Paul Krugman writes today on his blog on James Tobin’s work:

Let me offer an example of how this ended up impoverishing macroeconomic analysis: the strange disappearance of James Tobin. In the 1960s Tobin developed and elaborated a sophisticated view(pdf) [original link corrected] of financial markets that offered insights into things like the role of intermediaries, the effects of endogenous inside money, and more. I’ve found myself using Tobinesque analysis a lot since the financial crisis hit, because it offers a sophisticated way to think about the role of finance in economic fluctuations.

But Tobin, as far as I can tell, disappeared from graduate macro over the course of the 80s, because his models, while loosely grounded in some notion of rational behavior, weren’t explicitly and rigorously derived from microfoundations. And for good reason, by the way: it’s pretty hard to derive portfolio preferences rigorously in that sense. But even so, Tobin-type models conveyed important insights — which were effectively lost.

Compare that to his article in response to another article on Wynne Godley which appeared in the New York Times – completely dismissing Godley’s work.

Three things: first Krugman claimed earlier that we needn’t look at old ideas:

But it is kind of funny to see a revival of old-fashioned macro hailed, at least by some, as the key to a reconstruction of the field

directly contradicting what he says today.

Second – obviously not having read Wynne Godley, he missed the point that Wynne’s analysis has significant improvement of James Tobin’s work.

Third, of course, Krugman’s understanding of monetary economics in general is poor, as can be seen when he gets into debates with heteredox economists and makes the most elementary errors. So it is strange he is lecturing others on this and fails once again to acknowledge heteredox economists.

Here’s Marc Lavoie describing in his article From Macroeconomics to Monetary Economics: Some Persistent Themes in the Theory Work of Wynne Godley in the book Contributions to Stock-Flow Modeling: Essays in Honor of Wynne Godley:

As Godley points out on a number of occasions, he himself owed his formalization of portfolio choice and of the fully consistent transactions-flow matrices to James Tobin. Godley was most particularly influenced and stimulated by his reading of the paper by Backus et al. (1980), as he writes in Godley (1996, p. 5) and as he told me verbally several times. The discovery of the Backus et al. paper, with its large flow-of-funds matrix, was a revelation to Godley and allowed him to move forward. But as pointed out in Godley and Lavoie (2007, p. 493), despite their important similarities, there is a crucial difference in the works of Tobin and Godley devoted to the integration of the real and monetary sides. In Tobin, the focus is on one-period models, or on the adjustments from the initial towards the desired portfolio composition, for a given income level. As Randall Wray (1992, p. 84) points out, in Tobin’s approach ‘flow variables are exogenously determined, so that the models focus solely on portfolio decisions’. By contrast, in Godley and Cripps and in further works, Godley is preoccupied in describing a fully explicit traverse that has all the main stock and flow variables as endogenous variables. As he himself says, ‘the present paper claims to have made … a rigorous synthesis of the theory of credit and money creation with that of income determination in the (Cambridge) Keynesian tradition’ (Godley, 1997, p. 48). Tobin never quite succeeds in doing so, thus not truly introducing (historical) time in his analysis, in contrast to the objective of the Godley and Cripps book, as already mentioned earlier. Indeed, when he heard that Tobin had produced a new book (Tobin and Golub, 1998), Godley was quite anxious for a while as he feared that Tobin would have improved upon his approach, but these fears were alleviated when he read the book and realized that there was no traverse analysis there either.

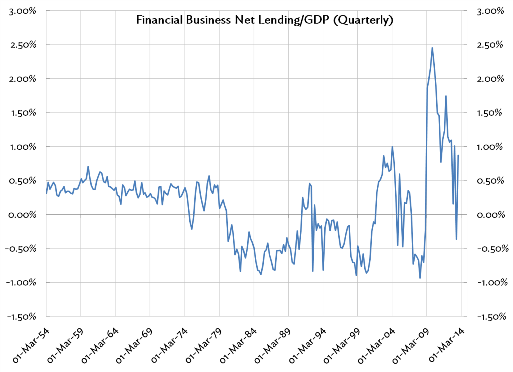

Draft link here.