]

Rodrik then goes on to argue that:

As trade agreements become less about tariffs and non-tariff barriers at the border and more about domestic rules and regulations, economists might do well to worry more about the latter possibility.

This line of thinking emphasises how it’s important to critique not just clauses in free trade agreements such as ISDS, but free trade itself. Else one risks of settling for free trade as a compromise in the best case (as opposed to “freer trade”), something which Dani Rodrik and other orthodox economists want to achieve.

More importantly, although people talk of ideologies such as neoliberalism, it is important to understand them as the ideology of the imperialist and not disconnected to them. The imperialist view of the world (modifying a quote by John Pilger) is that here are only two sides to an argument, and both those sides belong to the establishment.

Rarely does one come across some nice article about changes in the US economy, especially the conditions that enabled the election of Donald Trump. Most articles are, as Glenn Greenwald says, “In the Democratic echo chamber, inconvenient truths are recast as Putin plots”.

These have implications not just for the US but for the world as a whole.

Nancy Fraser, a professor of philosophy and politics at the New School for Social Research has a nice articleFrom Progressive Neoliberalism To Trump—And Beyond for American Affairs.

The trick of neoliberalism is to appear progressive on the social axis of the political spectrum and deceive voters into believing that right-wing economics is good for them.

Fraser says,

The progressive-neoliberal program for a just status order did not aim to abolish social hierarchy but to “diversify” it, …

Glenn Greenwald is one of the best intellectuals in the world today. His Twitter feed is my favourite page on the internet. New York, the magazine has a nice profile on him, titled Does This Man Know More Than Robert Mueller? with emphasis on his stand on stories that the Russian government intervened in the U.S. elections.

You should also read his own opinion on the article in this Twitter thread.

Excerpts:

… In his eyes, the Russia-Trump story is a shiny red herring — one that distracts from the failures, corruption, and malice of the very Establishment so invested in promoting it.

…

“When Trump becomes the starting point and ending point for how we talk about American politics, [we] don’t end up talking about the fundamental ways the American political and economic and cultural system are completely fucked for huge numbers of Americans who voted for Trump for that reason,” he says. “We don’t talk about all the ways the Democratic Party is a complete fucking disaster and a corrupt, sleazy sewer, and not an adequate alternative to this far-right movement that’s taking over American politics.”

…

Rather than see Trump as a product of a rotten power structure, as Greenwald does, and the 2016 election as a wild reaction against that power structure, as Greenwald also does, it was easier for most American liberals to frame his victory as an accident. And rather than look within to eradicate the conditions that wrought Trump, it was more comforting to pin his rise on an external foe.

…

… If you believe the 2016 election was a populist uprising against complacent elites, the Russia preoccupation can seem like an effort to ignore what Trump voters — and Sanders voters — were trying to say. Alternatively, if you believe Trump’s victory was a Russia-perpetrated fraud, normalcy is restored simply by removing him from office

Yesterday, there was a joint conference, Germany – Current Economic Policy Debates, jointly organized by the German Bundesbank and the IMF.

Christine Lagarde wrote an article, Three German Economic Challenges with European Effect at IMFBlog.

In that discusses Germany’s 🇩🇪 current account balance of payments:

Challenge 3: More balanced savings and investments

Another feature of the German economic recovery is the country’s high current account surplus. At nearly 8 percent of GDP, it is also the highest in the world in dollar terms. The high surplus shows that German households and companies still prefer to save rather than invest.

For our part, the IMF has indicated that this surplus is too large—even considering the need to save for retirement in an aging society. Boosting investment in the German economy and reducing the need to save for retirement by encouraging older workers to remain in the labor force can lower the surplus. We need to ask why German households and companies save so much and invest so little, and what policies can resolve this tension.

It’s welcome but still far from any action.

I also have a dislike for this kind of narrative. Usually the phrase saving is used in such discussion because of the identity:

National Saving = National Investment + CAB

where, CAB is the current account balance.

But the saving here is not the same as household saving and/or firms’ saving. Also it needn’t be the case that firms’ investment is low. It’s very well possible that households’ and firms may be saving low and yet the current account balance is high. This is because it depends on other things such as fiscal policy, competitiveness of German firms etc. The same argument is repeated in the other direction when the discussion is about the United States, with the claim that households save too little. But if US households start saving more, the US current account deficit will fall but that will be because of a fall in output and employment.

