Happy New Year 2012 and it is a nice opportunity for me to thank you much for visiting my blog.

(Card courtesy: Hallmark)

Hyman Minsky and Money

Did Hyman Minsky truly understand the endogenous nature of money?

The Levy Institute is one my favourite places in the world, but have been there only once :(. Here’s a picture of the nice garden at the institute I took.

Brings me to the main point of my post. The Institute has made an archive of Minsky’s works and you can reach the page by clicking the link below:

I came across a discussion on whether Minsky was really stuck with the loanable funds model of credit. I found an article he had written titled “Financial Institutions, Economic Policy and the Dynamic Behavior of the Economy” with two co-authors in 1994.

On page 10 (i.e., page 12 of the pdf document) the authors have this to say:

Further on page 12 (page 14 of the pdf):

Decide for yourself on the question posted earlier.

Update 22 January 2012: Withdrew a statement made on Sir Dennis Robertson

I have been reading this article/blog post The Curse of Tina by Adam Curtis of the BBC – it’s a long article and there are several videos in the post, making it a long read. What led me into the article was the discussion of policies put forward by Monetarists which led to a damage of the British economy in the 70s and the 80s. The IEA – Institute of Economic Affairs – called Monetarism “scientific” (!) and persuaded the government in adopting its policies. Overall, the article gives a good glimpse of failed policies over so many years. (Nevermind the author’s mistaken belief that there is no alternative)

Of course, the best source for this is Nicky Kaldor’s The Scourge Of Monetarism (Oxford University Press, 1982). Kaldor had a supreme understanding of banking and the endogenous nature of money. In the book, he wrote:

As it is, a highly developed banking system already provides such facilities on an ample scale, since it is prepared to accommodate the public’s changing demand between different types or financial assets by altering the composition of the banks’ assets or liabilities in a reverse direction. If the non-banking public wishes to switch its holding of gilts for interest-bearing bank deposits, the banks are ready to supply such deposits at the minimum of inconvenience, and at the same time to place their surplus funds into the gilts which were previously held by the public. Similarly the banks provide easy facilities to their customers for switching balances on current accounts into interest-bearing deposit accounts, or vice versa. Hence, while the annual increment in the total holding of financial assets of the private sector (considered as a whole) is nothing more than the mirror-image of the borrowing requirement of the public sector (in a closed economy at any rate), neither the Government nor the banks can determine how much of this increment will be held in the form of cash (meaning notes and current deposits) and how much in the near-equivalents to cash (such as interest-bearing demand deposits) or in various forms of public sector debt. Thus neither the Government nor the central bank can control how much or the total financial assets the public prefers to hold in the form of ‘money’ on one particular definition or another.

*I initially thought Adam Curtis as saying that there is no alternative which he was not – he probably just meant that according to politicians there is no alternative. I thank Philip Pilkington in pointing this out).

On 8 Dec, the European Central Bank announced that it will conduct two Longer-Term Refinancing Operations (LTRO) with a maturity of 36 months – one each in December and February. According to the initial press release,

The operations will be conducted as fixed rate tender procedures with full allotment. The rate in these operations will be fixed at the average rate of the main refinancing operations over the life of the respective operation. Interest will be paid when the respective operation matures.

The allotment was made today and banks borrowed around €489bn.

The ECB had also given banks an option to shift previous funding:

Counterparties are permitted to shift all of the outstanding amounts received in the 12-month LTRO allotted in October 2011 into the first 3-year LTRO allotted on 21 December 2011.

And according to today’s press release,

The allotment amount of EUR 489,190.75 million includes EUR 45,721.45 million that were moved from the 12-month LTRO allotted in October 2011. A total of 123 counterparties made use of the possibility to shift, whereas 58 banks decided to keep their borrowing in the 12-month LTRO, which has now a remaining outstanding amount of EUR 11,213.00 million.

Another feature of today’s allotment was that Italian banks issued bonds backed by their sovereign and retained the issuance to place them as collateral with their Banca d’Italia – their home NCB for their bids. According to FT Alphaville,

According to Reuters, 14 Italian banks have listed €38.4bn worth of state-guaranteed bonds ahead of the LTRO.

