Marc Lavoie has a new paperMMT, Sovereign Currencies And The Eurozone. It’s based on a lecture he was asked to give in 2021 STOREP conference. In this he analyses what neochartalism (“MMT”) is and what is says about the Euro Area.

Marc Lavoie also discusses Sergio Cesaratto’s work. Sergio had an excellent bookHeterodox Challenges In Economics: Theoretical Issues And The Crisis Of The Eurozone and I somehow missed Marc’s review of it earlier.

My view on these issues—with good grasp of the institutional details—is that countries face a balance-of-payments constraint and the way the Euro Area is set up makes the balance-of-payments constraint stronger. Euro Area countries can no longer devalue their currencies (or hope their currencies depreciate by market forces) and the government can’t make overdrafts on their central banks.

It’s true that the European Central Bank (ECB) can buy government bonds but that it can doesn’t mean it actually will do to the extent needed. Indeed, the ECB has also pushed for tightening of fiscal policy using its powers. Countries face a BOP problem because like in other institutional setups, they’re at the mercy of foreigners. In fact more it’s more than otherwise in case of the Euro Area. And international indebtedness ultimately falls on the shoulders of the governments and hence we saw crisis in the government bond markets.

Countries with a strong international investment position such as Germany do not face this problem.

Ultimately, the problem is that the Euro Area doesn’t have a central government which would be involved in large fiscal transfers and keeping imbalances between countries in check. But as Sergio Cesaratto argues, it was never meant to be that way as the founders of the Euro Area designed it in a way to take away powers from national governments.

I should add one question which arises: the question about the political role of the ECB, which is similar to the role of governments in other places such as the US. There seems to be an inconsistency in the position of people such as Sergio (and I) that we treat the ECB and the US government differently. We say that the US government should be involved in more fiscal stimulus but don’t exactly say that the problems of the Euro Area can be resolved by proposing that the ECB promises to purchase government bonds without limits.

The answer to that is: even outside the Euro Area, rich countries’ central banks can bail out poor countries facing balance-of-payments financing problems. Does that mean that countries outside the Euro Area don’t face a bop-constraint??

It’s a rhetorical question posed as an answer.

Ultimately the balance-of-payments problems in the Euro Area is more severe than otherwise.

Where does neochartalism (“MMT” or “M.M.T.”) fit in my description? The idea that Euro Area governments cannot make overdrafts at their national central banks (NCBs) is something stressed by neochartalists is right but many authors who didn’t call themselves MMTers stressed this such as Wynne Godley in 1992. The idea that current account deficits don’t matter isn’t useful as you still have to explain why Germany didn’t go into a crisis like Greece.

Mario Draghi is set to become the next Prime Minister of Italy!

From a recent interview with Sergio Cesaratto at Brave New Europe:

Will he be able to do it?

Draghi is a many-headed dragon. He is a Catholic socio-conservative. Somehow a Christian Democrat able to please almost everybody – German friends know what I mean. This is his real skill, which he has shown in running the ECB by skilfully keeping the German representatives’ hardliners at bay. Consensus is important. And he will need a heavy German endorsement (and not all Germans like him). Many in Italy fear his conservative facade. Draghi has been many things: the wretched privatiser of Italian public industry just before he went to work for Goldman Sachs; he declared that the European welfare state had had its day; but in 2014 he made it clear that Europe’s anti-Keynesian economic policy was wrong. There is something for everyone! In his tesi di laurea he even argued that the euro was a bad idea! Let’s remember, however, that in 2023 Italy must hold new elections, and although Renzi (who is a former Christian Democrat) shares Draghi’s Christian social-conservative visions (more CSU than CDU), he is unlikely to have the capacity to create a political background for him. Certainly Renzi might have had something like this in mind (recall that he comes from Tuscany, the land of Machiavelli!).