It’s important to remember that John Maynard Keynes recognized that active policy measures are needed to resolve global imbalances. He proposed to impose penalties on creditor nations in his plan for Bretton-Woods and also require them to take measures such as:

(a) Measures for the expansion of domestic credit and domestic demand. (b) The appreciation of its local currency in terms of bancor, or, alternatively, the encouragement of an increase in money rates of earnings; (c) The reduction of tariffs and other discouragements against imports. (d) International development loans.

– page 24 of The Keynes Plan

Of course Bancor is not the solution but we can still learn from Keynes’ idea for creating policies for balance of payments targets, instead of relying on the market mechanism to resolve imbalances.

Free trade is the most sacred tenet of Economics. So economists go at length to defend it. In doing so, they also ironically seem to talk like “Luddites”, i.e., claiming that automation is the cause of job losses.

Noah Smith has an articleDon’t Blame Robots for President Trump for Bloomberg View. The article is a large concession from orthodoxy. It says:

As Mishel and Bivens point out, estimates by Acemoglu and Restrepo imply that the effect of Chinese competition on U.S. manufacturing-job losses has been three times the effect of robots. So even researchers who are alarmed about robots think that so far, trade has been a much bigger shock to U.S. workers.

It’s easy to see all this is using simple Keynesian economics. In open economy macroeconomics, international trade affects the expenditure multiplier. So output is dependent on exports and imports and the actual output needn’t be the full employment output. Expenditure multiplier depends on both fiscal policy and the private expenditure function and so fiscal policy can be relaxed to achieve a higher output. But this process can be unsustainable.

Except that there may be a market mechanism to resolve imbalances in international trade. By that, what is usually meant is that stock-flow ratios converge and don’t keep rising (or falling if negative) without limits. In fixed exchange rate regimes, there is none. But free trade is not a new idea but an old one and orthodox economists used to argue for mechanisms. The problem with these is that they rely on Monetarism, which is deeply flawed. In floating exchange rate regimes, one could imagine adjustments of the exchange rate in doing the miracle. But it has not been seen in practice. In stock-flow coherent models, one does see adjustment of exchange rates leading to imbalances resolving but this is under simple simple assumptions on expectations of exchange rates. One can’t show this in general.

In reality, instead of convergence of fortunes of nations, what happens is polarisation. The nations who get a head start get more and more competitive and keep winning at the expense of the ones left behind. So we need a solution through actions of all governments.

A closely related claim is that manufacturing employment has reduced because of rise in productivity and not due to international factors. The Bloomberg article concedes that this orthodoxy is not true.

Some Post-Keynesian authors such as Wynne Godley had been stressing the importance of international trade on US employment. In his 1995 essay, A Critical Imbalance In U.S. Trade: The U.S. Balance Of Payments, International Indebtedness And Economic Policy, he said (page 16):

It is sometimes said that manufacturing has lost its importance and that countries in balance of payments difficulties should look to trade in services to put things right. However, while it is still true that manufacturing output has declined substantially as a share of GDP, the figures quoted above show that the share of manufacturing imports has risen substantially. The importance of manufacturing does not reside in the quantity of domestic output and employment it generates, still less in any intrinsic superiority that production of goods has over provision of services; it resides, rather, in the potential that manufactures have for expansion in international trade.

The new issue of ROKE is out and the journal has made available Marc Lavoie and Brett Fiebiger’s article free.

Abstract:

In late 2008 a consensus was reached amongst global policymakers that fiscal stimulus was required to counteract the effects of the Great Recession, a view dubbed as the New Fiscalism. Pragmatism triumphed over the stipulations of the New Consensus Macroeconomics, which viewed discretionary fiscal actions as an irrelevant tool of counter-cyclical macroeconomic policy (if not altogether detrimental). The partial re-embrace of Keynes was however relatively short-lived, lasting only until early 2010 when fiscal consolidation came to the forefront again, although the merits of fiscal austerity were questioned when economic recovery did not really materialize in 2012. This paper traces the ups and downs of the debate over the New Fiscalism, especially at the International Monetary Fund, by analysing IMF documents and G20 communiqués. Using fiscal policy as a means to exit the crisis remains contentious even amidst recognition of secular stagnation.

