The new issue of ROKE is out and the journal has made available Marc Lavoie and Brett Fiebiger’s article free.

Abstract:

In late 2008 a consensus was reached amongst global policymakers that fiscal stimulus was required to counteract the effects of the Great Recession, a view dubbed as the New Fiscalism. Pragmatism triumphed over the stipulations of the New Consensus Macroeconomics, which viewed discretionary fiscal actions as an irrelevant tool of counter-cyclical macroeconomic policy (if not altogether detrimental). The partial re-embrace of Keynes was however relatively short-lived, lasting only until early 2010 when fiscal consolidation came to the forefront again, although the merits of fiscal austerity were questioned when economic recovery did not really materialize in 2012. This paper traces the ups and downs of the debate over the New Fiscalism, especially at the International Monetary Fund, by analysing IMF documents and G20 communiqués. Using fiscal policy as a means to exit the crisis remains contentious even amidst recognition of secular stagnation.

Referred is also a 2016 article by Janet Yellen who makes a huge concession about the state of Macroeconomics:

The Influence of Demand on Aggregate Supply

The first question I would like to pose concerns the distinction between aggregate supply and aggregate demand: Are there circumstances in which changes in aggregate demand can have an appreciable, persistent effect on aggregate supply?

Prior to the Great Recession, most economists would probably have answered this question with a qualified “no.” They would have broadly agreed with Robert Solow that economic output over the longer term is primarily driven by supply–the amount of output of goods and services the economy is capable of producing, given its labor and capital resources and existing technologies. Aggregate demand, in contrast, was seen as explaining shorter-term fluctuations around the mostly exogenous supply-determined longer-run trend. This conclusion deserves to be reconsidered in light of the failure of the level of economic activity to return to its pre-recession trend in most advanced economies. This post-crisis experience suggests that changes in aggregate demand may have an appreciable, persistent effect on aggregate supply–that is, on potential output.

The idea that persistent shortfalls in aggregate demand could adversely affect the supply side of the economy–an effect commonly referred to as hysteresis–is not new; for example, the possibility was discussed back in the mid-1980s with regard to the performance of European labor markets.

Imagine a firm F1 in the United States 🇺🇸, which sells, say, toys. The firm is solely American, insofar as the employees of this firm and factory location are concerned. But the firm also exports toys and this contributes to the United States’ exports. For simplicity, assume that raw materials aren’t imported from abroad. Let’s say sales is $120 million of which exports are $100 million.

Now, imagine the firm has offshored significant part of its production to, say, Taiwan 🇹🇼. In other words, there’s a firm F2 in Taiwan owned by significantly by F1. This gives a cost advantage to F1 and let’s say the sales are $200 million outside the U.S. and $40 million in the US.

The way the system of national accounts and balance of payments guide, i.e., the 2008 SNA and BPM6 treat these two cases are different.

Exports of the United States is $100 million in the first case but not $200 million in the second.

This is because—and I am simplifying here—the toys are manufactured by F2, which is a resident of Taiwan and the goods sold in the rest of the world (rest in relation to the United States) is between a resident unit of Taiwan and the rest of the world.

In addition, there’s a significant transfer of resources from F1 to F2 and this is captured using the concept of transfer pricing.

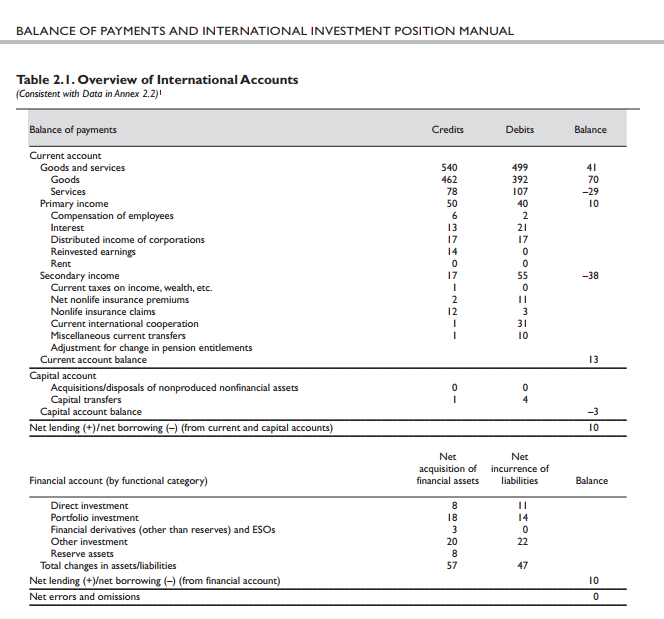

Of course, this doesn’t mean that these sales don’t affect the United States’ balance of payments. Remember how the current, capital and financial accounts look:

source: IMF, BPM6

In the first case, only the goods line in exports is affected in the current account.