Introduces readers to the basics of heterodox and orthodox approaches in economics

Explains the problematic aspects of the European Monetary Union (EMU) from the standpoint of alternative economic theories

Highlights the conservative nature of the EMU and the economic and political difficulties of reforming it

with the further description:

This book discloses the economic foundations of European fiscal and monetary policies by introducing readers to an array of alternative approaches in economics. It presents various heterodox theories put forward by classical economists, Marx, Sraffa and Keynes, as a coherent challenge to neo-classical theory. The book underscores and critically assesses the analytical inconsistencies of European economic policy and the conservative nature of the current European governance. In this light, it examines the political obstacles to proposals to reform the European monetary union, as well as those originating in the neo-mercantilist German model. Given its scope and format, the book offers a valuable asset for researchers and members of the general public alike.

In short, [we hear] Greece has made it, finally we are changing Europe. Unfortunately, this is not the case and such announcements seem to be news similar to Saddam´s journalists who proclaimed victory while American tanks rolled into Baghdad.

I recently referred to a paper by Sergio Cesaratto on the Euro Area crisis. There is another paper, Alternative Interpretations Of A Stateless Currency Crisis, written for the Cambridge Journal Of Economics, written last year which I somehow missed referring on this site.

CJE link (no paywall at the time of writing), Wayback Machinelink.

Abstract:

A number of economists warned that a political union was a prerequisite for a viable currency union. This paper disputes the feasibility of such a political union. A fully fledged federal union, which would likely please peripheral Europe, is impracticable since it implies a degree of fiscal solidarity that does not exist. A Hayekian minimal federal state, which would appeal to core Europe, would be refused by peripheral members, since residual fiscal sovereignty would be surrendered without any clear positive economic and social return. Even an intermediate solution based on coordinated Keynesian policies would be unfeasible, since it would be at odds with German ‘monetary mercantilism’. The euro area is thus trapped between equally unfeasible political perspectives. In this bleak context, austerity policies are mainly explained by the necessity to readdress the euro area balance-of-payments crisis. This crisis presents striking similarities to traditional financial crises in emerging economies associated with fixed exchange regimes. Therefore, the delayed response of the European Central Bank (ECB) to the sovereign debt crisis cannot be seen as the culprit of the euro area crisis. The ECB’s monetary refinancing mechanisms, Target 2 and the ECB’s belated Outright Monetary Transactions intervention impeded a blow-up of the currency union, but could not solve its deep causes. The current combination of austerity policies and moderate ECB intervention aims to rebalance intra-eurozone foreign accounts and to force competitive deflation strategy.

As the abstract says, the ECB alone cannot resolve the crisis.

I agree almost everything in the paper except that in my opinion, a political union—a central government—is the only way to solve the Euro crisis. But Sergio’s arguments about his view are solid.

Recently I commented on a paper, The Financial Crisis In The Eurozone: A Balance-Of-Payments Crisis With A Single Currency? by Eladio Febrero, Jorge Uxó and Fernando Bermejo, published in ROKE, Review Of Keynesian Economics. I hadn’t realised that Sergio Cesaratto has a reply (paywalled) in the same issue.

Sergio Cesaratto. Picture credit: La Città Futura, Sergio Cesaratto

Abstract:

Febrero et al. (2018) criticise the balance-of-payments (BoP) view of the European Economic and Monetary Union (EMU) crisis. I have no major objections to most of the single aspects of the crisis pointed out by these authors, except that they appear to underline specific sides of the EMU crisis, while missing a unifying and realistic explanation. Specific semi-automatic mechanisms differentiate a BoP crisis in a currency union from a traditional one. Unfortunately, these mechanisms give Febrero et al. the illusion that a BoP crisis in a currency union is impossible. My conclusion is that an interpretation of the eurozone’s troubles as a BoP crisis provides a more consistent framework. The debate has some relevance for the policy prescriptions to solve the eurocrisis. Given the costs that all sides would incur if the currency union were to break up, austerity policies are still seen by European politicians as a tolerable price to pay to keep foreign imbalances at bay – with the sweetener of some European Central Bank (ECB) support, for as long as Berlin allows the ECB to provide it.

Sergio carefully responds to all views of Febrero et al. and Marc Lavoie, Randall Wray and also Paul De Grauwe, pointing out that he agrees with most of their views except that their dismissal of this being a balance-of-payments crisis with their claims that the problem could have been addressed by the Eurosystem/ECB lending to governments without limits. He points out that, “The austerity measures that accompanied the ECB’s more proactive stance are clearly to police a moral hazard problem”. It is true that the ECB, the European Commission and the IMF overdid the austerity but it doesn’t mean that Sergio’s opponents’ claims are accurate.

