Anwar Shaikh is one of the few economists who had warned about cracks in the foundations of growth of the US economy and the world economy as a whole and that it will lead to a crisis in the 2000s. He has a new book titled Capitalism: Competition, Conflict, Crises. It will be published around February next year.

The book and 1024 pages and looks like a huge analysis of all ideas in economics. You can preview the table of contents at amazon.com here. The book is published by Oxford University Press and the book’s page at OUP is here.

Anwar Shaikh is a very knowledgeable economist. In an interview to Ian Macfarlane, Wynne Godley says how much he learned about neoclassical economics from Anwar Shaikh. They then put up a paper titled An Important Inconsistency at the Heart of the Standard Macroeconomic Model. Wynne Godley considered it one of his most important papers. I like the paper and want to sometime rework it in a slightly different way to show that neoclassical economics makes no sense at all.

Anwar Shaikh, Levy Institute, May 2011, Photograph by me.

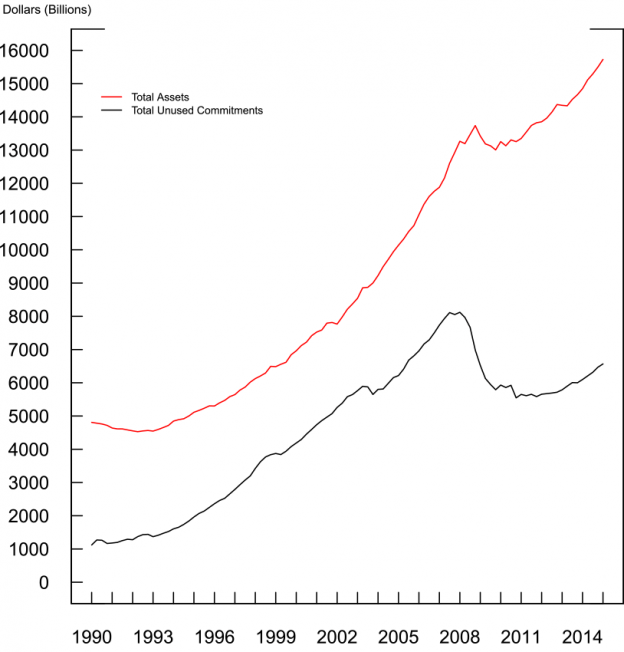

The Federal Reserve produces quarterly data for the financial accounts of the United States (earlier called “flow of funds”). There are a few notable additions termed enhanced financial accounts, which are in the process of being added. Some additions are details about money market mutual funds, off-balance sheet items of depository institutions, such as unused commitments, letters of credit and derivatives. This is the chart from the Federal Reserve’s FEDS note Off-Balance Sheet Items of Depository Institutions in the Enhanced Financial Accounts

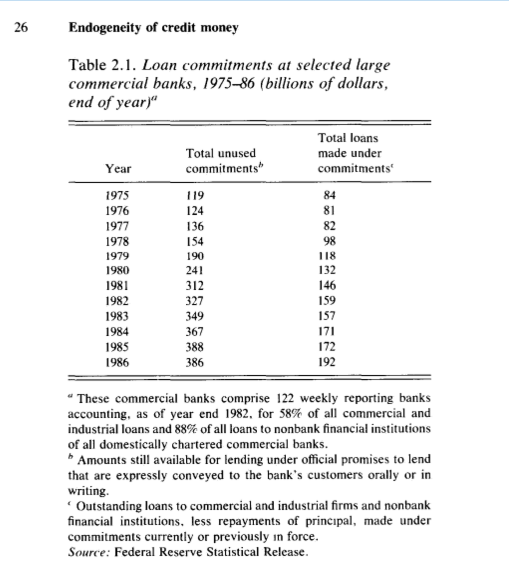

This data is probably not new but has been added in the report. Indeed it was one of the important points of Basil Moore’s book Horizontalists and Verticalists.

Moore has a sophisticated way of saying things (pages 24-25):

In making a loan commitment a bank should be viewed as a participant in forward rather than spot lending markets. Viewed as a seller of contingent claims, banks themselves obviously can excercise only limited control over the volume of their lending.