More information:

RTRS-ITALIAN BANKS TAPPED ECB’S NEW 3-YR LOANS FOR MORE THAN 110 BLN EUROS – ITALIAN BANKING SOURCE

RTRS: 14 Italian banks win clearance for state-backed bond issues worth EUR 57-58bln, figure includes EUR 38.4bln already listed – sources

Another reason the auction received so much attention was due to the huge speculation that banks will borrow from the Eurosystem and use it to purchase the debt of their sovereigns and even other Euro Area governments. To me, this is nothing more than speculation because it fails to understand how banks work – the LTRO was to help banks meet their funding needs. It is true that some banks (and only a few) may have done this “carry trade” but it is highly risky and as Megan Greene of Roubini Global Economics put it,

This sort of carry-trade could be extremely dangerous, because it not only fails to break the banking/sovereign feedback loop, it actually strengthens it.

Gavyn Davies of FT had this to say in his blog (which is a fine explanation).

The French government was very explicit that the liquidity injection could be used by banks to buy sovereign debt with a large positive carry. This will almost certainly prove too optimistic, since the banks need the money to redeem their own bonds, not to buy risky debt from sovereigns. Nevertheless, the ECB is certainly preventing banks from selling sovereign debt that they otherwise would have sold, and it is doing this by expanding its own balance sheet. …

In recent posts on the Eurosystem, I looked at how it operates and in The Eurosystem: Part 2 highlighted how capital flow across borders within the Euro Area has led to a large accumulation of TARGET2 balances by some NCBs such as the Deutsche Bundesbank.

If the euro zone breaks into sorry little pieces, Germany could possibly lose its entire €495 billion claim. That’s more than $650 billion. It is 60 percent bigger than Germany’s annual federal budget—and larger than the lending under the European Financial Stability Facility and other aid programs that have received more scrutiny.

Some experts on TARGET2 disagree. So I got into an argument with a blogger (who has a good understanding of TARGET2, btw) according to whom

But let’s take a closer look. Who is this “Germany”? Will the German residents who got their accounts credited as a result of the Target2-facilitated transfers out of Ireland now lose their money? No. There will be no losses to private citizens. Despite all this misleading stuff about “enforced lending”, German citizens will be very grateful that they managed to repatriate their money to German via Target2.

So “Who is Germany”? Hidden in the above quote is that individuals and corporations only make Germany and that if the Euro collapses and hence the European Central Bank goes out of existence, Germany’s Bundesbank’s TARGET2 loss of €465bn (latest data I could get) will be not really a loss for “Germany”. This can be dismissed easily.

According to the IMF’s Balance Of Payments And International Investment Position Manual or BPM6

The IIP is a statistical statement that shows at a point in time the value of: financial assets of residents of an economy that are claims on nonresidents or are gold bullion held as reserve assets; and the liabilities of residents of an economy to nonresidents. The difference between the assets and liabilities is the net position in the IIP and represents either a net claim on or a net liability to the rest of the world.

A nation’s net wealth is the value of its real assets and its net international investment position. This definition has a Mercantalist bias but they have been proven right many times! A loss of Germany’s TARGET2 balance will represent a loss to Germany as a whole. Let us look at this closely with some real numbers.

According to the Bundesbank’s Balance of Payments Statistics, November 2011, (with English translation below)

(click to enlarge)

(click to enlarge)

Germany had assets of €6,158bn and liabilities of €5,209bn and thus a net asset position of around €949bn.

The table columns 26 and 27 show how Bundesbank’s foreign assets have increased recently but aren’t fully updated. Another table from the publication gives the updated numbers.

(click to enlarge)

with the English translations:

(click to enlarge)

So the Deutsche Bundesbank had a TARGET2 balance of €465bn at the end of October and is still rising! This is a sizable fraction of the net asset position of €949bn. (for other comparions, Germany’s 2010 GDP was €2,499bn).

The reason I went through this detail was to help the reader appreciate the question “Who is Germany”. Many breakup scenarios may put Germany at the risk of losing out this huge asset. No domestic transaction will bring this back to the original level.