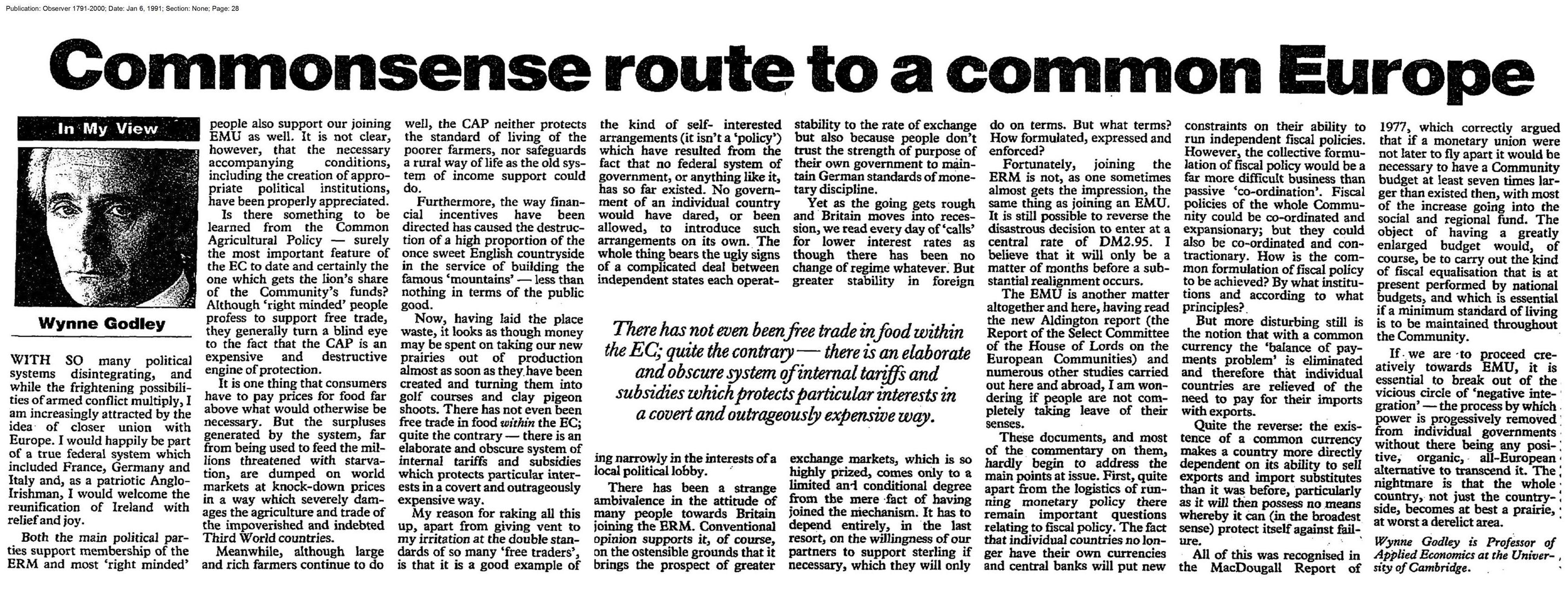

… But more disturbing still is the notion that with a common currency the ‘balance or payments problem’ is eliminated and therefore that individual countries are relieved of the need to pay for their imports with exports.

Quite the reverse: the existence or a common currency makes a country more directly dependent on its ability to sell exports and import substitutes than it was before, particularly as it will then possess no means whereby it can (in the broadest sense) protect itself against failure.

– Wynne Godley, Commonsense Route To A Common Europe, inThe Observer, 6 January 1991.

Greece had large negative current account balance of payments and Germany had the opposite over the lifetime of the Euro.