In the second case, goods and services (transfer of resources from F1 to F2), distributed income of corporations and retained earnings are all affected.

Goods, because of transfer of some goods from F1 to F2. Also because consumers inside the United States may buy the toys.

Services, because of use of intellectual property of F1 by F2.

Distributed income of corporations and retained earnings because F1 is a direct investor in F2.

So in our example, in the second case, the sale of toys to the the world affects exports, imports and primary income in the balance of payments.

So what was $100 million of exports could be $30 million of exports when production is offshored, whereas $200 million is more intuitive.

In other words, the goods and services balance (or the trade surplus, or the negative of the trade deficit) is changed.

So the change in the U.S. goods and services balance of payments is attributable to three things:

Change in competitiveness of American firms,

Changes in accounting treatment because of offshoring,

Transfer pricing.

The UN 🇺🇳 guide, Guide To Measuring Global Production is a good reference for this.

It explains complications because of transfer pricing:

Transfer pricing

3.40 The Organisation for Economic Co-operation and Development (OECD) (2010) guidance on transfer pricing13 introduced a series of guidelines that may assist MNEs and national tax authorities in using transfer prices to value intra-firm transactions and to evaluate their appropriateness for taxation purposes. The guidelines insist that intra-firm transactions are priced, as far as possible, like arm’s length transactions between unrelated third parties. The guidelines give recommendations on how these intra-firm transactions can be analyzed to determine if they meet these requirements. These recommendations cover comparable measures of profits or comparable measures of costs to be used in assessing transactions between firms.

3.41 In this context recent developments at OECD have resulted in a series of steps to be followed by member countries to limit the impact of Base Erosion and Profit Shifting (BEPS)14. These steps will require transparency, exchange of information between taxation authorities and general cooperation to ensure the arm’s length principle is followed in transactions between entities in an MNE group.

3.42 Nevertheless, distortions in the use of the arm’s length principle are not always tax driven. The 2008 SNA (paragraph 3.133) explains that the exchange of goods between affiliated enterprises may often be one that does not occur between independent parties (for example, specialized components that are usable only when incorporated in a finished product). Similarly, the exchange of services, such as management services and technical know-how, may have no near equivalents in the types of transactions in services that usually take place between independent parties. Thus, for transactions between affiliated parties, the determination of values comparable to market values may be difficult, and compilers may have no choice other than to accept valuations based on explicit costs incurred in production or any other values assigned by the enterprise.

3.43 The 2008 SNA explains that replacing book values based on transfer pricing with market value equivalents is perhaps desirable in principle but is an exercise calling for cautious and informed judgment. One would expect such adjustments to be enforced in the first place by the tax authorities.

13 Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations: www.oecd.org/ctp/transferpricing/transfer-pricing-guidelines.htm

14 http://www.oecd.org/tax/beps.htm

The guide has 175 pages, so it’s very complicated!!

Again, distortions in transfer pricing isn’t the only thing. Even if it is captured properly, the mere act of offshoring changes the goods and services account numbers.

To summarize, there are two important issues here:

Measurement issues for national accountants,

Need for economists to understand the accounting behind all this.

So one could say that U.S. trade balance isn’t as bad as it seems, because a lot is captured in primary income account of balance of payments instead of the goods and services account. It might also partly explain why the U.S. primary income balance is so large. It should however be noted that there’s a cancelling effect in the current account and current account balance which is equally important.

There’s a nice new book titled, Advances In Endogenous Money Analysis, edited by Louis-Philippe Rochon and Sergio Rossi.

