In two recent posts, I had mentioned how economists are shifting their positions because of politics:

- Opposing Principles Of Political Economy Just Because Donald Trump Supports It,

- The Soon-To-Be Conventional Wisdom: “Fiscal Policy Is Not So Good”.

Thanks to Kevin Glass on Twitter, I came across two headlines highlighting this.

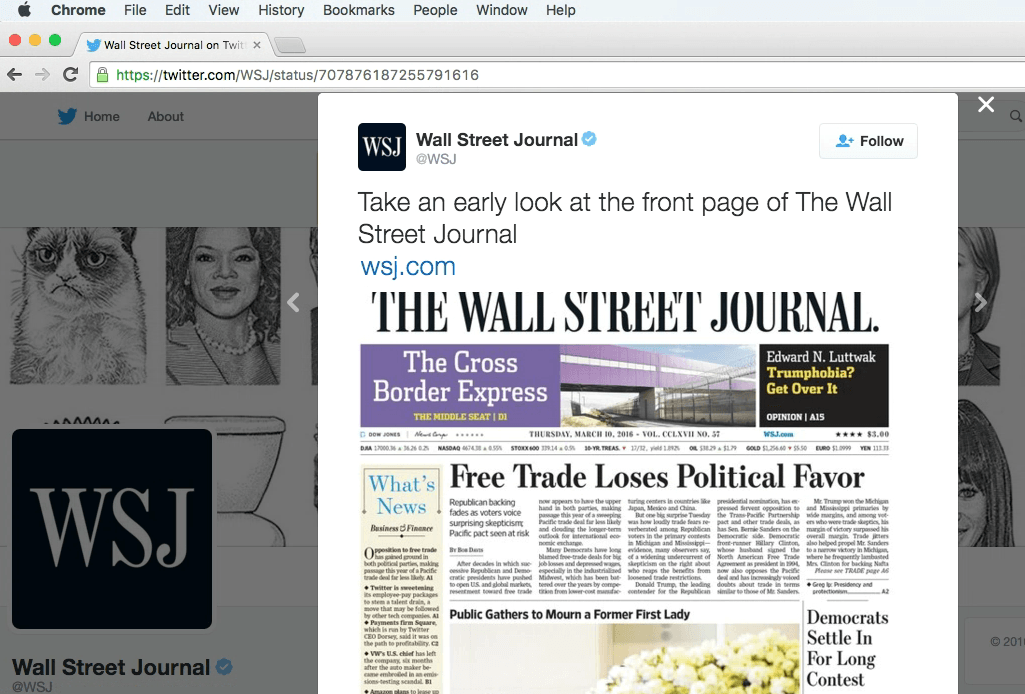

Headline 1, post-election (click for the link)

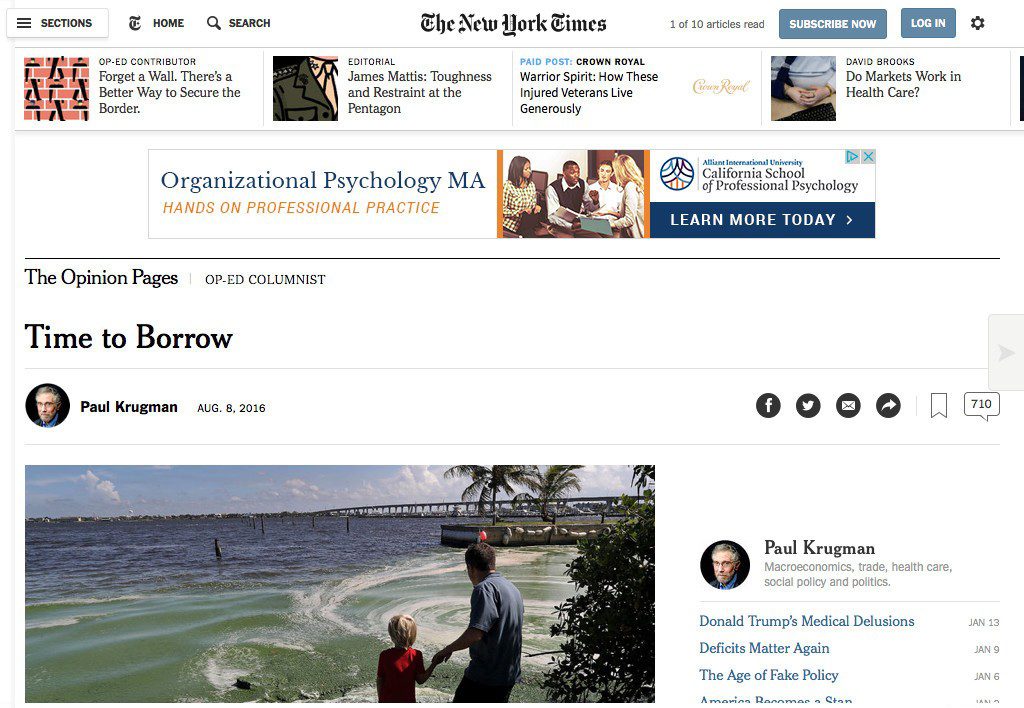

Headline 2, pre-election (click for the link)

I am sure an apologist would go, “Can you read beyond the headline?”. Well, yes and the two articles mean precisely what the headlines imply.

Krugman says,

This diagnosis — shared by most professional economists — didn’t come out of thin air; it was based on well-established macroeconomic principles. Furthermore, the predictions that came out of those principles held up very well. In the depressed economy that prevailed for years after the financial crisis, government borrowing didn’t drive up interest rates, money creation by the Fed didn’t cause inflation, and nations that tried to slash budget deficits experienced severe recessions.

…

What changes once we’re close to full employment? Basically, government borrowing once again competes with the private sector for a limited amount of money. This means that deficit spending no longer provides much if any economic boost, because it drives up interest rates and “crowds out” private investment.

There are several things wrong with this:

- Krugman is trying to argue that fiscal expansion makes sense only in limited scenarios

- We are not really close to full employment. There are enough people unemployed, and underemployed. Even if the US economy were close to full employment, a fiscal expansion will raise production and hence productivity via the Kaldor-Verdoorn mechanism. So it’s not like supply-side constraints are exogenously given.

- “limited amount of money” is Monetarism. Paul Krugman claims that he is no longer a follower of Milton Friedman but that’s not really the case.

- “Crowd out” is just like “patriotism is the last refuge of the scoundrel”. Krugman himself debunked it:

There is, however, a somewhat related doctrine — call it the doctrine of immaculate crowding out — which has now, I’d argued, achieved true zombiehood. That is, it keeps coming back no matter how many times you kill it.

But Krugman is not the only one. Simon Wren-Lewis is echoing him and so is Ben Bernanke.

Bernanke says:

There is still a case for fiscal policy action today, but to increase output without unduly increasing inflation the focus should be on improving productivity and aggregate supply—for example, through improved public infrastructure that makes our economy more efficient or tax reforms that promote private capital investment.

ignoring the fact that rise in production can lead to a rise in productivity.

It’s sad that all this happened. Orthodoxy needs to be fought harder.