Yet, there are some economists who argue that the Euro Area crisis is not a balance of payment crisis. Of course there are other aspects to the crisis as well but this in my view is the main issue. There was a debate between Sergio Cesaratto and Marc Lavoie on this. Now there is a new paper in the most recent issue of ROKE (Review of Keynesian Economics) by Eladio Febrero, Jorge Uxó and Fernando Bermejo which discusses this. The Wayback Machine/Internet Archive link is here if you are reading it after the journal puts the paywall again.

The authors seem to be against Sergio Cesaratto view. Since I agree with Cesaratto, I thought I should comment on it.

The fundamental problem of the Euro Area is that it doesn’t have a central government. If there had been a central government like the US federal government, with large fiscal powers, the Euro Area crisis would have been far less deeper. This is because weaker regions would have been recipients of “fiscal transfers”, i.e., receive more government expenditure than what they send in taxes.

Fiscal transfers can be seen transactions in the balance of payments of Euro Area countries if the EA had a central government. The way to do balance of payments for monetary and political unions is explained in the IMF Balance of Payments and International Investment Position manual. Take a country like Greece. The Euro Area government would be considered external to Greece. Same for other countries. But for the Euro Area as a whole, the central government would be considered inside the Euro Area.

So government expenditure would appear in Greek exports in the goods and services account and transfers in the secondary income account. Taxes would appear only in the latter.

So there is an improvement in the current account balance of payments for regions compared to the case when there is no central government. Current account balances accumulate to the net international investment of the whole country. A country which has persistent imbalances would have negative net international investment position, i.e., indebtedness to other countries.

So fiscal transfers keep all this in check by improving the current account balance. So if the Euro Area had a central government, debts of a country like Greece would be in check.

By joining the half-baked half-way house, Greece got an overvalued exchange rate and easier access for other Euro Area countries into its markets and its external imbalances worsened in its lifetime inside the monetary union.

Nations with high current account deficits will also have higher public debt than otherwise and would need international investors to buy the debt which residents won’t. Normally the price would adjust to bring international investors but as we have seen, sometimes there is no price and a fall in bond prices might lead to expectations of further fall leading external investors to dump the bonds instead of finding them attractive.

The trouble with Febrero et al. is that they seem to think that the European central bank can purchase all government debt of nation. Certainly, the European Central Bank (ECB) has stepped in at various times to ease the pressure on government bond markets. But the trouble with this is that there are under some conditions such as assuming it can impose tight fiscal policy on the governments it is helping.

If the Euro Area treaty is modified to allow countries to have independent fiscal policies, then for stability, the ECB has to buy bonds without limits and can keep accumulating. It is a political mess. A country like Germany could argue that it is writing an open cheque to Greece.

A political union wouldn’t have such problems. National level governments such as the Greek government would have fiscal rules on them, and hopefully not the supranational government. This is like the United States where state governments have rules on their budgets.

In contrast, if the ECB guarantees Greece’s debt, it has to impose some rules and since Greece is not recipient of any equalisation payments—the fiscal transfers—its performance is still dependent on its competitiveness. This is because competitiveness would affect the Greece government’s fiscal balance and hence put a deflationary pressure on Greece’s fiscal stance.

On the other hand, a Euro Area with a central government would imply Greece is recipient of substantial equalisation payments and its competitiveness isn’t so binding.

An argument of the economists arguing that the European monetary system has this thing called TARGET2 and that the intra-Eurosystem balances (i.e., automatic credits offered by one national central bank to another) can rise without limit is used in this paper. This is highly misleading. It is true but one should look at the changes in debits and credits elsewhere. Suppose a country like Greece sees a large private financial outflow. While T2 can absorb a lot of this—much more than anyone imagined—in the late stages, Greece banks become heavily indebted to their national central bank, The Bank of Greece. When they run out of collateral, the rules under ELA, Emergency Liquidity Assistance, is triggered. So TARGET2 or more accurately the Eurosystem cannot absorb everything.

In summary, the Euro Area cannot do without a central government in the long run. Anyone who thinks that the ECB or the Eurosystem can buy whatever residual debt private investors doesn’t understand that in such a system, Euro Area governments are given an open cheque.

The difference between not having a central government and a central government is that in the former, there is no equivalent income flow as in the latter. The Eurosystem purchases would affect the financial account of balance of payments, not the current account.

