I was rereading the articleKeynes And The Management Of Real National Income And Expenditure by Wynne Godley from 1983 (page 157 in that book, footnote 20) and he reminds us of this letter from JMK published in The Collected Writings Of John Maynard Keynes, Volume XXVI, pages 287-289, that he thought that import controls work much better than movements in the exchange rates.

To J. M. FLEMING, 13 March 1944

Dear Fleming,

Your paper on quotas versus depreciation, sent me with your letter of February 14th, raises a very interesting question. But, for my own part, I am not one of the’ most economists’, to whom in paragraph 2 you attribute the view that disequilibrium ought, so far as possible, to be corrected by movements in the rate of exchange rather than by controls over commodity trade.

There is, first of all, to the contrary the simple-minded argument that, after all, restriction of imports does do the trick, whereas movements in the rate of exchange do not necessarily do so.

Senate Poised To Pass Huge Industrial Policy Bill To Counter China is the headline of a recent news item from The New York Times.

US politicians have come to realise—especially after the rise of Trump—that free trade and globalisation is a major cause of damage to the US economy. The purpose of industrial policy is to make US producers more competitive. This results in increase of exports and fall in imports, relative to gdp.

Wynne Godley had been warning for quite some time on how the US government should address the trade imbalance instead of leaving it to market forces. In March 2003, in an articleThe U.S. Economy: A Changing Strategic Predicament he said:

The default conclusion is that the U.S. economy will not recover properly in the medium term, but rather will enter a prolonged period of “growth recession.” The only lasting solution will be to get U.S. exports to rise much faster than imports over a prolonged period.

And also suggested non-selected protectionism for the short term.

Another recent news article from NYT is about a global tax coordination. Globalisation has led to a race to the bottom. To raise price competitiveness, countries have been wrongly incentivised to reduce tax rates on firms and this led to some competition between countries to keep reducing tax rates on corporations. And this has led to lot of economic damage.

The Democratic Party of the US has learned from mistakes in the past and is trying to correct them but the Dems are total corporatists and these measures are just for elite preservation. For example, they were talking of reversing Trump’s tax cuts for corporations but the party is a champion in performative politics: it seems they’re not reversing it now.

As Joseph Stiglitz points out, the problem with this 15% tax rate is that it become the de facto the maximum tax rate.

In his last paper, Wynne Godley said on rebalancing:

It is inconceivable that such a large rebalancing could occur without a drastic change in the institutions responsible for running the world economy—a change that would involve placing far less than total reliance on market forces.

Although the steps taken by the US government looks in the right direction, there’s still a large way to go, especially considering how the Democrats pretend to do all sorts of good things. Still far from a Keynes like plan to fine surplus countries and to remove imbalances in balance of payments and international investment position.

There was a conference on the 10th death anniversary of Wynne Godley last year. If you haven’t seen it, the video recordings/presentation/remarks are in that link.

Now, there’s a special issue by the JPKE about the conference with papers as in the cover:

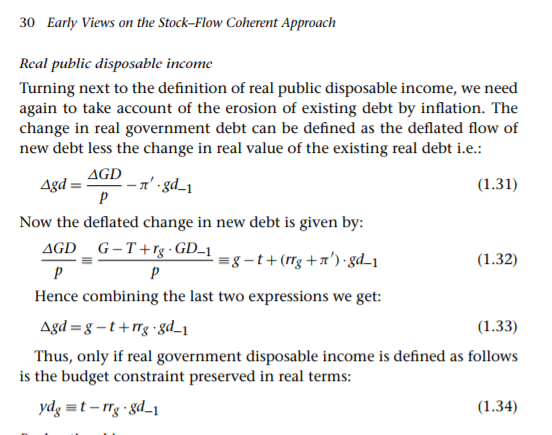

A good macroeconomic model would use national accounts and the flow of funds with behavioural hypotheses. It’s complicated by the fact that prices of goods and services change. It’s not just that if prices of goods and services change, you’re consumption would change in response to that, but also because say the deposits you hold in the bank is worth less.