Referred is also a 2016 article by Janet Yellen who makes a huge concession about the state of Macroeconomics:

The Influence of Demand on Aggregate Supply

The first question I would like to pose concerns the distinction between aggregate supply and aggregate demand: Are there circumstances in which changes in aggregate demand can have an appreciable, persistent effect on aggregate supply?

Prior to the Great Recession, most economists would probably have answered this question with a qualified “no.” They would have broadly agreed with Robert Solow that economic output over the longer term is primarily driven by supply–the amount of output of goods and services the economy is capable of producing, given its labor and capital resources and existing technologies. Aggregate demand, in contrast, was seen as explaining shorter-term fluctuations around the mostly exogenous supply-determined longer-run trend. This conclusion deserves to be reconsidered in light of the failure of the level of economic activity to return to its pre-recession trend in most advanced economies. This post-crisis experience suggests that changes in aggregate demand may have an appreciable, persistent effect on aggregate supply–that is, on potential output.

The idea that persistent shortfalls in aggregate demand could adversely affect the supply side of the economy–an effect commonly referred to as hysteresis–is not new; for example, the possibility was discussed back in the mid-1980s with regard to the performance of European labor markets.

Imagine a firm F1 in the United States 🇺🇸, which sells, say, toys. The firm is solely American, insofar as the employees of this firm and factory location are concerned. But the firm also exports toys and this contributes to the United States’ exports. For simplicity, assume that raw materials aren’t imported from abroad. Let’s say sales is $120 million of which exports are $100 million.

Now, imagine the firm has offshored significant part of its production to, say, Taiwan 🇹🇼. In other words, there’s a firm F2 in Taiwan owned by significantly by F1. This gives a cost advantage to F1 and let’s say the sales are $200 million outside the U.S. and $40 million in the US.

The way the system of national accounts and balance of payments guide, i.e., the 2008 SNA and BPM6 treat these two cases are different.

Exports of the United States is $100 million in the first case but not $200 million in the second.

This is because—and I am simplifying here—the toys are manufactured by F2, which is a resident of Taiwan and the goods sold in the rest of the world (rest in relation to the United States) is between a resident unit of Taiwan and the rest of the world.

In addition, there’s a significant transfer of resources from F1 to F2 and this is captured using the concept of transfer pricing.

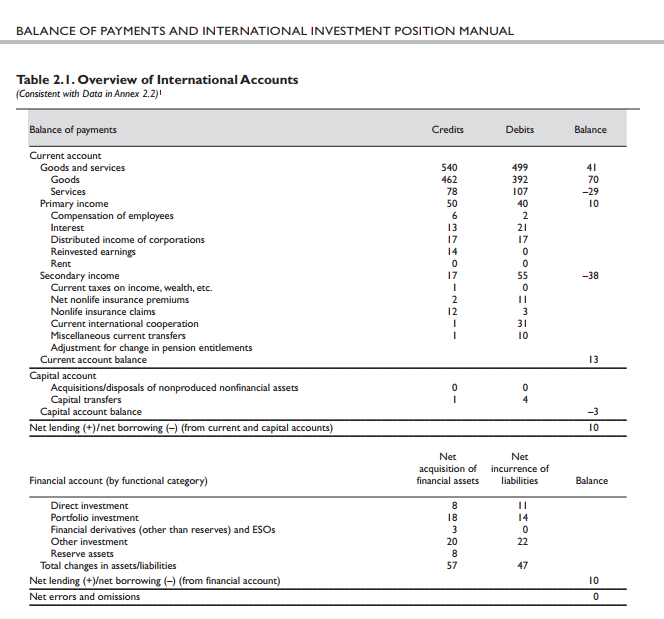

Of course, this doesn’t mean that these sales don’t affect the United States’ balance of payments. Remember how the current, capital and financial accounts look:

source: IMF, BPM6

In the first case, only the goods line in exports is affected in the current account.

In the second case, goods and services (transfer of resources from F1 to F2), distributed income of corporations and retained earnings are all affected.

Goods, because of transfer of some goods from F1 to F2. Also because consumers inside the United States may buy the toys.

Services, because of use of intellectual property of F1 by F2.

Distributed income of corporations and retained earnings because F1 is a direct investor in F2.

So in our example, in the second case, the sale of toys to the the world affects exports, imports and primary income in the balance of payments.

