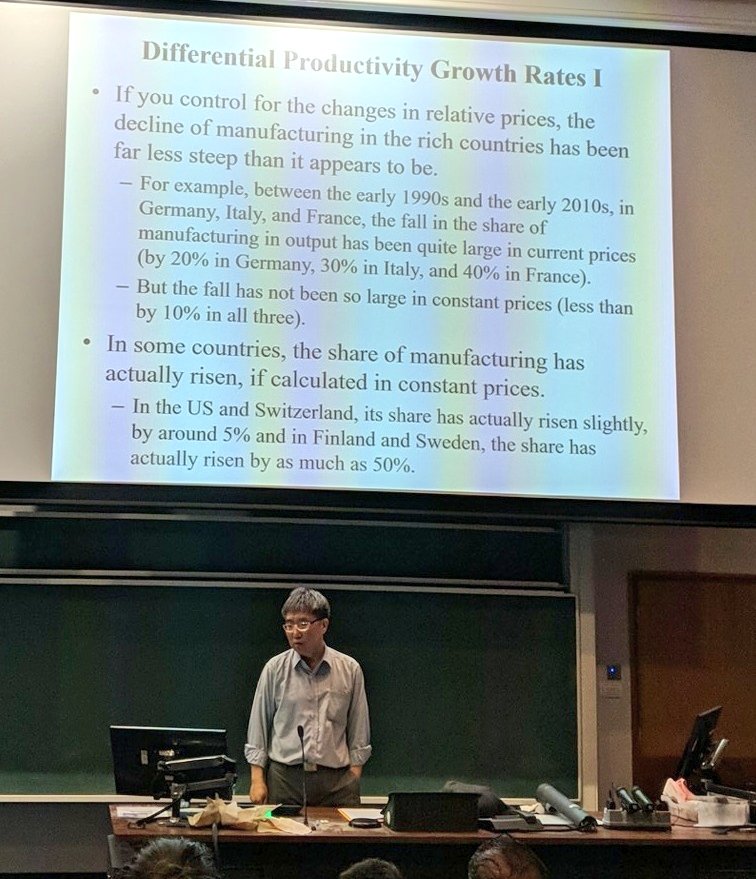

Recently the University Of York hosted a talk by Ha-Joon Chang on deindustrialisation. The title of the talk was: Manufacturing Matters – The Myth Of Post-Industrial Knowledge Economy.

You will find a lot of emphasis on manufacturing in Nicholas Kaldor and Wynne Godley’s work. Why is manufacturing important? Wynne Godley emphasised the supremacy of manufactured products over services in exports, since it’s more difficult to export services. Nicholas Kaldor also suggested increasing returns to scale in manufacturing.

We are frequently told that manufacturing lost its importance. Ha-Joon Chang’s talk is precisely in debunking this myth. As Wynne Godley emphasised, while the share of manufacturing in GDP has fallen, the share of imports has risen a lot. Ha-Joon Chang also points out another important point that superficial reading of data might mislead. So because of offshoring and how the data is recorded by national accounts, it might look like there is no manufacturing happening. For example—and the real thing is more complicated—Apple manufactures phones, computers, etc., in China and it is recorded as an export of services in U.S. balance of payments and hence not as manufacturing in the production account of U.S. national accounts.

You can view the talk on YouTube. It has slides and audio.

The Levy Institute Of Bard College was far ahead of anyone with its prescience on the fate of the U.S. economy (and also the world) before the crisis. So everyone should read them. Michalis Nikiforos and Gennaro Zezza have a new Strategic Analysis report.

Abstract:

The US economy has been expanding continuously for almost nine years, making the current recovery the second longest in postwar history. However, the current recovery is also the slowest recovery of the postwar period.

This Strategic Analysis presents the medium-run prospects, challenges, and contradictions for the US economy using the Levy Institute’s stock-flow consistent macroeconometric model. By comparing a baseline projection for 2018–21 in which no budget or tax changes take place to three additional scenarios, the authors isolate the likely macroeconomic impacts of: (1) the recently passed tax bill; (2) a large-scale public infrastructure plan of the same “fiscal size” as the tax cuts; and (3) the spending increases entailed by the Bipartisan Budget Act and omnibus bill. Finally, Nikiforos and Zezza update their estimates of the likely outcome of a scenario in which there is a sharp drop in the stock market that induces another round of private-sector deleveraging.

Although in the near term the US economy could see an acceleration of its GDP growth rate due to the recently approved increase in federal spending and the new tax law, it is increasingly likely that the recovery will be derailed by a crisis that will originate in the financial sector.