There’s a great chapter on Nicholas Kaldor’s views on money over the years by John E. King and another by Marc Lavoie titled, Assessing Some Structuralist Claims Through A Coherent Stock–Flow Framework. John E. King also discusses the importance of fiscal policy in Kaldor’s work:

Kaldor continued to insist on the importance of fiscal policy. The first point in his ‘constructive programme of recovery’ from the world stagflationary crisis of the early 1980s was international agreement on ‘coordinated fiscal action including a set of consistent balance of payments targets and “full employment” budgets’ (Kaldor, 1996, pp. 86, 87). Existing budget deficits, he maintained, were

largely the consequence of the low level of activity. On a ‘full employment’ basis they would show a highly restrictive picture – they would show surpluses and not deficits. Contrary to appearances, the requirement of stability is for expansionary budgets – with lower taxes and higher expenditure, and not further fiscal restriction (as is advocated, for example, by M. de Larosiere of the International Monetary Fund). (Ibid., p. 87)

International coordination was critical to the success of this strategy. Trade liberalization was not consistent with full employment: ‘under conditions of unrestricted free trade the actual volume of production and trade may in fact be considerably less than under some system of regulated trade’ (ibid., italics in the original).

Yesterday, the Indian government announced a $32 billion plan to recapitalise some banks. These banks have large government ownership. Such issues remain controversial because the government is seen as allowing a lot of bank debtors get away with defaulting on their loans. At any rate, the topic for this post is whether the government plan leads to a rise in deficit or not.

The Chief Economic Advisor clarified on Twitter than according to international standards, it doesn’t lead to a rise in fiscal deficits over the periods during which recapitalisation happens. But people don’t seem to be convinced. So here’s an attempt.

In short, a recapitalisation of banks by the government by an amount of say $100 doesn’t lead to an increase of $100 in deficit. There are some complications, as highlighted below.

It shouldn’t matter but those arguing whether it leads to a rise in deficits are motivated to do so since acceptance by the government will lead to a fall in government expenditures since they are—incorrectly—committed to “fiscal responsibility”.

In the system of national accounts—the latest update of which is the 2008 SNA—there are three main types accounts in the transactions flow account:

Current accounts

Capital account

Financial account

The current accounts record things such as production, generation and distribution of income and so on.

The capital account records transactions in non-financial assets. Para 10.1 of the 2008 SNA describes it:

The capital account is the first of four accounts dealing with changes in the values of assets held by institutional units. It records transactions in non-financial assets. The financial account records transactions in financial assets and liabilities. The other changes in the volume of assets account records changes in the value of both non-financial and financial assets that result from neither transactions nor price changes. The effects of price changes are recorded in the revaluation account. These four accounts enable the change in the net worth of an institutional unit or sector between the beginning and end of the accounting period to be decomposed into its constituent elements by recording all changes in the prices and volumes of assets, whether resulting from transactions or not. The impact of all four accounts is brought together in the balance sheets. The immediately following chapters describe the other accounts just mentioned.

[emphasis: mine]

The financial account is described in para 11.1:

The financial account is the final account in the full sequence of accounts that records transactions between institutional units. Net saving is the balancing item of the use of income accounts, and net saving plus net capital transfers receivable or payable can be used to accumulate non-financial assets. If they are not exhausted in this way, the resulting surplus is called net lending. Alternatively, if net saving and capital transfers are not sufficient to cover the net accumulation of non-financial assets, the resulting deficit is called net borrowing. This surplus or deficit, net lending or net borrowing, is the balancing item that is carried forward from the capital account into the financial account. The financial account does not have a balancing item that is carried forward to another account, as has been the case with all the accounts discussed in previous chapters. It simply explains how net lending or net borrowing is effected by means of changes in holdings of financial assets and liabilities. The sum of these changes is conceptually equal in magnitude, but on the opposite side of the account, to the balancing item of the capital account.

[emphasis: mine]

A recapitalisation of banks is an exchange for equities issued by the bank for funds. The government might raise funds via auctions. The Indian government is even planning to issue something called “recapitalisation bonds” which will be a direct exchange of those bonds with banks for equity. At any rate, these transactions for the government are likely to change the financial account and won’t enter the current accounts and the capital account. So these don’t change the deficit, with the exception below.

It could be the case that the purchase of equity by the government could be not at the market value. So there’s something called capital transfers.

There was a good publication by the BEA which appeared in the Survey of Current Business, February 2009.

click for the pdf file

So the note says:

… consistent with the recommendations in the newly updated international guidelines, System of National Accounts 2008 (SNA), in the fourth quarter of 2008, BEA recorded a portion of the purchase of preferred stock through the TARP as capital transfers; this portion was calculated as the difference between the actual prices paid for the financial assets and an estimate of their market value. These capital transfers recognize that the federal government paid over market value for these financial assets. Net government saving was not affected by the capital transfers, but net government lending or borrowing was reduced as shown in NIPA tables 3.1 and 3.2.