There are even more dreadful scenarios one can think of. A sudden loss of confidence and a dramatic “flight to quality” will lead residents and foreigners selling foreign assets in the Euro Area (in addition to non-Euro denominated assets) and shifting the liquidated deposits via TARGET2 to German banks and if Germany loses its TARGET2 balance, it could become a net debtor to the rest of the world!

An example will illustrate this. Suppose there is a further shift of €1,000bn before a Eurocalypse. This will lead to Germany’s gross assets increasing from €6,158bn to €7,158bn and liabilities from €5,209bn to €6,209bn, leaving the net position unchanged but increasing the Bundesbank’s TARGET2 position from €465bn to €1,465bn. A potential impairment of 100% implies that Germany’s Net International Investment Position is minus €516bn. All this ignoring residents’ revaluation losses of assets held abroad in such scenarios which will make the whole thing even more disastrous!

The above analysis is for non-residents inside the Euro Area making a financial flight to quality into Germany. For residents, a shift of say €1bn does not increase gross asset and liability positions – as far IIP construction is concerned – but increases Bundesbank’s TARGET2 assets by €1bn with the same effect as above.

In either case – residents or non-residents – Germany’s net asset position is under high risk because of the potential loss due to Bundesbank’s TARGET2 balance vanishing in thin air.

Of course, it won’t be an immediate risk to Germany in the sense that it can go back to the Deutsche Mark and redenominate debts in the new currency and do a fiscal expansion to prevent a loss in output. At any rate, Germany’s wealth which it earned in all these years would have reduced – a Mercantalist’s nightmare.

FT has an article today on Christine Lagarde’s warning

about a 30s style depression and that

faces the prospect of “economic retraction, rising protectionism, isolation and . . . what happened in the 30s [Depression]”

The video is below. Lagarde’s speech starts at 13:00 and ends at 25:25

click to watch the video on YouTube

Lagarde rightly stresses the “vast interconnectedness” between all economies and that that the crisis can be resolved only by all countries taking action.

Gillian Tett of FT wrote a bio of Christine Lagarde recently. It has more about her shoes than economics.

Charles Goodhart and Dirk Schoenmaker just released their article on a game plan for saving the Euro, which is approaching its endgame. According to them,

An EZ Minister of Finance without money is like an emperor without clothes. There are proposals to have tax capacity capable of funding a budget of about 2% of European GDP (Marzinotto et al 2011; Goodhart 2011). This 2% should cover most eventualities, including effective stabilisation policies. Yet there may be exceptional circumstances, for example, relating to banking resolution where more is needed (the deep pockets of government).

Given the severe imbalances in the Euro Area, this looks too low. Really 2%? A recent empirical study done by The Economist for the United States suggests otherwise.

