A few days back I posted a link to a paper written by a top advisor the US government admitting that economists in general got fiscal policy quite wrong before the crisis.

Now another admission, but this time from a non-orthodox economist.

In a recent blog post, Bill Mitchell writes (on reforming the international institutional framework):

…

2. Macroeconomic stabilisation – support for national currencies in the face of problematic balance of payments.

This function recognises that all nations should maintain sovereign currencies and float them on international markets but at the same time recognising that capital flows may be problematic at certain times and that some nations require more or less permanent assistance due to their export capacities and domestic resource bases.

The trouble with Neochartalism (Mitchell and his colleagues’ theory, also called “modern monetary theory” by themselves) is that what is correct is not original and what is original is incorrect. Despite repeated arguments of other non-orthodox economists, Neochartalists have continued to deny the existence of the balance-of-payments constraint. Still a long way to go from understanding the supreme importance of balance of payments on growth, but this is a good positive step.

It’s ironic that Neochartalists are followers of Hyman Minsky who talked of financial crises. While Neochartalists emphasize that crises can happen in financial markets, they have till now completely denied that it can happen in foreign exchange markets.

Neochartalists emphasize fiscal policy, as if problems start and end there. But the problems of this world can be solved not just by fiscal policy but also by industrial policy and in the international sphere via diplomacy.

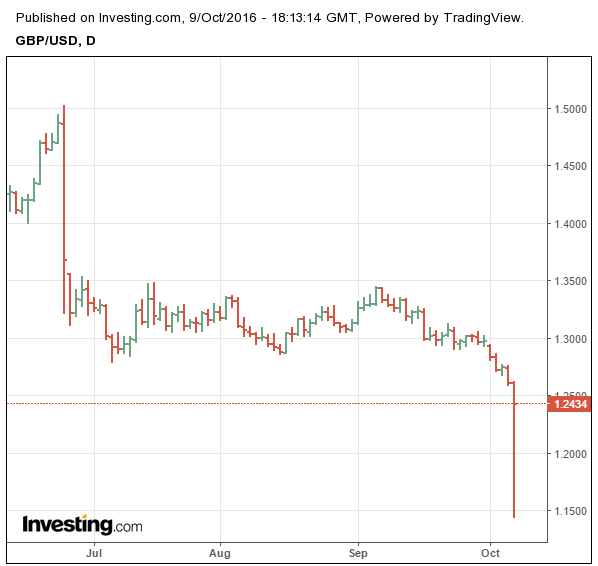

The European Union is founded on the principles of free trade. Dean Baker has a nice blog post on his blog Beat The Press titled, The Value Of The Pound Is Not A Measure Of The Success Or Failure Of Brexit. In that, he comments on Friday’s fall in the exchange rate of the Sterling.

The fall has been claimed to be a failure of the UK 🇬🇧 exiting from the European Union. Dean Baker, although seems to side with the remain-in-the-EU camp, points out:

The Brexit vote was a case where the elites were clearly aligned against the UK leaving the European Union. While they had many good arguments on their side, and much of what the pro-Brexit crew was saying was nonsense, some of the elite gloating now also falls into the nonsense category.

The reason I say this is that he seems to think that there is no economic argument for leaving, while in my opinion, it is quite the opposite. Anyway, I really liked him saying that the elites were aligned against the non-elites. Unfortunately the UK far-right jumped on to this – arguing for exiting the European Union, and it made it easy for the neolibs to thrash arguments for leaving the European Union.

Anyway, the reason for the post is that there’s a frequent claim made around the UK’s current account deficit and the exchange rate in contrast to Baker who says:

Rather than being a negative for the economy, this is a positive development. It is the only plausible mechanism through which the UK can get closer to balanced trade.

Somewhat funnily, the neolibs whose arguments are about the magic of the “market mechanism” are making arguments similar to heterodox economists’ elasticity pessimism. According to the elasticity pessimism view income effects far outweigh the price effects and the market mechanism does not resolve imbalances in balance of payments. The elasticity pessimism view doesn’t claim that price effects do not matter at all.

But funnily, the anti-Brexit people seem to use this view since it suits their political purposes and what’s interesting is that even taking the view that price effects aren’t there! So they are claiming that the exchange rate movement can’t improve the UK balance of payments. Now an analysis of how much exchange rate movements have affected the UK’s exports and imports is difficult but instead of taking an empirical approach, let me make some theoretical arguments.

The claim is that wide movement of exchange rates hasn’t improved the UK current account balance. But that doesn’t mean it doesn’t matter. It just means that the income effects have far outweighed price effects. The depreciation of the Sterling should help the UK. To illustrate my point imagine this (numbers are just for illustration, aren’t actual):

Scenario: The UK current account deficit rises from 7% of GDP in 2016 to 8% of GDP in 2017.