So what was $100 million of exports could be $30 million of exports when production is offshored, whereas $200 million is more intuitive.

In other words, the goods and services balance (or the trade surplus, or the negative of the trade deficit) is changed.

So the change in the U.S. goods and services balance of payments is attributable to three things:

Change in competitiveness of American firms,

Changes in accounting treatment because of offshoring,

Transfer pricing.

The UN 🇺🇳 guide, Guide To Measuring Global Production is a good reference for this.

It explains complications because of transfer pricing:

Transfer pricing

3.40 The Organisation for Economic Co-operation and Development (OECD) (2010) guidance on transfer pricing13 introduced a series of guidelines that may assist MNEs and national tax authorities in using transfer prices to value intra-firm transactions and to evaluate their appropriateness for taxation purposes. The guidelines insist that intra-firm transactions are priced, as far as possible, like arm’s length transactions between unrelated third parties. The guidelines give recommendations on how these intra-firm transactions can be analyzed to determine if they meet these requirements. These recommendations cover comparable measures of profits or comparable measures of costs to be used in assessing transactions between firms.

3.41 In this context recent developments at OECD have resulted in a series of steps to be followed by member countries to limit the impact of Base Erosion and Profit Shifting (BEPS)14. These steps will require transparency, exchange of information between taxation authorities and general cooperation to ensure the arm’s length principle is followed in transactions between entities in an MNE group.

3.42 Nevertheless, distortions in the use of the arm’s length principle are not always tax driven. The 2008 SNA (paragraph 3.133) explains that the exchange of goods between affiliated enterprises may often be one that does not occur between independent parties (for example, specialized components that are usable only when incorporated in a finished product). Similarly, the exchange of services, such as management services and technical know-how, may have no near equivalents in the types of transactions in services that usually take place between independent parties. Thus, for transactions between affiliated parties, the determination of values comparable to market values may be difficult, and compilers may have no choice other than to accept valuations based on explicit costs incurred in production or any other values assigned by the enterprise.

3.43 The 2008 SNA explains that replacing book values based on transfer pricing with market value equivalents is perhaps desirable in principle but is an exercise calling for cautious and informed judgment. One would expect such adjustments to be enforced in the first place by the tax authorities.

13 Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations: www.oecd.org/ctp/transferpricing/transfer-pricing-guidelines.htm

14 http://www.oecd.org/tax/beps.htm

The guide has 175 pages, so it’s very complicated!!

Again, distortions in transfer pricing isn’t the only thing. Even if it is captured properly, the mere act of offshoring changes the goods and services account numbers.

To summarize, there are two important issues here:

Measurement issues for national accountants,

Need for economists to understand the accounting behind all this.

So one could say that U.S. trade balance isn’t as bad as it seems, because a lot is captured in primary income account of balance of payments instead of the goods and services account. It might also partly explain why the U.S. primary income balance is so large. It should however be noted that there’s a cancelling effect in the current account and current account balance which is equally important.

There’s a nice new book titled, Advances In Endogenous Money Analysis, edited by Louis-Philippe Rochon and Sergio Rossi.

There’s a great chapter on Nicholas Kaldor’s views on money over the years by John E. King and another by Marc Lavoie titled, Assessing Some Structuralist Claims Through A Coherent Stock–Flow Framework. John E. King also discusses the importance of fiscal policy in Kaldor’s work:

Kaldor continued to insist on the importance of fiscal policy. The first point in his ‘constructive programme of recovery’ from the world stagflationary crisis of the early 1980s was international agreement on ‘coordinated fiscal action including a set of consistent balance of payments targets and “full employment” budgets’ (Kaldor, 1996, pp. 86, 87). Existing budget deficits, he maintained, were

largely the consequence of the low level of activity. On a ‘full employment’ basis they would show a highly restrictive picture – they would show surpluses and not deficits. Contrary to appearances, the requirement of stability is for expansionary budgets – with lower taxes and higher expenditure, and not further fiscal restriction (as is advocated, for example, by M. de Larosiere of the International Monetary Fund). (Ibid., p. 87)

International coordination was critical to the success of this strategy. Trade liberalization was not consistent with full employment: ‘under conditions of unrestricted free trade the actual volume of production and trade may in fact be considerably less than under some system of regulated trade’ (ibid., italics in the original).