On page 186 of Moore’s book, he also notes that Keynes talks about this in his book A Treatise On Money:

Keynes insists that cash facilities of the public includes unused overdraft facilities, “of which we have no statistical record whatever” (JMK, 5, p. 37). He then concludes, “Thus the cash facilities, which are truly cash for the purposes of the theory of the value of money, by no means correspond to the bank deposits which are published” (JMK, 5, p. 38).

Tracking Keynes’ writing Moore concludes that although Keynes talked of unused overdraft facilities, he fails to recognize its importance in theory. Moore says (p. 203):

Keynes then returned to the issue of unused overdraft facilities, without, however, recognizing that this was the key to the endogeneity of the money stock:

[Keynes]: In Great Britain the banks pay great attention to the amount of their outstanding loans and deposits, but not to the amount of their customers’ overdraft faclities … it means that there is no effective pressure on the resources of the banking system until the finance is employed … there is no superimposed pressure resulting for planned activity over and above the pressure resulting from actual activity. (JMK, 14, pp. 222-23).

Honestly, I am not sure what Keynes is trying to say in all this. Moore is quite clear in his book. It’s still nice to know that Keynes discussed all this. Perhaps he wanted to say something more but couldn’t translate his thoughts in words. But if you can interpret Keynes, do tell me!

Recently, Paul Krugman reminded us of his “45 degree rule” on his blog Conscience Of A Liberal. This was a reference to his paper in 1989 which was a rediscovery of Thirlwall’s Law from 1979 [1] which states that the long run rate of growth of any country is constrained by the rate of growth of exports divided by the income elasticity of imports. Krugman rediscovered this law but interpreted the causality in the opposite way. This shouldn’t be surprising because in neoclassical economics, growth is explained by a production function and it is then difficult to interpret the causality in Thirlwall’s way. In an essay [2], John McCombie explains:

Krugman (1989) rediscovered Thirlwall’s Law, which he termed the 45-degree rule, as empirically ε/π = y/z or, when the (log) of the former is regressed on the (log) of the latter, the coefficient is unity or the slope of the line is 45-degrees. (Krugman provides some empirical evidence providing further confirmation of this empirical relationship). Like McCombie and Thirlwall (1994), he rules out sustained changes in the real exchange rate as a factor in bringing the balance of payments into equilibrium. Consequently, it is necessary to explain why the rule holds. The Keynesian explanation is that it is growth rates that adjust to maintain the balance of payments in equilibrium, but this is rejected by Krugman on “a priori grounds” that it is “fundamentally implausible.” He continues that “we all know that differences in growth rates among countries are primarily determined in the growth rates of total factor productivity, not differences in the rate of growth of employment; it is hard to see what channel links balance of payments due to unfavourable income elasticities to total factor productivity growth” (Krugman, 1989, p. 1037).

The Krugman article is instructive because it goes to the heart of the question about the direction of causation. Drawing on new trade theory, monopolistic competition, and the importance of increasing returns, he argues that faster growth leads to increased specialisation and the production of new goods for sale in overseas markets. Thus high “export elasticities of demand” are due to a dynamic supply side and rapid growth, rather than vice versa.

[x is the growth of the volume of exports, π is the domestic income elasticity of demand for imports, ε is the world income elasticity of demand for exports, and z is the growth of world income]

For a more forceful defence of Thirlwall’s Law, see McCombie’s paper.

In my opinion, the causality runs in both directions. However I am more sympathetic to Thirlwall and McCombie. And because the causality runs in both directions, there is still a balance-of-payments constraint. Complex economic dynamics still benefit richer nations and immiserate others. To an extent, this is already present in Kaldorian models. Growth brings in rise in productivity and this effects price competitiveness and hence beneficial to balance of payments generally. However, I also consider the income elasticity as being affected by growth at home and abroad.

References

Thirlwall, A. P. (1979) ‘The Balance of Payments Constraint as an Explanation of International Growth Rate Differences’, Banca Nazionale del Lavoro Quarterly Review, March.

McCombie, J.S.L. (2011) ‘Criticisms and defences of the balance-of-payments constrained growth model: some old, some new ‘, PSL Quarterly Review, vol. 64 n. 259 (2011), 353-392. (Can be previewed on Google Books here)

Few people are capable of expressing with equanimity opinions which differ from the prejudices of their social environment. Most people are even incapable of forming such opinions. — Albert Einstein, Essay to Leo Baeck (1953)