Dani Rodrik has a nice interview to ProMarket, the blog of the Stigler Center at the University of Chicago Booth School of Business. Rodrik’s views are dissenting but within the conventional DC wisdom/New Consensus. For example, he said as recently as last year that free trade is fine as long as losers as compensated, which is far from accurate, as free trade leads to loser regions as well. Still he has better views than neoliberals. In this interview Rodrik is asked about the ant-globalisation backlash:

Q: Much of the anti-globalization backlash of the last two years has been xenophobic, racist, authoritarian in nature. What is it about the nature of globalization that led to this kind of response?

I think a lot of it has to do with the fact that the left has been missing in action. Twenty years ago, when I was fretting that globalization would create a backlash, I would have guessed that the main beneficiary of this might have been the left, because it would capitalize on the economic and social grievances that these divisions create. Indeed, when we think about the populisms of the late 19th century—in the US or for that matter Latin America, with its long history of populism—they were by and large not racist and xenophobic, ethno-nationalist populisms, but left-wing populisms that focused on financial elites, on corporate elites, and pushed for social reform and more regulation of the economy.

Today, here and in Europe, we’re seeing much more of a right-wing ethnonationalist backlash. I think it’s partly that the left has been missing in action and that the center-left and the social democrats have essentially been complicit in many of these changes since the 1990s. New Democrats in the US and New Labour in the UK were at the very forefront of this push for hyperglobalization, so they couldn’t easily disassociate themselves from this complicity. I think Hillary Clinton’s ill-fated campaign showed that very well.

There were other shocks that made it easier. For example, immigration made it easy for right-wing nativists to provide a much more nativist, ethnonationalist frame for economic and social grievances to which I think one might have responded very differently.

This is a fairly accurate description of what has happened. As I have mentioned many times, the absence of a strong political alternative gave enough opportunities for the far right to come to power. It had an appeal—which the left lacked—although no real solution.

Although we see a lot of left-wing activism these days, it is mainly restricted to cultural issues. People still hold right wing economic ideas while sounding faux left wing.

Austerity measures adopted in the wake of the global financial crisis nearly a decade ago have compounded this state of affairs. Such measures have hit the world’s poorest communities the hardest, leading to further polarization and heightening people’s anxieties about what the future might hold. Some political elites have been adamant that there is no alternative, which has proved fertile economic ground for xenophobic rhetoric, inward-looking policies and a beggar-thy-neighbour stance. Others have identified technology or trade as the culprits behind exclusionary hyperglobalization, but this too distracts from an obvious point: without significant, sustainable and coordinated efforts to revive global demand by increasing wages and government spending, the global economy will be condemned to continued sluggish growth, or worse.

The Trade and Development Report 2017 argues that now is the ideal time to crowd in private investment with the help of a concerted fiscal push – a global new deal – to get the growth engines revving again, and at the same time help rebalance economies and societies that, after three decades of hyperglobalization, are seriously out of kilter. However, in today’s world of mobile finance and liberalized economic policies, no country can do this on its own without risking capital flight, a currency collapse and the threat of a deflationary spiral. What is needed, therefore, is a globally coordinated strategy of expansion led by increased public expenditures, with all countries being offered the opportunity of benefiting from a simultaneous boost to their domestic and external markets.

Kaldorians have been stressing how the Euro project is a half-baked idea. Nicholas Kaldor himself predicted in 1971 that the Euro Area without a federal government would be a failure and warned the establishment.

Anthony Thirlwall—the literary executor of Kaldor—also had his great predictions.

In an article, The Euro And Regional Divergence In Europe, in the book, The Eurosceptical Reader 2, in the year 2000 even predicted the rise of dark forces and the alt-right!

Some quotes:

Page 33:

The regional disaffection that will be caused by deteriorating economic circumstances in countries that lack the policy instruments to deal with economic crisis can too easily become the breeding ground for nationalism and fascism, and political resentment, as witnessed in Europe in the 1920s and 1930s. By all means, let there be more coordination of economic policies in Europe and let the countries of Europe strive for greater political cooperation in areas such as defence, human rights and relations with other countries, but not by luring them into an economic straitjacket over which there is no democratic control and from which there is no easy escape. This is a recipe for political turmoil and the fragmentation of Europe that Britain would be wise to steer clear of.

[italics: mine]

Page 28:

… paradoxically, the euro could become a threat to European integration and stability if it exacerbates regional differences within the EU which I believe it is likely to do. Shocks to countries and to regions within countries are rarely symmetric. Without the instruments to cope, asymmetric shocks will exacerbate regional differences, with the prospect of civil strife, political unrest and disaffection with the whole EU project in the affected regions. Regional policies in the EU are a poor substitute for the ability of individual countries to cope with shocks in their own way.