This 1% rise might be explained by:

1.3% due to income effects: i.e. change in GNI at home and abroad, changes in non-price competitiveness.

minus 0.3% due to price effects i.e., changes in the exchange rate and changes in price competitiveness.

So just superficially looking at empirical data might lead us to conclude that the fall in the exchange rate of the Sterling has had no improvement, but that’s not the case. The fall has helped but income effects have outweighed. If the exchange rate hadn’t changed, the current account deficit would have risen to 8.3% of GDP.

But if the UK current account balance of payments doesn’t improve, what is the point of all this you may ask. Well, for one a depreciated exchange rate helps at the margin but the more important effects—which depend on trade negotiations—tariffs etc, would depend on how the UK government manages to help its domestic industry and improve its non-price competitiveness. Leaving the EU would also mean that the UK regulates migration and this would help improve wages, employment and output.

It’s an extreme view that price effects do not matter. China, for example has a highly undervalued exchange rate obtained by official management by PBOC, China’s central bank. Elasticity pessimists do not think that price effects do not matter, only that income effects matter more typically and that the market mechanism does not resolve imbalances. Elasticity pessimism is not an extreme view but it is ironic to see the neolibs who have argue in favour of a common market to take an extremized version of the elasticity pessimism view.

There is even more irony in this. Not joining the European Union was a respectable view in the 70s when Nicholas Kaldor used to argue against joining the EU. But in recent times, it has been hijacked by the nationalists making it easier for neoliberals to claim victory. They just have to argue how the nationalists are wrong (which is true) but it doesn’t mean that the neoliberal project is correct.

Lastly, does it not matter if a currency has a run. Of course it does matter. Just that the Sterling’s fall can’t be called that and the UK is not really in danger because of the fall in the exchange rate. There are no expectations building around the Sterling like what happens to third-world nations’ currencies many times.

Wikileaks has released “The Podesta Emails” which show Hillary Rodham Clinton’s political positions best explained by an NYT article:

[Clinton] embraced unfettered international trade and praised a budget-balancing plan that would have required cuts to Social Security, according to documents posted online Friday by WikiLeaks.

The tone and language of the excerpts clash with the fiery liberal approach she used later in her bitter primary battle with Senator Bernie Sanders of Vermont and could have undermined her candidacy had it become public.

Neoliberalism, the “New Consensus” and pre-Keynesian economics stand exactly for this idea: free trade and balanced-budgets. John Maynard Keynes’ true followers starting with Joan Robinson stood exactly in dissent against the idea of free trade and balanced budgets. Keynes himself understood the trouble with free trade, as can be seen by reading his chapter on Mercantilism in the General Theory, but didn’t emphasize it enough. Unlike what others see, Joan Robinson stood for her opposition to free trade more than anything else.

According to the New Consensus of economics, fiscal policy is impotent and hence budget should be balanced. Free trade will lead to convergence of fortunes of nations according to this view. Instead what we see is polarization. In my previous post, I quoted a top advisor who conceded how economists had been wrong about fiscal policy. But the damage seems to have done. Progressive and Keynesian ideas have a long battle ahead.

Needless to say Donald Trump is not the alternative. So there’s a lot of fight ahead for economists in years ahead to overthrow the new consensus. Macroeconomics makes a difference in people’s life, and it’s a battle worth fighting.

There’s a paper by Jason Furman who is the Chairman of the Council of Economic Advisers which concedes how wrong economists were on fiscal policy. The link is a file hosted at the White House’s website! The paper starts off with a remarkable admission on fiscal policy (h/t and words borrowed from Jo Michell)

A decade ago, the prevalent view about fiscal policy among academic economists could be summarized in four admittedly stylized principles:

Discretionary fiscal policy is dominated by monetary policy as a stabilization tool because of lags in the application, impact, and removal of discretionary fiscal stimulus.

Even if policymakers get the timing right, discretionary fiscal stimulus would be somewhere between completely ineffective (the Ricardian view) or somewhat ineffective with bad side effects (higher interest rates and crowding-out of private investment).

Moreover, fiscal stabilization needs to be undertaken with trepidation, if at all, because the biggest fiscal policy priority should be the long-run fiscal balance.

Policymakers foolish enough to ignore (1) through (3) should at least make sure that any fiscal stimulus is very short-run, including pulling demand forward, to support the economy before monetary policy stimulus fully kicks in while minimizing harmful side effects and long-run fiscal harm.