One of the noticeable assertions of the paper is:

With T2, there is just one currency. This means that if foreign exchange markets did not exist, there could not be a BoP crisis, so that the cause of the crisis should be found elsewhere.

The trouble with this is that it sees it only as a currency crisis. But the fact is that countries whose external position were weak were the ones running into trouble in the Euro Area. Had current account deficits not blown up, countries would have had better fiscal balance since the current account balance and the budget balance are related by an identity and even behaviourally as can be seen in stock-flow consistent models. In crisis times, foreign investors are more likely to shift their funds in their home countries. With better balance of payments, public debt would be held more internally and there would have been less pressure on government bonds.

There are comments in the paper about too much credit etc. This is true, but then the Euro Area crisis would have looked more like the economic and financial crisis affected the United States.

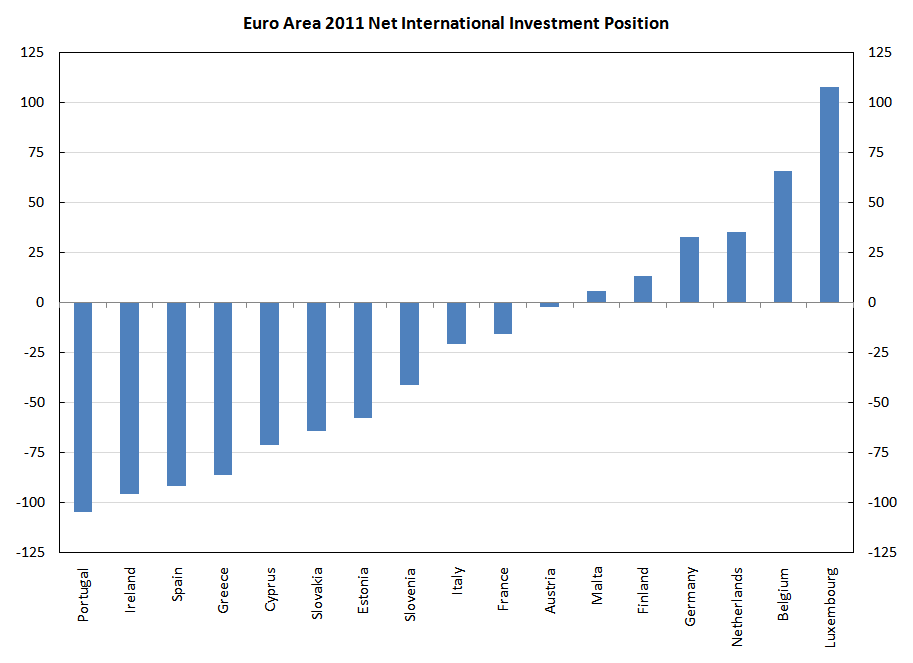

Here’s the the NIIP of Euro Area countries in 2011.

Doesn’t this explain why Germany was in a better position than Greece when the crisis started heating up? Or that Netherlands was in a better position than Portugal?

Sergio Cesaratto has posted a reply on Matias Vernengo’s blog, replying to a paper by Marc Lavoie on economic problems of the Euro Area

For previous discussions, see the citations in that post or see my previous post on this.

Marc’s point is that because TARGET2 allows unlimited and uncollateralized credit/debit facilities between Euro Area NCBs and the ECB, the troubles facing the Euro Area are not balance-of-payments in origin.

As mentioned earlier, this however is not the thing to look at. One should look at counterparts to the intra-ESCB (TARGET2) debts. Intraday overdrafts, marginal lending facility, MRO, LTRO, ELA … none of these can rise without limit. At some point, a crisis occurs and foreigners’ help is needed.

Greece, Portugal, Ireland, Spain, Cyprus all have high negative net international investment positions. No wonder these nations have seen the most troubles.

I echo Sergio’s example (on Calabria) with a similar example of my own. If nations in a monetary union cannot face a balance-of-payments crisis, why not have the whole world join the Euro Area and adopt the Euro as their currency and have the ECB as the central bank of the world and guarantee all government debts without any condition? Surely, that should be the solution to the problems of the world! Not!