Page 30:

Loss of economic sovereignty

Adoption of the euro means the abandonment of all the traditional weapons of economic policy that in the past have served countries reasonably well. It is hard to imagine how the countries of Europe would have fared in the post-war years without the active use of monetary, fiscal and exchange rate policy. Relinquishing these instruments of policy could spell disaster for individual countries in the future.

Page 32:

Nowhere in the pacts and conditions governing Economic and Monetary Union and the single currency are there any safeguards against deflationary policies and deflationary conditions such as rising unemployment, falling prices or even governments running budget surpluses. The ‘rules of the game’ are asymmetrical, biased against inflation, as indeed they are at the international level whereby the International Monetary Fund penalises countries in balance of payments deficit, but not those in surplus, which therefore imparts deflationary bias in the world economy.

Page 49:

It would be churlish to wish the euro ill, but I fear that it is going to do great damage to the economies of Europe and to the noble objective of greater European harmony and cooperation. Economic and social disparities between the countries and regions of Europe are still vast, and there is nothing in the euro itself which is going to eliminate these disparities. If anything, without an effective regional policy and fiscal transfer mechanisms, they are likely to widen, making the task of political integration – if that is the ultimate aim of the euro – that much more difficult. The United Kingdom government would do well to steer clear of this risky venture for more than the lifetime of even the next Parliament.

PSL Quarterly Review has a new series Recollections Of Eminent Economists and Anthony Thirlwall has the inaugural contribution.

Abstract:

The paper is the first inaugural contribution to the new series of “Recollections of Eminent Economists”. Under this name, the previous series of the journal (then called “Banca Nazionale del Lavoro Quarterly Review”) used to publish autobiographic essays in which renowned economists described their scientific path and reflected on the recent developments of the discipline. In this work, A.P. Thirlwall recalls his personal and academic biography, ranging from employment in the UK to consultancy work in developing countries, and comments on the reception of his main works. Among the latter, special attention is paid to regional and development economics, as well as to the relation between the balance of payments and economic growth. Throughout the discussion, the author emphasizes the Keynesian inspiration of his analyses.

The General Theory of Employment, Interest and Money was published in January, 1936.

Meanwhile, … , Michal Kalecki had found the same solution.

His book, Essays in the Theory of Business Cycles, published in Polish in 1933, clearly states the principle of effective demand in mathematical form. At the same time he was already exploring the implications of the analysis for the problem of a country’s balance of trade, along the same lines that I followed in drawing riders from the General Theory in essays published in 1937.

The version of his theory set out in prose (published in ‘Polska Gospodarcza’ No. 43, X, 1935) could very well be used today as an introduction to the theory of employment.

He opens by attacking the orthodox theory at the most vital point – the view that unemployment could be reduced by cutting money wage rates. And he shows (a point that Keynesians came to much later, and under his influence) that , of monopolistic influences prevent prices from falling when wage costs are lowered, the situation is still worse, because reduced purchasing power causes a fall in sales on consumption goods …

…

Michal Kalecki’s claim to priority of publication is indisputable.

– Joan Robinson, Kalecki And Keynes in Essays In Honour Of Michal Kalecki, 1964.

Jan Toporowski’s intellectual biography, volume 2 of Michał Kalecki is out now.

Ashwani Saith has a fine biography of Ajit Singh for Ajit Singh (1940–2015), The Radical Cambridge Economist: Anti‐Imperialist Advocate Of Third World Industrialization for the latest issue of Development And Change.

The article highlights how his worldview and work was quite close to Nicky Kaldor.

Ajit Singh died on 23 June 2015 and there’s also a fine obituary on him in The Guardian by John Eatwell.

F.M. Scherer had a nice biography in the Palgrave Companion To Cambridge Economics.

Recently Paul Krugman wrote up an article, Globalization: What Did We Miss? for the IMF globalisation conference last fall. The paper is a large concession to the points some economists have been making on international trade and globalisation. Krugman concedes that:

soaring imports did impose a significant shock on some U.S. workers, which may have helped cause the globalization backlash.

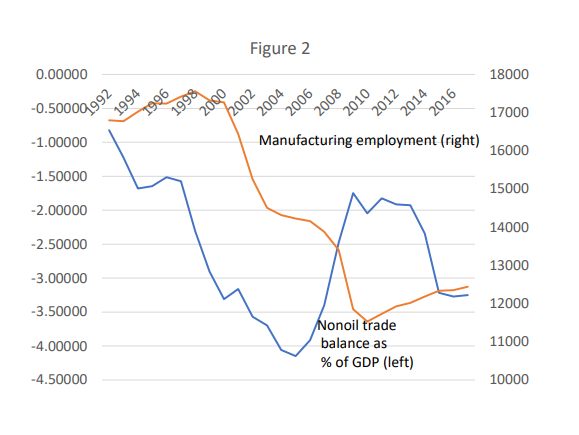

He also draws this chart, coming to the view that the US trade has led to a weakness of manufacturing.