Today, the tide of expert opinion is shifting the other way from this “Old View,” to almost the opposite view on all four points. This shift is partly the result of the prolonged aftermath of the global financial crisis and the increased realization that equilibrium interest rates have been declining for decades. It is also partly due to a better understanding of economic policy from the experience of the last eight years, including new empirical research on the impact of fiscal policy as well as observations of the reaction of sovereign debt markets to the large increases in debt as a share of GDP in the wake of the global financial crisis. In the first part of my remarks, I will discuss the theory and evidence underlying this “New View” of fiscal policy (with, admittedly, the core of this theory being an “Old Old View” that dates back to John Maynard Keynes and the liquidity trap).

Compare that to the Post-Keynesian view, which according to Wynne Godley and Marc Lavoie in their book Monetary Economics written before the crisis (from chapter 1, Introduction):

The alternative paradigm, which has come to be called ‘post-Keynesian’ or ‘structuralist’, derives originally from those economists who were more or less closely associated personally with Keynes such as Joan Robinson, Richard Kahn, Nicholas Kaldor, and James Meade, as well as Michal Kalecki who derived most of his ideas independently.

… According to post-Keynesian ideas, there is no natural tendency for economies to generate full employment, and for this and other reasons growth and stability require the active participation of governments in the form of fiscal, monetary and incomes policy.

Lars Syll has a nice post quoting James Tobin’s views on the real business cycle theory (and dynamic stochastic general equilibrium (DSGE) models. DSGE models are just RBC theory models with some modifications but still retaining the core).

There’s also another paper, An Old Keynesian Counterattacks by James Tobin written in 1992 and devoted heavily on attacking all this.

Tobin says:

The crucial issue of macroeconomic theory today is the same as it was sixty years ago when John Maynard Keynes revolted against what he called the “classical” orthodoxy of his day. It is a shame that there are still “schools” of economic doctrine, but perhaps controversies are inevitable when the issues involve policy, politics, and ideology and elude decisive controlled experiments. As a lifelong Keynesian, I am quite dismayed by the prevalence in my profession today, in a particularly virulent form, of the macroeconomic doctrines against which I as a student enlisted in the Keynesian revolution. Their high priests call themselves New Classicals and refer to their explanation of fluctuations in economic activity as Real Business Cycle Theory. I guess “Real” is intended to mean “not monetary” rather than “not false,” but maybe both.

I am going to discuss the issues of theory, Keynesian versus Classical, both then and now. Since the main purpose and preoccupation of macroeconomic theory is to guide fiscal and monetary policies, the theoretical differences imply important differences in policy. Moreover, prevailing doctrines seep gradually into the ways the world is viewed not only by economists but also by students, pundits, politicians, and the general public. It is in this sense but only in this sense that I shall be talking about current events.

The doctrinal differences stand out most clearly in opposing diagnoses of the fluctuations in output and employment to which democratic capitalist societies like our own are subject, and in what remedies, if any, are prescribed. Keynesian theory regards recessions as lapses from full-employment equilibrium, massive economy-wide market failures resulting from shortages of aggregate demand for goods and services and for the labor to produce them. Modern “real business cycle theory” interprets fluctuations a moving equilibrium, individually and socially rational responses to unavoidable exogenous shocks. The Keynesian logic leads its adherents to advocate active fiscal and monetary policies to restore and maintain full employment. From real business cycle models, and other theories in the New Classical spirit, the logical implication is that no policy interventions are necessary or desirable.

Should we describe the macro-economy by two regimes or one? The old Keynesian view favors two regimes. In one, the Keynesian regime, aggregate economic activity is constrained by demand but not by supply. If there were additional effective demands for goods and services, they could be and would be satisfied. “Demand creates its own supply.” The necessary inputs of labor, capital capacity, and other factors are available, ready to be employed at prices, wages, and rents that their productivity would earn. Only customers are missing.

The second regime, which Keynes called classical, is supply-constrained. Extra demand could not be satisfied at the economy’s existing capacity to produce. The needed workers or other inputs are not available at affordable wages and rents. The supply limits bring about prices and incomes that restrict aggregate demand to capacity output. Should capacity increase, those prices and incomes will automatically generate just enough additional purchasing power to buy the extra output. “Supply creates its own demand.”

Keynesians believe that the economy is sometimes in one regime, sometimes in the other. New Classicals model the economy as always supply-constrained and in supply-equals-demand equilibrium. In their real business cycle models, the shocks that move economic activity up and down are essentially supply shocks, changes in technology and productivity or in the bounty of nature or in the costs and supplies of imported products. Although external forces of those kinds, for example weather, harvests, natural catastrophes, have been the main sources of fluctuating fortunes for most of human history, and although events continually remind us that they still occur, Keynesians do not agree that they are the main source of fluctuations in business activity in modern capitalist societies.

and in the end concludes by asking:

Why do so many talented economic theorists believe and teach elegant fantasies so obviously refutable by plainly evident facts? Trying to answer that question would take us into a speculative excursion on the sociology of the economics profession, beyond the scope of this paper.