So the full amount of the recapitalisation doesn’t affect the deficit.

In other words, government recapitalisation of banks for an amount $100 doesn’t increase the deficit by $100, but only by the amount mentioned above.

There’s a technicality. If a bank is fully government owned, then it’s the case that the full amount of recapitalisation is the capital transfer. Else it is not.

Also, once a bank is recapitalised, the government pays interest on the bonds and also receives dividends from the ownership. These affect the deficit, and the numbers are also different to the case when a bank isn’t recapitalised or recapitalised by the markets. But for the current purpose, it’s not that important.

It should be simple to understand. If you borrow to buy financial securities for $100, it doesn’t change your deficit or net borrowing (except for brokerage fees and transaction taxes). Your net lending is the difference between your disposable income and expenditure on goods and services. You have borrowed to buy some financial securities but you are also a lender.

Anyway, this simple point was missed even by the US Treasury!

I recently came across a phrase, social silence, which Gillian Tett of FTdescribes:

As Pierre Bourdieu, the French anthropologist and intellectual, observed in his seminal work Outline of a theory of practice, the way that an elite typically stays in power in almost any society is not simply by controlling the means of production (i.e. wealth), but by shaping the discourse (or the cognitive map that a society uses to describe the world around it.) And what matters most in relation to that map is not just what is discussed in public, but what is not discussed because those topics are considered boring, irrelevant, taboo or just unthinkable. Or as Bourdieu wrote: “The most successful ideological effects are those which have no need of words, but ask no more than a complicitous silence.”

Very few talk of the world order and how it operates. The current world order can be described as a neoliberal. It is a system of free trade (or more generally globalization), tight fiscal policy, deregulation and privatization.

The IMF is one institutional which has been responsible for maintaining this world order. Since governments need exceptional financing, they are arm-twisted by the IMF.

A recent United Nations General Assemby note, Promotion Of A Democratic And Equitable International Order, has recognized this and criticizes the IMF strongly. Many economists and pundits deny there’s something called neoliberalism but the note is open about the ideology and the word.

In fact, IMF advocacy of structural adjustment has privileged powerful corporate interests and created a vicious cycle of dependence for borrower countries. As noted by Peter Dolack:

Ideology plays a critical role here. International lending organizations … consistently impose austerity. The IMF’s loans, earmarked … to pay debts or stabilize currencies, always come with the same requirements to privatize public assets (which can be sold far below market value to multi-national corporations waiting to pounce); cut social safety nets; drastically reduce the scope of government services; eliminate regulations; and open economies wide to multi-national capital, even if that means the destruction of local industry and agriculture. This results in more debt, which then gives multi-national corporations and the IMF, which enforces those corporate interests, still more leverage to impose more control, including heightened ability to weaken environmental and labour laws.

and also:

IMF still appears more committed to the obsolete neoliberal economic model.

The report is 18 pages long and critical of the IMF from the start to the end. Please read. You won’t find any discussion of the report in the mainstream media.

In August, Gennaro Zezza and his co-authors Michalis Nikiforos and Marshall Steinbaum had a paper for the Roosevelt Institute, studying the effects of a Universal Basic Income. The model uses the Levy Institute‘s model.

The idea is simple. If a basic income is provided for everyone, it raises domestic demand because of higher consumption and hence leads to higher output. This is easy to see if there’s no rise in tax rates. If tax rates are increased so that the income provided matches the taxes raised, it’s still a stimulus to the economy, since the propensity to consume for people with lower incomes (or no income otherwise) is higher.

From the introduction;

We examine three versions of unconditional cash transfers: $1,000 a month to all adults, $500 a month to all adults, and a $250 a month child allowance. For each of the three versions, we model the macroeconomic effects of these transfers using two different financing plans – increasing the federal debt, or fully funding the increased spending with increased taxes on households – and compare the effects to the Levy model’s baseline growth rate forecast. Our findings include the following:

For all three designs, enacting a UBI and paying for it by increasing the federal debt would grow the economy. Under the smallest spending scenario, $250 per month for each child, GDP is 0.79% larger than under the baseline forecast after eight years. According to the Levy Model, the largest cash program – $1,000 for all adults annually – expands the economy by 12.56% over the baseline after eight years. After eight years of enactment, the stimulative effects of the program dissipate and GDP growth returns to the baseline forecast, but the level of output remains permanently higher.