So your behavioural equations need to be modified. It’s not easy. Wynne Godley recalls in his book Monetary Economics:

And no lesser authority than Richard Stone (1973) made the same mistake because in his definition of real income he did not deduct the erosion, due to inflation, of the real value of household wealth.

…

References

…

Stone, R. (1973) ‘Personal spending and saving in post war Britain’ in H.C. Bos, H. Linneman and P. de Wolff (eds), Economic Structure and Development: Essays in Honour of Jan Tinbergen (Amsterdam: North Holland), pp. 75–98.

The system of national accounts does recognise the importance of this but there aren’t any real variables defined. Real as opposed to nominal. Instead holding gains (formal phrase for “capital gains”) is divided into two parts: real holding gains and neutral holding gains. So,

Assets prices can rise differently than prices of goods and services. Para 12.89 says:

The real holding gain on an asset is defined as the difference between the nominal and the neutral holding gain on that asset. The values of the real holding gains on assets thus depend on the movements of their prices over the period in question, relative to movements of other prices, on average, as measured by the general price index. An increase in the relative price of an asset leads to a positive real holding gain and a decrease in the relative price of an asset leads to a negative real gain, whether the general price level is rising, falling or stationary.

Of course we should consider holding gains and losses on liabilities as well.

This is anyway complicated practically. I haven’t yet seen national accounts of any country producing such tables. But the SNA—including the 2008 SNA—doesn’t have any framework beyond this. This is because it considers that economic behaviour would be different for real holding gains or losses, as opposed to just the flow aspect.

In other words, if your (nominal) income is $100 and there’s a 10% inflation, your consumption would fall. But you might not react the same if you have a real holding loss of $10.

But to a first approximation you could simplify and bring real holding gains into real income. I have simplified quite a bit and these are quite challenging things, so I refer you to Wynne Godley and Marc Lavoie’s (G&L)’s book Monetary Economics.

I wrote this post after an online discussion about the government “inflating away the nominal debt”. Although such claims are loaded, there is some logic to it. In inflation accounting, holding gains/losses appear in incomes. Modeling involves going back and forth between real and nominal variables.

An original writing is that of Wynne Godley (and Ken Coutts and Graham Gudgin)—a 1985 paper titled Inflation Accounting Of Whole Economic Systems. In that you see the equation:

So the government disposable income (in addition to taxes and central bank profits, also has the holding losses due to the fact that prices of goods and services has increased in the period, not just because of changes in prices of government bonds).

Of course, there’s also the loadedness of the phrase “inflating away the debt”. That’s a different matter, my point here is to address the intuition of why inflation can be thought of as bringing revenue to the government and reducing its debt.

James Tobin pioneered the stock-flow consistent modeling. He won the Nobel Prize for it. You can find his Nobel lecture Money And Finance In The Macroeconomic Processhere.

Although quite brilliant, there are many shortcomings in James Tobin’s approach. The genius of Wynne’s approach was to overcome those.