Surely austerity has been high and the ECB can help to keep government bond yields in check and allow for expansionary fiscal policies. It had its “OMT”, which has never been used as the annoucement effect itself has kept government bond yields low. But Greece has faced difficulties despite this.

The ECB alone cannot resolve the crisis. Attempts to boost domestic demand with fiscal policy will bring higher imbalances within the Euro Area. The Euro Area needs a central government with high powers to tax and spend. Regional imbalances will be kept in check via fiscal transfers and regional policies of the government. And the powers of the government won’t be limited with this. There are many other things such as wages which need to be coordinated at the federal level, for example. Euro Area balance-of-payments cannot be neglected.

This is a continuation of the post from the end of 2014, although reading that isn’t necessary.

In a new paper, Marc Lavoie continues his debate with Sergio Cesaratto on whether the Euro Area crisis is a balance-of-payments crisis or not. For the sake of completeness, here’s the list of papers, with references copy-pasted from Marc’s latest paper. Not all links are final versions and some may not be available to read in full).

Cesaratto, S. 2013. “The Implications of TARGET2 in the European Balance of payments Crisis and Beyond.” European Journal of Economics and Economic Policy: Intervention 10, no. 3: 359–382. link

Lavoie, M. 2015. “The Eurozone: Similarities to and Differences from Keynes’s Plan.” International Journal of Political Economy 44, no. 1 (Spring): 3–17. link

Cesaratto, S. 2015. “Balance of Payments or Monetary Sovereignty?. In Search of the EMU’s Original Sin–Comments on Marc Lavoie’s The Eurozone: Similarities to and Differences from Keynes’s Plan.” International Journal of Political Economy 44, no. 2: 142–156. link

Lavoie, M. 2015. “The Eurozone Crisis: A Balance-of-Payments Problem or a Crisis Due to a Flawed Monetary Design?” International Journal of Political Economy 44, no. 2: 157-160. (abstract)

As mentioned in my part 1, referred to on top of this post, I agree with Sergio Cesaratto.

Sergio Cesaratto with Marc Lavoie (picture credit: Matias Vernengo)

Marc Lavoie’s main point in the final paper seems to be that, “Eurozone countries can never run out of TARGET2 balances, which can take unlimited negative values, so that the evolution of the balance of payments cannot be the source of the crisis”.

This is not accurate in my view. Although the rules of the Eurosystem allow unlimited and uncollateralized credit facility between the Euro Area NCBs and the ECB, one has to look at the counterpart to the T2 imbalances. If an economic unit transfers funds across border from country A to country B, this first results in a reduction of balances of banks in country A at their NCB and may result in an intraday overdraft (“daylight overdraft” in U.S. language), usage of the marginal lending facility with the NCB, an MRO, or an LTRO and finally ELA in late stages of a crisis (if capital outflow is large).

Marc himself mentions this point in his latest paper:

If a Eurozone country is running a current account deficit that banks from other Eurozone members decline to finance, or if it is subjected to capital outflows, then all that happens is that the national central bank of that country will be accumulating TARGET2 debit balances at the ECB. There is no legal limit to these debit balances. The national central bank with the debit balances, which pay interest at the target interest rate, has as a counterpart in its assets the advances that it must make to its national commercial banks at that same target interest rate. And the commercial banks can obtain central bank advances as long as they show proper collateral. Why would the size of current account deficits or TARGET2 debit balances worry speculators? There might be a problem with the quality of the loans that have been granted by the banks, or with the size of the government debt, but that as such has nothing directly to do with a balance-of-payments problem.

[italics: mine]

But that is the case! It’s because of balance-of-payments. Nations who had high indebtedness to the rest of the Euro Area saw more capital flight. This is because in times of crisis, there is a home bias and international investors are likely to sell securities abroad and repatriate funds home. Large current account imbalances lead to a large negative net international investment position. (It’s of course also true that revaluations are important, and this is what happened in the case of Ireland). So when non-residents sell securities to domestic investors, banks are likely to get into a bad situation because they have to accommodate these transfer of funds and are losing central bank balances on a large scale.

