Recently Financial Times had an article A Keynesian Solution to Global Imbalances (‼) by Daire Macfedden.

Martin Wolf at FT also discussed global imbalances in Why Global Imbalances Matter with the intro text:

They lie at the intersection of almost everything that matters in geoeconomics and geopolitics.

This is welcome, but you need to keep in mind that Bancor is not a complete solution.

In stock-flow consistent models, you can see that the most important things governing the world economy are fiscal policy and international trade. Hence, you get expressions such as

as a first approximation of GDP, where the variables are, respectively: government expenditure, exports, the tax rate, and the propensity to import.

John Maynard Keynes:

- was right about global imbalances (even if the terminology is more recent),

- underestimated the importance of trade,

- and therefore proposed Bancor—not exactly a complete solution.

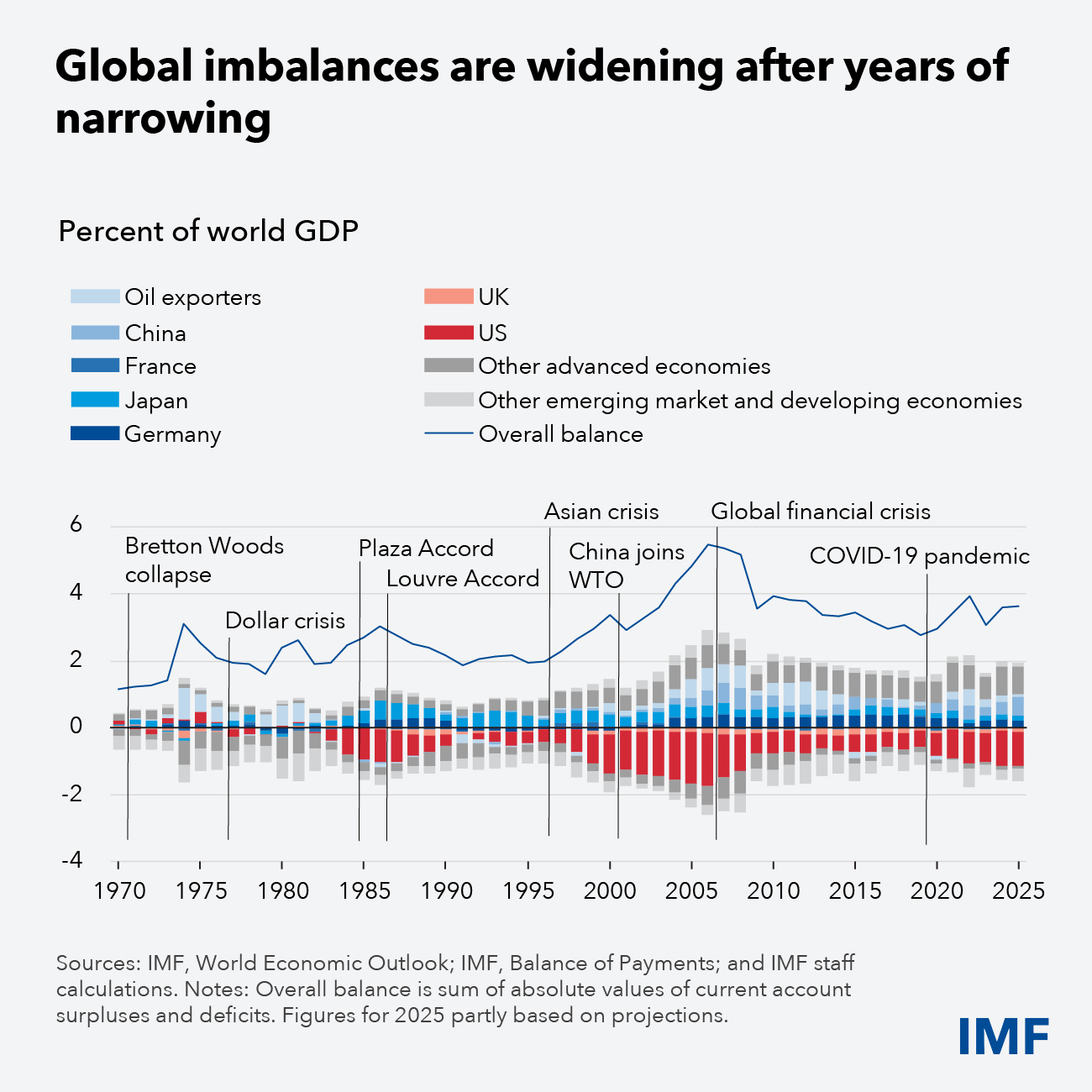

The main problem is that we live in an economic order with free trade, and deficit countries are constrained from expanding demand because they face balance-of-payments problems, while surplus countries are constrained by an ideology that discourages demand expansion.

Even deficit countries can expand demand until they hit a binding constraint. But the problem is that politicians and the corporations that fund them are often dogmatically opposed to fiscal expansion. So there is a bias toward tight fiscal policy in both surplus and deficit countries.