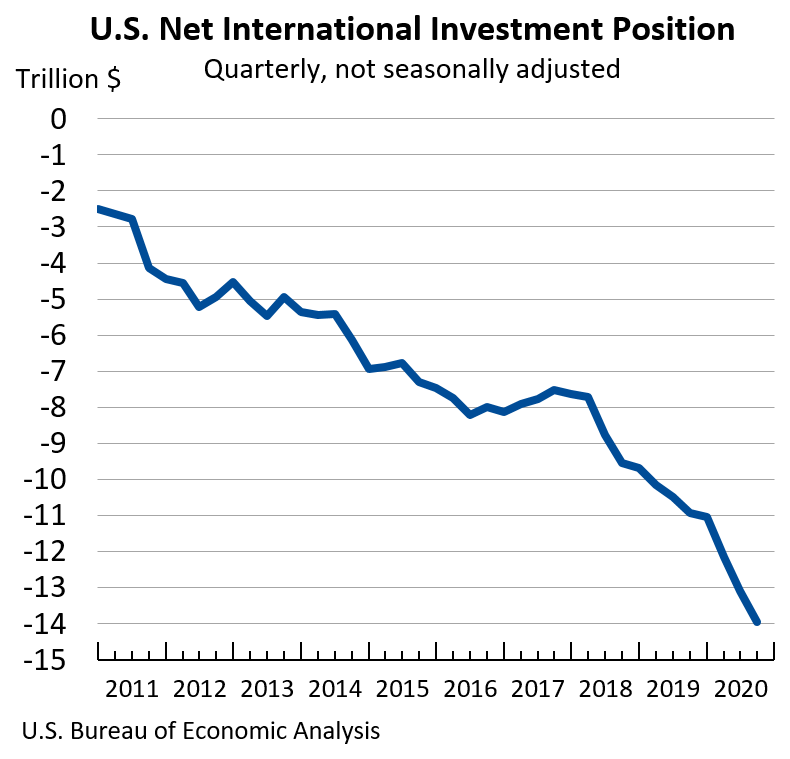

Although the release is more than a month old, I missed the release. The US international investment position is worsening and in unsustainable territory.

Chart from the BEA release dated 29 December, 2020, with last data point from Q3, 2020:

It’s not plotted relative to gdp, but work that out in your head 😉

Wynne Godley’s analysis before 2008 was simple: the US private sector balance—the difference between private expenditure and private income—was negative continuously and was unsustainable. The reversal—private expenditure falling relative to private income—would lead to a large crisis. And meanwhile the US trade was also weak and a large fiscal stimulus would be needed but because of international trade, the fiscal multiplier won’t be large enough and the recovery would be weak. His papers also forecast rising negative net international position mirrored by large rise in public debt relative to gdp, so to keep a sustainable configuration, the US government should directly address international trade, or else face slow growth.

… financial balances (relative to income flows) must stay within certain limits if debts are not to grow excessively, implying that the monitoring of these balances may yield a warning that unsustainable processes are at work.

Also, the “investment income” in balance of payments—the flows—stays positive. A lots has been written on it but on the question of sustainability it’s not too important in my view, although of course, once it turns negative it accelerates the already unsustainable position.

Jan Hatzius of Goldman Sachs talks about how he drew inspiration from Wynne Godley in the latest Odd Lots podcast hosted by Joe Weisenthal and Tracy Alloway of Bloomberg.

He talks of how the private sector financial balance (or net lending) is an important thing to look at to predict crisis.

Wynne Godley in a 1988 article, The Sensibility Of Contemporary Institutions in Theology, (first given as a Sermon before the University in King’s College Chapel, 31 May 1987:

Recourse to the dictionary gives, among the definitions of the word sensibility, ‘the glad or sorrowful recognition of a fact or a condition of things’. Also, ‘readiness to feel compassion for suffering’.

…

But the major issues at stake have been vastly more important than ones which concern sensibility narrowly defined. They go beyond who becomes rich and who remains poor. They extend to matters such as slavery, mass unemployment and civil war.

…

… The IMF would do well to reperuse its own Article I, which .lists among its purposes: ‘to facilitate the expansion and balanced growth of international trade, and to contribute thereby to the promotion and maintenance of high levels of employment and real income and to the development of the productive resources of all members as primary objectives of economic policy … ‘ In this passage you hear the authentic note of optimism and mutual concern which informed economic relationships within and between countries in the first twenty-five years after the war.

I have been forced to recognize with sadness and very great disappointment that I have so far failed in my personal endeavour to change the course of events or the attitudes of other people. But I remain steadfast to what I understand to be the meaning of Christianity: the unique value it places on the individual inner life; the ability to tolerate aloneness and the imminence of death; the joyful and sensitive concern for and love of other human beings.

From Alan Shipman’s biography, Wynne Godley, A Biography, Chapter 9: Balance Of Payments, Deindustrialisation And Protection, page 151:

Of all Godley’s policy prescriptions, direct import controls were the one most roundly rejected by other economists, and least likely to be adopted by politicians with any chance of gaining power. The accusation of advocating a policy that was economically illogical, politically infeasible and inadmissible in international law hurt deeply, but never crushed his belief that import quotas should be seriously considered as an additional macroeconomic instrument. The depth of the wound emerged in an unusually personal statement to a 1978 conference on ‘Slow Growth in Britain’, convened by Oxford University’s Wilfred Beckerman in Bath. ‘I am disconcerted and distressed to find myself, together with the group of people with whom I work in Cambridge, in such an isolated position. For we seem to be the only group of professional economists who entertain the possibility that control of international trade may be the only way of recovering and maintaining the prosperity of this country; that free trade may be an enemy for the relatively weak’ (Godley 1979: 226).

