Martin Wolf has a nice new column on imbalances creating troubles for the UK economy in the Financial Times: What a floating currency gives and what it does not.

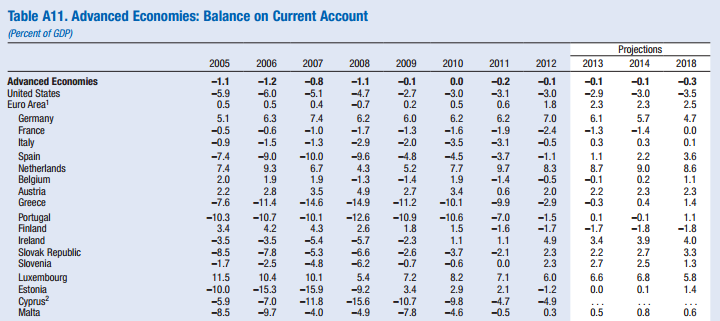

Why are current account deficits a haemorrhage in the flow of circular income? Weak external trade performance implies a drain in demand and hence pressure on the path to full employment and also that fiscal policy has to give in: else public debt and net indebtedness to foreigners keep rising relative to output which cannot be sustained for long. This means that if an individual nation or the world as a whole needs reflation, drastic changes need to made on how the world is run – especially using a system of regulated international trade rather than a system of free trade.

Nicholas Kaldor had a lot of change of mind about exchange rates during his lifetime. In the introduction to Volume 6 of his collected essays Further Essays On Applied Economics, he has a lot to say about his views.

Nicky Kaldor also had a paper The Relative Merits Of Fixed Exchange And Floating Rates – a memorandum as an economic adviser to the Chancellor in 1965 in which he was arguing for the merits of floating the exchange rates. In page xiii from introduction to Further Essays On Applied Economics he confesses:

The strategy advocated in my 1965 paper “The Relative Merits of Fixed and Floating Exchange Rates” thus proved in practice futile …

… So the policy which I advocated in the 1960s and developed at greater length in my 1970 Presidential Address to the British Association, of reconciling full employment growth with equilibrium in the balance of payments through adjusting the relationship between import and export propensities by a policy of continuous manipulation of the exchange rate, proved in the event a chimera. The main reason for this was that (along with most economists) I greatly overestimated the effectiveness of the price mechanism in changing the relationship of exports to imports at any given level of income. The doctrine that exports and imports are kept in balance through induced changes in their relative prices is as old and deeply ingrained as almost any proposition in economics.

So there you have it – realising his mistake earlier than anyone else.

He goes on further to drive this point:

… In other words, what the Harrod theory asserts is that trade is kept in balance by variations of production and incomes rather than by price variations: a proposition which implies that the income elasticity of demand of a country’s inhabitants for imports and those of foreigners for its exports are far more important explanatory variables than price elasticities.

which is essentially saying that it is non-price competitiveness which is far more important than price competiveness.

Further …

… If the Harrod theory provides the realistic explanation of the underlying forces which maintain the trade flows of an industrial exporter in balance (subject, of course, to the exceptions to this rule in the shape of long-term surplus and deficit countries, which must be capable of being explained in the same framework) this also carries the implication that the relationship of import propensities to exports will be relatively insensitive to such variations of relative prices as can be accomplished by monetary or exchange rate policies.

This latter implication (though discussed in the 1930s) seems to have got lost when the debate on fixed versus flexible exchange rates flared up again in the 1960s. This explains perhaps the exaggerated hopes placed on variations in exchange rates as an instrument of the “adjustment process” in international trade and payments and, for Britain in particular, on a system of “managed floating” as a means of securing higher and stable growth rates.

Again he later emphasises his learning:

… I was convinced that once exchange rates are freed from the rigidities imposed by Bretton-Woods, the forces of cumulative causation which made some countries grow fast and others slowly will no longer operate, or not in the same manner. That belief was so badly shaken by experience of subsequent years for for reasons explained in my most recent paper on the subject, which is discussed below.

James Tobin said it best once:

I believe that the basic problem today is not the exchange rate regime, whether fixed or floating. Debate on the regime evades and obscures the essential problem.

Of course that doesn’t mean one ties both shoes together and irrevocably fixes exchange rates (and give up the government powers to make drafts at the central bank) but the essential problem referred above – although gets diluted – doesn’t go away outside a monetary union.