When paying for the policy by increasing taxes on households, the Levy model forecasts no effect on the economy. In effect, it gives to households with one hand what it is takes away with the other.

However, when the model is adapted to include distributional effects, the economy grows, even in the tax-financed scenarios. This occurs because the distributional model incorporates the idea that an extra dollar in the hands of lower income households leads to higher spending. In other words, the households that pay more in taxes than they receive in cash assistance have a low propensity to consume, and those that receive more in assistance than they pay in taxes have a high propensity to consume. Thus, even when the policy is tax- rather than debt-financed, there is an increase in output, employment, prices, and wages.

The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2017 was awarded to Richard H. Thaler “for his contributions to behavioural economics”.

In his book, Post-Keynesian Economics: New Foundations, (2014), Marc Lavoie has a nice discussion/critique on what’s called “New Behavioural Economics”:

There was a conference last year in honour of Nicholas Kaldor organized by Corvinus University of Budapest.

The papers by the speakers has now been published by Acta Oeconomica in their 2017 s1 issue.

Anthony Thirlwall’s paper Nicholas Kaldor’s Life And Insights Into The Applied Economics Of Growth (Or Why I Became A Kaldorian) is notable. You can access it here if you can’t access the journal.

The second paper which struck an intellectual chord was Kaldor’s address to the Scottish Economic Society in 1970 entitled ‘The Case for Regional Policies’ (Kaldor, 1970). Here, at the regional level, he switches focus from the structure of production in a closed economy to the role of exports in an open regional context in which the growth of exports is considered the major component of autonomous demand (to which other components of demand adapt) which sets up a virtuous circle of growth working through the Verdoorn effect – similar in character to Gunnar Myrdal’s theory of circular and cumulative causation in which success breeds success and failure breeds failure (Myrdal, 1957). This is one of his challenges to equilibrium theory that free trade and the free mobility of factors of production will necessarily equalise economic performance across regions or countries.

Wynne Godley’s Seven Unsustainable Processes (1999) examined the medium-term prospects for the US economy. It shows that in the United States, growth in that period was associated with seven unsustainable processes related to fiscal policy, foreign trade and payments, and private saving, spending, and borrowing. Given unchanged US fiscal policy and growth in the rest of the world, in order to maintain growth, the excessive indebtedness implied by these processes would be so large as to create major problems for the US economy and the world economy in the future. Godley was right. This web application aims to replicate Godley’s analysis for all of the countries in the EU, to see whether or not these unsustainable processes can be seen. It goes beyond Godley in forecasting each important ratio. The accompanying paper gives full details of the ratios and their construction.

The United Nations 🇺🇳 Conference On Trade And Development (UNCTAD) publishes wonderful annual reports on trade and development. These are written by heterodox authors many times. Alex Izurieta, Francis Cripps, Jayati Ghosh are a few contributors. This year’s report is here. 200 pages!

The report has detailed discussion on robots and its impact. This is quite different from what one hears normally.

From the press release:

With the United States withdrawing from its role as global consumer of last resort, recycling surpluses is a key element in rebalancing the global economy. The report turns the spotlight on the eurozone – especially Germany – which is now running a large surplus with the rest of the world. The recent Group of 20 proposal made by Germany – a Marshall Plan for Africa – is welcome, but so far lacks the requisite financial muscle. The trillion-dollar Belt and Road Initiative of China is much bolder, even as its surplus has dropped sharply over the last two years.

The report draws lessons from 1947, when the International Monetary Fund, the World Bank, the General Agreement on Tariffs and Trade and the United Nations joined forces to rebalance the post-war global economy, and the Marshall Plan was launched. Seven decades later, an equally ambitious effort is needed to tackle the inequities of hyperglobalization to build inclusive and sustainable economies.

In response to the political slogan of yesteryear – “there is no alternative” – the report outlines a global new deal to build more inclusive and caring economies. This would combine economic recovery with regulatory reforms and redistribution policies, and do so with speed and at the requisite scale. The successes of the New Deal of the 1930s in the United States owed much to its emphasis on counterbalancing powers and giving a voice to weaker groups in society, including consumer groups, workers’ organizations, farmers and the dispossessed poor. This is no less true today.

In today’s integrated global economy, Governments will need to act together for any one country to achieve success. UNCTAD urges them to seize the opportunity offered by the Sustainable Development Goals and put in place a global new deal for the twenty-first century.

In addition, you can see the two short videos here.