It is precisely nations which had worse net international investment positions which were affected as charted in my previous post on this.

Now moving on to definitions: what is a balance-of-payments problem? The simplest definition is the problem for residents in obtaining finance from non-residents. Greece precisely has been struggling to obtain funds from non-residents.

So I do not agree with Marc’s view that:

Cesaratto, as others, is adamant that the Eurozone crisis is a balance-of-payments crisis, whereas I believe, as others do, that this is a side issue.

Marc Lavoie also says that the people arguing for this view are implicitly assuming some kind of “excess saving” view on all this:

In discussions with colleagues who support a “current account deficit” view of the Eurozone crisis, I sometimes get the impression that they are also endorsing a kind of “excess saving” view of the economy. They tell me that current accounts deficits are unsustainable within the Eurozone because the core Eurozone countries will refuse to lend to the periphery and will thus prevent these countries from financing economic activity. This seems wrong to me.

I disagree with this. It’s precisely because residents’ liabilities are large compared to their financial assets that they have to rely on non-residents/foreigners. And during the crisis a lot of capital outflow has happened and this precisely shows that non-resident private investors are unwilling to lend again on the same scale as before. This obviously means that to obtain finance, governments of nations affected have to take the help of the official sector abroad, such as from governments, the ECB and the IMF. If TARGET2 alone could do the trick, is the Greek government foolish to go abroad?

It is of course true that the design of the Euro Area was faulty. But that still leaves open the question about why Germany is not facing a crisis as severe as Greece. The design view cannot explain this. Any country (or all countries) in the Euro Area could have faced a crisis. There is a pattern here and that is where balance-of-payments comes in.

This debate is an interesting one. Both Sergio Cesaratto and Marc Lavoie agree on almost everything, except this BIG thing.

Of course this also spills over to policy proposals. Marc Lavoie believes that the European Central Bank can guarantee that all nations can have independent fiscal policies (by promising to buy all government debt which the financial markets isn’t interested in purchasing). Sergio Cesaratto is clear on this (and I agree very much) – in another paper Alternative Interpretation of a Stateless Currency Crisis:

A more resolute role of the ECB as lender of last resort accompanied by fine-tuned expansionary fiscal policies can only be imagined in a different political and institutional framework, quite close to that of a political union.

Let’s consider what happens if there is no federal government and if the ECB is the main supranational authority (ignoring other supranational institutions which have limited powers). Suppose the ECB were to guarantee the debt of governments of all Euro Area nations. There’s nothing to prevent, say, the government of Finland to increase the compensation of its employees every year by a huge percentage and thereby affecting Finnish corporations’ compensation of its employees. This will result in a reduction of competitiveness of Finnish producers and Finnish resident economic units will rely more on goods and services produced abroad. This will raise Finland’s net indebtedness to the rest of the Euro Area and the world. If someone believes that this debt is not a problem, how about the inflationary impact of this rise in demand on the rest of the Euro Area?

So the solution lies in bringing down the balance-of-payments imbalances (both negative and positive ones such as that of Germany). This requires a supranational institution, which is a central government. National governments would have rules on their budgets but the central government — since its goals and objectives are different — wouldn’t be bound by any rules. Wage rises would need to be coordinated. And as I argue in this post, fiscal transfers also plays a role of keeping imbalances in check.

Of course there are many other economists who also argue that the Euro Area problem is a balance-of-payments problem, but with a different motive. Their argument is to blame the nations in crisis instead of taking a humanist approach.

To summarize, the Euro Area problem wouldn’t have been a balance-of-payments problem had the official sector promised to act as a lender of the last resort to national Euro Area governments without any condition. As long as there are conditions, it is a balance-of-payments problem. One cannot pretend that the European Central Bank has or can be given such powers to lend without any condition. And hence the Euro Area crisis is a balance-of-payments problem.

Sergio Cesaratto has a new paper Balance Of Payments Or Monetary Sovereignty? In Search Of The EMU’s Original Sin – A Reply To Lavoie. (html link, pdf link)

I obviously agree with Sergio Cesaratto.