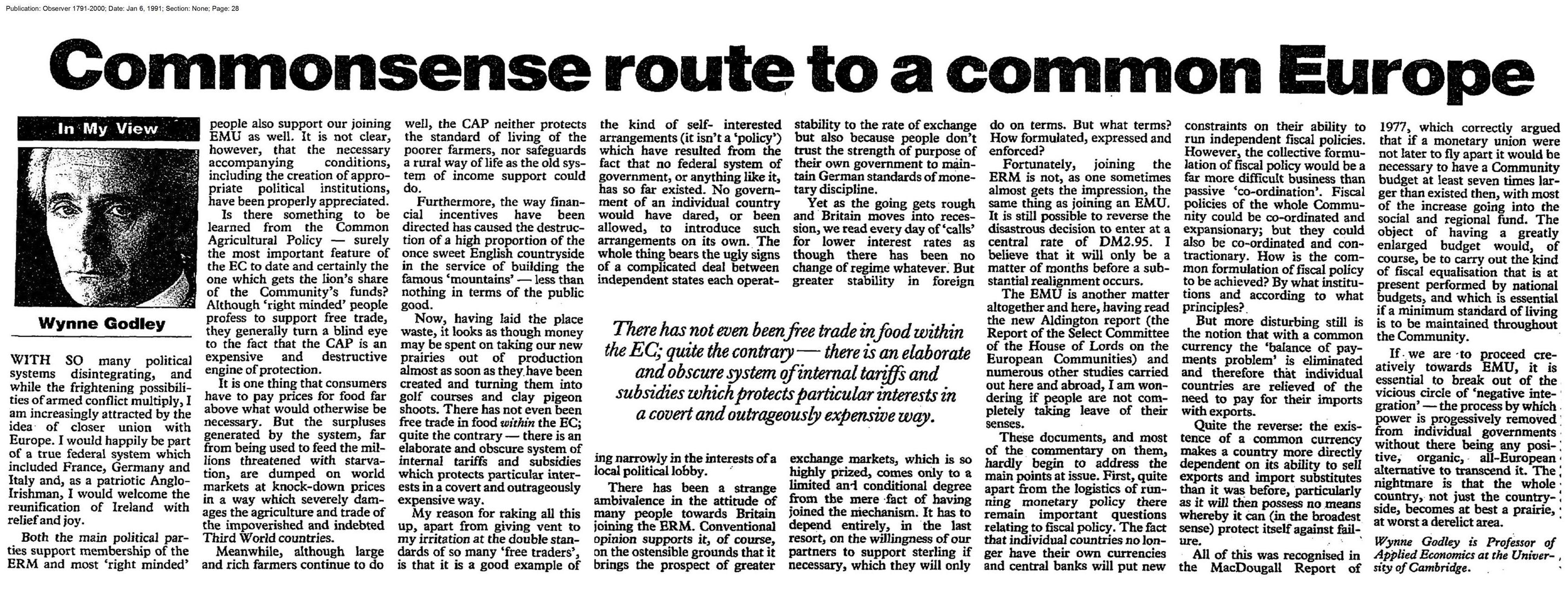

What is wrong with the Euro Area? Wynne Godley said this best in an article (written in 1991) in The Observer titled “Commonsense Route To A Common Europe”. Scan here

But more disturbing still is the notion that with a common currency the ‘balance or payments problem’ is eliminated and therefore that individual countries are relieved of the need to pay for their imports with exports.

Quite the reverse: the existence or a common currency makes a country more directly dependent on its ability to sell exports and import substitutes than it was before, particularly as it will then possess no means whereby it can (in the broadest sense) protect itself against failure.

All of this was recognised in the Macdougall Report of 1977 which correctly argued that if a monetary union were not later to fly apart it would be necessary to have a Community budget at least seven times larger than existed then, with most of the increase going into the social and regional fund. The object of having a greatly enlarged budget would, of course, be to carry out the kind of fiscal equalisation that is at present performed by national budgets, and which is essential if a minimum standard of living is to be maintained throughout the Community.

[emphasis added ;-)]

The Macdougall Report is available from the European Commission website: Part 1 and Part 2. Haven’t read it, so my knowledge is restricted to the above quote, and it adds to my huge list of things to do.

At the time of writing, I believe the situation was much different. The imbalances in the “three sectors” (public, private and external) is now severe in the Euro Area. (Three for each country, so actually 17 x 3)

Sir Donald Macdougall died in 2004 and according to The Guardian‘s obituary:

His career – as an Oxford don, a London “special adviser”, a mover and shaker in Whitehall and Westminster – started before the second world war, and wound down with skilful “letters to the editor” against the euro.

There have been so many proposals on attempts to rescue the Euro Area. Ideas termed “monetary financing” by the European Central Bank carry tremendous risks of exacerbating imbalances within the Euro Area, because nations will keep relying on the Eurosystem’s financing and is a potential political time-bomb. And, there are those simpletons, who argue that nations should just walk away! As if …

To me, it looks as if the European leaders know that the size of the central government and the fiscal transfers would be substantial given Macdougall’s estimations were done when the situation was much different and a redoing may prove this. It is the political unacceptability of this, which will finally lead to Eurocalypse.

Excellent analysis of the EU Summit by Martin Wolf on FT using the sectoral balances approach:

…

Let me make this point by turning last week’s analysis of the balance of payments into one of foreign, private and government financial balances in eurozone members (see charts). To remind readers: these have to add up to zero, by definition. But how they go about adding up is revealing.