So, in his plan for Bretton Woods, Keynes proposed Bancor, along with penalties on creditor nations, and also required them to take measures such as:

(a) Measures for the expansion of domestic credit and domestic demand.

(b) The appreciation of its local currency in terms of bancor, or, alternatively, the encouragement of an increase in money rates of earnings.

(c) The reduction of tariffs and other discouragements against imports.

(d) International development loans.

[The Collected Writings of John Maynard Keynes, Volume XXV: Shaping the Post-War World: The Clearing Union, Chapter 1, The Origins of the Clearing Union, 1940–1942]

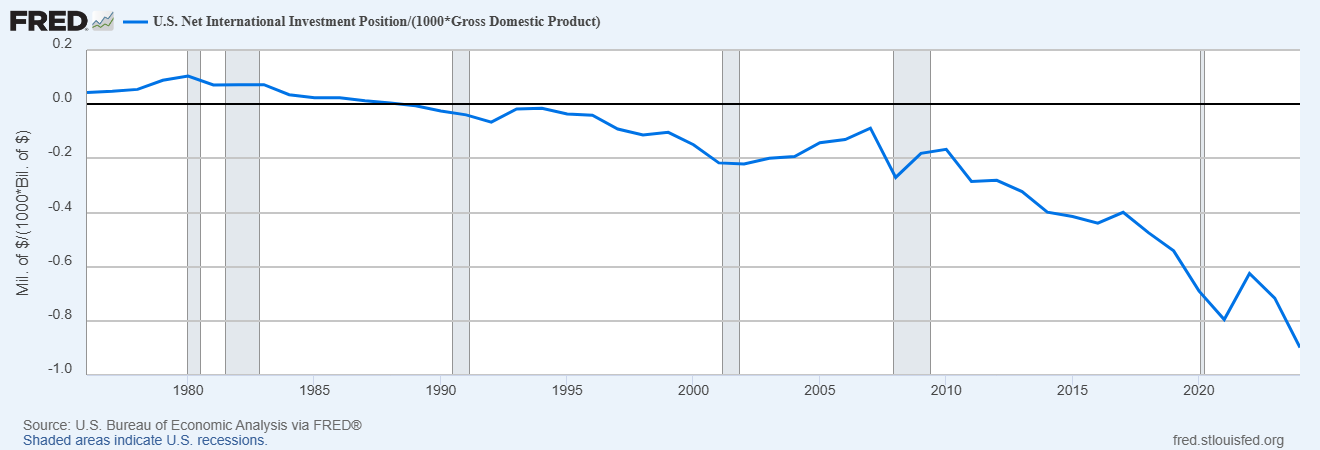

Now, the Bancor rules work when Bancor balances move outside a certain range. However, Bancor balances are neither the current account balance nor a stock measure such as the net international investment position.

In fact, Bancor balances can be positive even while a country is running large current account deficits and accumulating a large negative net international investment position.

So while the discussion is moving in the right direction, it is important to realise that pundits may downplay the problem in the same way Keynes did, leaving us with a solution that is far less effective than directly targeting measures such as current account balances and the net international investment position.