Marc Lavoie has an excellent new article at the Institute For New Economic Thinking website titled Rethinking Macroeconomic Theory Before The Next Crisis.

Excerpt:

In this article, I have tried to stress that there is considerable dissatisfaction with the current state of mainstream macroeconomics and with the quasi-dictatorial directive that the only game to be played in town is the adoption of the DSGE model.

…

Some orthodox economists believe that mainstream economics holds under normal conditions (Richard Koo’s yang phase), but that it needs to be modified under zero-lower bound conditions or during balance sheet recessions (Koo’s yin phase). Macroeconomic theory needs to be revised both for the yang and the yin phases. Providing new clothes to the Naked Emperor of mainstream economics won’t do; the Emperor needs to be dethroned.

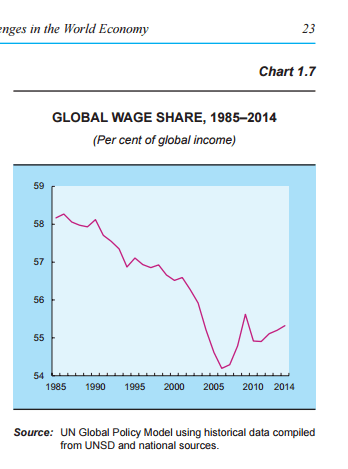

The United Nations Conference On Trade and Development’s annual report for 2016 is out and it’s worth reading as always. It’s generally written by non-orthodox authors.

There’s reference to Myrdal and Kaldor’s work on circular and cumulative causation: specifically the importance of manufacturing. See page 58 onward (page 92 of the pdf file).

Another thing which caught my attention is the share of wages in the national income.

I have been looking at Noam Chomsky’s views on neoliberalism and I found a documentaryNeo-Liberalism Ensnares Democracy by Richard Brouillette which I thought I should mention.

Noam Chomsky in ‘Neo-Liberalism Ensnares Democracy’ Picture from the documentary’s site.

Chomsky argues how neoliberalism is not really “neo” and that it is what created the third world. He goes on to argue how this happens: In his language, free capital flows creates a virtual parliament of investors and lenders who carry out moment by moment referendum on government policies. Governments hence face a dual constituency and that neoliberalism is power-play.

The documentary length is 160 minutes (2h 40m). Chomsky appears at 23:06, 57:20, 1:10:22, 1:46:38, and 2:33:18.

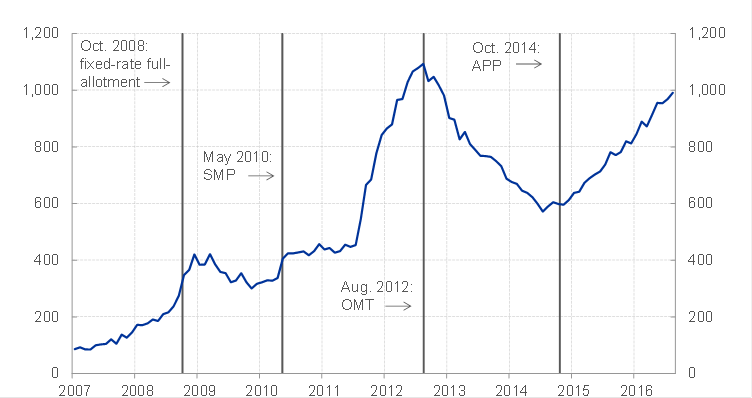

During the crisis which started in 2007 and especially around mid-2011, TARGET2 liabilities of some National Central Banks (NCBs) of the Eurosystem increased drastically (chart below) and led to heated discussion among economists and became a political subject.

Recently, the (im)balance has been increasing again but it seems that it’s mostly because of what some call QE recycling.

Peter Praet, Member of the Executive Board of the ECB explained this in his speech yesterday.

First the chart from his talk:

Sum of all positive TARGET2 balances. Source: ECB.

As Praet shows using T-accounts, what happens if Banco de España purchases securities from a German counterparty, Bundesbank’s TARGET2 assets—claims on the rest of the Eurosystem—will rise and so will Banco de España’s TARGET2 liabilities to the rest of the Eurosystem.

Once the German counterparty sells the securities to Banco de España, it will try to find the nearest substitute which may not be a Spanish security. So this is nothing to be worried about unlike earlier where TARGET2 balances were symptomatic of capital flight from some countries threatening financial meltdown.

Of course one has to be careful. Not all the recent rise may be attributed to the QE effect. But at the same time this analysis should throw some light on the topic.