The New Consensus narrative is that loss of employment is due to productivity rises and not due to international trade. Now Krugman has accepted the view that it is the latter.

Further, he also says:

Until the late 1990s employment in manufacturing, although steadily falling as a share of total employment, had remained more or less flat in absolute terms. But manufacturing employment fell off a cliff after 1997, and this decline corresponded to a sharp increase in the nonoil deficit, of around 2.5 percent of GDP.

Does the surge in the trade deficit explain the fall in employment? Yes, to a significant extent. A trade deficit doesn’t produce a one-for-one decline in manufacturing value added, since a significant share of both exports and imports of goods include embodied services. But a reasonable estimate is that the deficit surge reduced the share of manufacturing in GDP by around 1.5 percentage points, or more than 10 percent, which means that it explains more than half of the roughly 20 percent decline in manufacturing employment between 1997 and 2005.

Again, this is over a relatively short time period and focuses on absolute employment, not the employment share. Trade deficits explain only a small part of the long-term shift toward a service economy. But soaring imports did impose a significant shock on some U.S. workers, which may have helped cause the globalization backlash.

And trade deficits are, as I said, part of a broader story of adjustment issues.

Manufacturing is important partly because of increasing returns to scale and partly because it’s easier to export manufactures, although services are catching up.

Further, he quotes the work of Autor, et. al.:

This is where the now-famous analysis of the “China shock” by Autor, Dorn, and Hanson (2013) comes in. What ADH mainly did was to shift focus from broad questions of income distribution to the effects of rapid import growth on local labor markets, showing that these effects were large and persistent. This represented a new and important insight.

To make partial excuses for those of us who failed to consider these issues 25 years ago, at the time we had no way of knowing that either the hyperglobalization shown in Figure 1 or the trade deficit surge shown in Figure 2 were going to happen. And without the combination of these developments the “China shock” would have been much smaller. Still, we missed an important part of the story.

But concessions of previous held orthodox views are hardly straightforward. Despite this large concession, Krugman still wants to defend free trade and is against any tariffs. One may critique selective protectionism but there is also the option of imposing tariffs non-discriminately, i.e., non-selective protectionism.

More importantly, as Joan Robinson often stressed the thesis of free trade ought to also come with the answer to the question: what is the mechanism for resolving imbalances? Free traders always avoid this question, sometimes claiming—as Milton Friedman did—that floating exchange rates does the trick. But we know that it’s hardly the case. In the absence of any market mechanism, we need an official mechanism.

At their blog, in an article titled The Economic Scars of Crises and Recessions, the IMF is now conceding that demand affects supply and that all types of recessions lead to a permanent damage to the supply side. This is known in Post-Keynesian literature as the endogeneity of the natural rate of growth.

Earlier it was thought by them that these are temporary and the economy recovers to its pre-recession trend.

In a 2016 article for the INET, Marc Lavoie had argued how these ideas were new to the mainstream but well known in the heterodox literature.

These are not special to just recessions, as the IMF authors seem to be arguing but is happening continuously, even outside recession. The 2002 paperThe Endogeneity Of The Natural Rate Of Growth by Miguel A. León‐Ledesma and A. P. Thirlwall for the Cambridge Journal Of Economics is a great reference.

If there’s full employment, the rate of growth of GDP is equal to the rate of growth of the labour force plus the rate of growth of productivity. This is Harrod’s natural rate of growth. Unlike the natural rate of interest or of unemployment, this is not vacuous. Of course, below full employment, an economy can grow faster, although the actual rate of growth depends on demand always. We also know that the rate of growth of productivity depends itself on the rate of growth of the GDP. So that implies that the natural rate of growth is endogenous.

From the León‐Ledesma-Thirlwall paper:

The question of whether the natural growth rate is exogenous or endogenous to demand, and whether it is input growth that causes output growth or vice versa, lies at the heart of the debate between neoclassical growth economists on the one hand, who treat the rate of growth of the labour force and labour productivity as exogenous to the actual rate of growth, and economists in the Keynesian/post-Keynesian tradition, who maintain that growth is primarily demand driven because labour force growth and productivity growth respond to demand growth, both foreign and domestic. The latter view does not imply, of course, that demand growth determines supply growth without limit; rather, that aggregate demand determines aggregate supply over a range of full employment growth rates, and that in most countries demand constraints (related to excessive inflation and balance of payments disequilibrium) tend to bite long before supply constraints are ever reached.