…

References

…

Godley, W. (1979). Britain’s chronic recession—Can anything be done? In W. Beckerman (Ed.), Slow Growth in Britain. Oxford: Clarendon Press.

A study of the history of opinion is a necessary preliminary to the emancipation of the mind.

Although in the poor countries, ones colonised and which suffered because of imposition of laissez-faire, there have been a lot of opposition to free trade—and those voices aren’t heard through silencing internationally—in the advanced countries, it has been almost non-existent except from Cambridge Keynesians and maybe a few others. In recent times, we see some opposition, but not remotely like this even 40 years ago. It is important to know the history of thought to understand how hegemonic the ruling ideology has been.

For Wynne Godley, dissenting against free trade was one of the most important reasons for his dissent against the profession. In his short autobiography written in 2001 for A Biographical Dictionary Of Dissenting Economists, Godley said:

There are two aspects (in particular) of the work of the CEPG [Cambridge Economic Policy Group] which put its members into a category which may he termed ‘dissenting’. The first – a matter mainly of concern to the modelling fraternity and academic econometricians – was the unconventional view we took about how to construct and use an econometric model.

…

The second, and more egregious, respect in which we became a ‘dissident’ group was that, as a result of trying to think through the possible ways in which Britain’s net export demand might be improved, we entertained the possibility that international trade should be, in some sense, ‘managed’. There might, we argued, be no way in which the adverse trends could be reversed other than some form of control of imports. Our argument (see for instance Cripps, 1978; Cripps and Godley, 1978) was never one in favour of protectionism as normally understood – that is, the selective and unilateral protection of relatively failing industries under conditions of general stagnation. On the contrary, we were most careful to lay down conditions under which the management of trade would benefit not only our own country (without making its industry less efficient) but would also increase the level of trade and output in the rest of the world. The two basic principles were, first, that trade management should reduce import propensities without ever reducing imports themselves (in total) below what they otherwise would have been; and, second, that ‘protection’ should be as minimally selective as possible (for example, through the use of market mechanisms such as auction quotas) so that industrial inefficiency would not be sponsored.

I was surprised by the hostility with which our ideas about trade were received. It seemed to me at the time, and still seems to me, that the arguments actually used against us (at their most coherent by Maurice Scott et al., 1980) did not, in practice, rest on a well-articulated theoretical position but on very special assumptions about behavioural relationships and international political responses. (I have, to the best of my ability, answered these particular points in Christodoulakis and Godley, 1987.)

…

The ‘dissident’ argument in favour of managed trade is well summarized in Kaldor (1980), where he points out that the modern theory of international trade is based on the assumption that all production takes place according to the conditions described by the neoclassical production function, with constant returns to scale. Kaldor postulated instead, and he was surely right to do so, that the principle of circular and cumulative causation leads (through dynamically increasing returns) to a process, not of convergence, but of polarization between successful and unsuccessful economies in which success in competitive performance feeds on itself and losers become immiserated by trade.

…

Godley’s Major Writings

…

(1978), ‘Control of Imports as a Means to Full Employment: The UK’s Case’ (with T.F. Cripps), Cambridge Journal of Economics, 2, September.

…

(1987), ‘A Dynamic Model for the Analysis of Trade Policy Options’ (with N. Christodoulakis), Journal of Policy Modelling, 9.

…

Other References

Cripps, T.F. (1978), ‘Causes of Growth and Recession in World Trade’, Cambridge Economic Policy Review, No. 4.

Kaldor, N. (1980), ‘The Foundations of Free Trade Theory and Recent Experiences’, in E. Malinvaud and Fitoussi, J.P. (eds), Unemployment in Western Countries, London: Macmillan.

…

Scott, M., Corden, W.M. and Little, I.M.D. (1980), The Case Against Import Controls (Thames Essay No. 24), London: Trade Policy Research Centre.