As I noted last week, fiscal imbalances were modest before the crisis, but the current account imbalances were huge. Surplus private funds in some countries (notably Germany and the Netherlands) were intermediated by the financial system to fund private deficits in others (notably Greece, Ireland, Portugal and Spain). When crisis hit, these flows ceased. Deficits of private sectors collapsed (most turning into surpluses), while fiscal deficits exploded. Now, says Germany, the latter must be slashed.

By definition, the sum of private and current account deficits must also fall towards zero. The private sectors of erstwhile capital-importing countries have moved towards surpluses, for a good reason: they are trying to reduce their debts, not least because their assets are falling in value. Thus the external deficit needs to fall. That can occur in a good or a bad way. The good way would be via increased output of exports and import substitutes; the bad would be via a deeper recession. The good way requires far higher imports in the core of the eurozone or far greater competitiveness for the eurozone as a whole. But little chance of either of these exists, under plausible expectations for demand and activity. That leaves the bad way: deep recessions, in which the government reduces its deficit by deflating the private sector yet more.

In brief, it is extremely difficult to eliminate fiscal deficits in the structural capital-importing countries, without prolonged recessions or huge improvements in their external competitiveness. But the latter is relative, so the needed improvements in the external performance of weak eurozone countries imply a deterioration in that of eurozone capital-exporters, or radically improved external performance for the eurozone as a whole. The former means that Germany becomes far less German. The latter implies that the eurozone becomes a mega-Germany. Who can believe either outcome is plausible?

This leaves much the most plausible outcome of the orgy of fiscal austerity: long-term structural recessions in vulnerable countries. To put it bluntly, the single currency will come to stand for wage falls, debt deflation and prolonged economic slumps. Can this stand, however big the costs of a break-up?

The eurozone has no credible plan to fix the flaws of the eurozone, apart from greater fiscal austerity: there is to be no fiscal, financial or political union; and there is to be no balanced mechanism for economic adjustment on both sides of the creditor-debtor divide. The decision is, instead, to try still harder with a stability and growth pact whose failures have been both predictable and persistent.

This is the fifth part of the series of posts on the description of the Eurosystem. In this post, I will discuss whatever I had kept postponing in previous posts – except central bank swaps, which I will postpone to Part 6.

The Euro Area is comprised of 17 nations using the Euro as the legal tender and this is referred to as EA17. In addition, 10 more nations potentially can join the Euro, so they refer to “EU27”. In the recent “summit to end all summits”, European leaders believed in Merkels and worked toward changing the Treaty. UK’s Prime Minister David Cameron refused to sign the new European accord – a wonderful thing to do.

[The UK always had an opt-out option and this move effectively divorces the UK from EU. The other nation with an opt-out is Denmark. The remaining 8 are: Bulgaria, Czech Republic, Hungary, Latvia, Lithuania, Poland, Romania and Sweden. The Wikipedia entry Enlargement of the Euro Zone has good details.]

Before the summit of political leaders, the ECB, in its monthly monetary policy meeting, decided to take steps to improve banks’ conditions: It will now conduct two LTROs with a maturity of 36 months and reduced reserve requirements from 2% to 1%. Other than that, it allowed NCBs to accept bank loans satisfying certain criteria as collateral and reduced the ratings threshold on Asset-Backed Securities. Before this, the maximum maturity of LTRO till date was 1 year.

In the press conference that followed, Mario Draghi, the President of the ECB, dashed market hopes of a more aggressive intervention of the ECB in the markets. The press conference transcript is here. However, analysts saw this as a signal from the ECB to force Euro Area governments into agreeing into fiscal contraction ahead of the summit and still expect the ECB to intervene.

Securities Markets Programme

Back in May 2010, the ECB observed that yields of a few “peripheral” government bonds were rising and it looked as if it could become a “self-fulfilling prophecy” and decided to intervene in the markets. In the ECB’s words, the Governing Council decided to:

To conduct interventions in the euro area public and private debt securities markets (Securities Markets Programme) to ensure depth and liquidity in those market segments which are dysfunctional. The objective of this programme is to address the malfunctioning of securities markets and restore an appropriate monetary policy transmission mechanism. The scope of the interventions will be determined by the Governing Council. In making this decision we have taken note of the statement of the euro area governments that they “will take all measures needed to meet [their] fiscal targets this year and the years ahead in line with excessive deficit procedures” and of the precise additional commitments taken by some euro area governments to accelerate fiscal consolidation and ensure the sustainability of their public finances.