As long as there is no supranational fiscal authority, a Euro Area nation’s economic success is more restricted by its exports than otherwise as there is no mechanism for fiscal transfers. The European Central bank can of course backstop and to some extent it has done so, but it cannot let fiscal policy of nations become independent of balance of payments beyond a certain extent. If it does so, nations’ public debt will rise together with net indebtedness to foreigners relative to output and this will become unsustainable. The European Central Bank (the Eurosystem less the domestic National Central Bank) will become a huge creditor and this will not be acceptable to the rest of the Euro Area. (There is of course the question whether this would be morally right but I do not think it is immoral beyond a limit).

To some extent, Mario Draghi has acted the opposite and pushed austerity, but one cannot assume unlimited power for the ECB (Eurosystem to be precise).

The other way to check that it is indeed a balance-of-payments crisis is to simply see the net international investment position of nations. This chart is from 2011 (intentionally chosen to be old).

The nations troubled most had huge net indebtedness to foreigners. If it is not a balance-of-payments crisis, how does one explain that countries such Germany and Luxembourg had far less troubles than Greece and Portugal?

Abstract of the paper:

In a recent paper Marc Lavoie (2014) has criticized my interpretation of the Eurozone (EZ) crisis as a balance of payments crisis (BoP view for short). He rather identified the original sin “in the setup and self-imposed constraint of the European Central Bank”. This is defined here as the monetary sovereignty view. This view belongs to a more general view that see the source of the EZ troubles in its imperfect institutional design. According to the (prevailing) BoP view, supported with different shades by a variety of economists from the conservative Sinn to the progressive Frenkel, the original sin is in the current account (CA) imbalances brought about by the abandonment of exchange rate adjustments and in the inducement to peripheral countries to get indebted with core countries. An increasing number of economists would add the German neo-mercantilist policies as an aggravating factor. While the BoP crisis appears as a fact, a better institutional design would perhaps have avoided the worse aspects of the current crisis and permitted a more effective action by the ECB. Leaving aside the political unfeasibility of a more progressive institutional set up, it is doubtful that this would fix the structural unbalances exacerbated by the euro. Be this as it may, one can, of course, blame the flawed institutional set up and the lack an ultimate action by the ECB as the culprit of the crisis, as Lavoie seems to argue. Yet, since this institutional set up is not there, the EZ crisis manifests itself as a balance of payment crisis.

Excerpt from the conclusion:

… To conclude, since the EZ is closer to a fixed exchange rate regime rather than to a viable, U.S.-style CU, the euro-crisis is akin to a classical BoP crisis. True, the existence of T2 and the possibility of some ECB backing to troubled local sovereign debts make some difference. However, the limits to an ultimate action by the ECB in connection to the absence of other institutions that compose a viable CU render its action necessarily restricted. One can, of course, blame the lack of these institutions and of an ultimate action by the ECB as the culprit of the crisis, as Lavoie and De Grauwe seem to maintain. Yet, since those institutions are not there, the EZ crisis manifests itself as a balance of payment crisis …

Finally, remember the balance-of-payments constraint manifests itself as lower domestic demand and output as much as financial crises.

In general — in other institutional setups, the importance of the government’s power to make drafts at its central bank is exaggerated. It is highly important of course, but problems of balance-of-payments restrain the power of governments in having a fiscal policy independent of what is happening in international trade. In the Euro Area, the lack of critique of the “Common Market” is striking. One can however see these discussions in the works of Nicholas Kaldor.

Unlimited TARGET2 power?

An important point in the current discussion is around the issue of limits of TARGET2. It is true that the TARGET2 system has large powers to absorb imbalances. The intra-Eurosystem debts need not be collateralized. However, when there is capital flight from a nation, banks become more indebted to their NCB. This process can go on for a long time but ultimately it is restricted by collateral banks can provide to their NCB for replenishing lost settlement balances. There is of course the ELA, Emergency Loan Assistance, but this too is limited beyond a point. There is a lot of politics involved here with some nations complaining unfairly on debtor nations’ use of the ELA, but beyond a certain point, their complaints may be fair.

To summarize, TARGET2 is a big shock absorber: beyond what any economist may have expected, but it cannot absorb shocks beyond a limit.

{kind=link}