In order to sterilise the impact of the above interventions, specific operations will be conducted to re-absorb the liquidity injected through the Securities Markets Programme. This will ensure that the monetary policy stance will not be affected.

The outstanding amount held (settled, to be precise) by the Eurosystem as on Dec 2 was about €207bn, as per this link.

This has continued to rise in recent months because of rising yields of government bonds with markets suspecting that the public debts of Spain and Italy are on unsustainable territory. So the Eurosystem intervenes frequently and the market participants quickly figure this out.

Who Buys – NCBs or ECB?

Some people have asked me – who buys the bonds: NCBs or the ECB? The answer – I believe – is both. Someone asked me if there are traders in the ECB building at Frankfurt. I do not know – perhaps a few. Someone pointed out that the ECB may be buying using the NCB as its agent. Possible. There’s another question, which nobody has asked me – does an NCB of country A buy government bonds of country B? I think so. Who decides all this is not an easy question!

For example, according to the Banque de France Annual Report 2010, (page 118 of publication, 108 of pdf)

The total amount of securities held by NCBs of the Eurosystem under the SMP increased to EUR 60,873 million, of which EUR 9,353 million are held by the Banque de France and are shown under asset item A7.1 in its balance sheet. Pursuant to Article 32.4 of the ESCB statute, any risks from the holding of securities under the Securities Markets Programme, if they were to materialise, should eventually be shared in full by the NCBs of the Eurosystem in proportion to the prevailing ECB capital key shares.

Assuming, the Eurosystem didn’t need to buy French government bonds till now, (at least till 2010 end), it seems it has purchased government bonds of other EA17 nations.

What about the ECB? Yes. According to the ECB Annual Report 2010, page 223 (page 224 of pdf):

Compare that to the Eurosystem’s consolidated balance sheet item (7.1 below) which was large compared to €17.9bn above at the end of 2010:

Also, according to Banca d’Italia’s Annual Report 2010 (page 224 of publication, 231 of pdf):

“Securities held for monetary policy purposes” was about €18bn at the end of 2010, of which about €8bn was in government bonds under SMP and the remaining covered bonds.

So to summarize, government debt is purchased by all NCBs and the ECB and the NCB purchase is not restricted to purchasing government bonds of the same nation the NCBs are located.

The same is true with the Covered Bonds Purchase Programme. The latter is somewhat equivalent to the Federal Reserve’s purchase of Agency Mortgage-Backed Securities in the United States. Covered Bonds are somewhat similar to Asset-Backed Securities such as MBS; the former are on balance sheet of the issuing bank, unlike the latter which are moved into Special Purpose Entities. The assets backing covered bonds are clearly identified in a “cover pool” and are “ring-fenced” which means that if the issuing bank closes down due to insolvency, the assets in the covered pool will be used to pay the covered bond holders, before they are available to unsecured creditors including depositors. The reason the ECB has chosen covered bonds instead of ABS is because of the strength of the covered bond lobby in Europe.

Emergency Loan Assistance

Imagine the following. A Euro Area country X’s government bond yields are at rising and the bond markets are highly suspicious of the government’s solvency. Banks are also in a bad situation and funds have made frequent flights out of the country. The banks have provided all collateral they had to their home NCB. (To be technically correct, foreign assets are pledged to the respective foreign NCB who acts as a custodian for the home NCB). The government has €8bn of payments to bond holders this week. The government has enough funds deposited at a local bank, so it can meet its obligations. However, most bond holders are foreigners. When the government pays the bond holders, the payment will go through via TARGET2 and commercial banks will run out of collateral to provide to their home NCB.

The above is one way in which banks can run out of collateral and there are other ways in which the government is not the direct reason for the outflow of funds, such as a simple capital flight. For this reason, some NCBs invented a programme called “Emergency Loan Assistance” which may not have been a terminology used in the Treaty. The relevant article which may provide an NCB with this power is the Article 14.4 of the Statute of the ESCB and of the ECB

14.4. National central banks may perform functions other than those specified in this Statute unless the Governing Council finds, by a majority of two thirds of the votes cast, that these interfere with the objectives and tasks of the ESCB. Such functions shall be performed on the responsibility and liability of national central banks and shall not be regarded as being part of the functions of the ESCB.

The situation highlighted above happened frequently with Greece during the past few months. The ELA, however was first used by Ireland in 2010. From the Central Bank of Ireland Annual Report 2010

(click to expand)

The item highlighted “Other Assets” contains the balance sheet item for Emergency Loan Assistance. More below, but before this, it is instructive to look at Liabilities:

(click to enlarge)

So, the Central Bank of Ireland’s Liabilities to the rest of the Eurosystem was around €145bn! – which is indicative of how much funds flew out of Ireland and the amount of stress the nation went through. (Ireland’s 2010 GDP was €154bn, btw). I described how funds flow within the Euro Area in Part 2 of this series.

Back to ELA. Page 104 of the publication (106 of the pdf) describes Other in Other Assets as:

This includes an amount of €49.5 billion (2009: €11.5 billion) in relation to ELA advanced outside of the Eurosystem’s monetary policy operations to domestic credit institutions covered by guarantee (Note 1(v)). These facilities are carried on the Balance Sheet at amortised cost using the effective interest rate method. All facilities are fully collateralised and include sovereign collateral as well as a broad range of security pledged by the counterparties involved.

The Bank has in place specific legal instruments in respect of each type of collateral accepted. These comprise: (i) Promissory Notes issued by the Minister for Finance to specific credit institutions and transferrable by deed, (ii) Master Loan Repurchase Deeds covering investment/development loans, (iii) Framework Agreements in respect of Mortgage-Backed Promissory Notes covering non-securitised pools of residential mortgages, (iv) Special Master Repurchase Agreements covering collateral no longer eligible for ECB-related operations and (v) Facility Deeds providing a Government Guarantee. In addition, the Bank received formal comfort from the Minister for Finance such that any shortfall on the liquidation of collateral is made good. Where appropriate, haircuts (ranging from 5.5 per cent to 80 per cent) have been applied to the collateral. Credit risk is mitigated by the level of the haircuts and the Government Guarantee. At the Balance Sheet date no provision for impairment was recognised.

You can find details of these in this blog post Irish Central Bank Comfort at the blog called Corner Turned, which is now inactive.

Oh yeah … How does the Irish NCB provide the loans? Hint: Loans make deposits.

FT Alphaville has two nice posts (among others) on ELA in Greece: Sundry secret Greek liquidity [updated], Hooray for, erm, Greek ELA?. The first one pokes on how the Bank of Greece – Greece’s NCB – hides the item under “Sundry” and the second one one how Greek banks’ net interest income were higher than expected – the reason being that expensive deposits were replaced by cheaper NCB funding!

This concludes this post. In Part 6 – the final one – I will discuss central bank liquidity swap lines with the Federal Reserve.

Kevin O’Rourke of Oxford University has a post on Project Syndicate, correctly titled A Summit to the Death, in which he nicely summarizes the recent EU “summit to end all summits” held at Brussels. He says

With this in mind, the most obvious point about the recent summit is that the “fiscal stability union” that it proposed is nothing of the sort. Rather than creating an inter-regional insurance mechanism involving counter-cyclical transfers, the version on offer would constitutionalize pro-cyclical adjustment in recession-hit countries, with no countervailing measures to boost demand elsewhere in the eurozone. Describing this as a “fiscal union,” as some have done, constitutes a near-Orwellian abuse of language.

As, FT Alphaville put it appropriately, “Do you believe in Merkels?”

It’s a dark age for Macroeconomics, as Paul Krugman put it – except for a few like Stephen Kinsella (from the Univesity of Limerick, Ireland), who is taking up the challenge of making stock-flow coherent models more practical and using them to come up with policy proposals, scenarios under different policies, etc for the Irish economy. Here’s an interview by INET

{kind=link}