Paul Krugman has a new article titled Wonking Out: Economic Nationalism, Biden-Style, in which he defends Biden’s economic policy which is a deviation from laissez-faire, in particular free trade.

The article has reference to a 250-page report by the White House titled Building Resilient Supply Chains, Revitalizing American Manufacturing, And Fostering Broad-Based Growth,

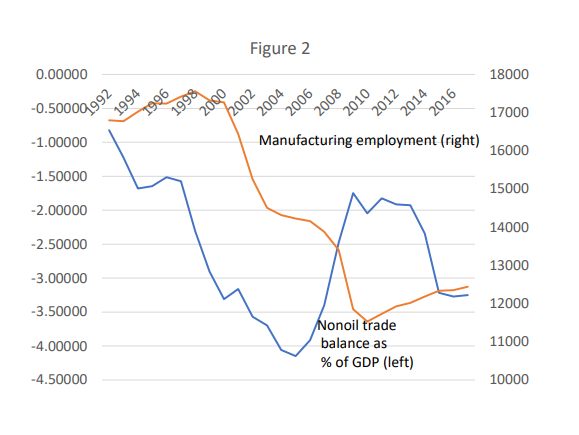

The United States’ balance of payment and international investment position is unsustainable and it needs to do something to reverse it. Weakness in international trade and offshoring have led to a lot of economic destruction which was exploited by Donald J. Trump. But the Democratic Party—led by Paul Krugman on economics—attacked Trump for deviating from free trade. But now that they are in power, they have learned a bit from their mistakes and economic realism has also taken over. Even during the Democratic Party primary election, the candidates all agreed that something has to be done on international trade and proposed policies to address it.

Elizabeth Warren, for example had a post on Medium titled A Plan For Economic Patriotism.

It’s a shame that the Democratic Party which has voters consisting of more educated people had to copy or at least follow Donald Trump.

Why is manufacturing important? Because (a) manufacturing is important to exports (b) rise in production leads to faster rise in productivity compared to other things. (c) a process of success leads to higher competitiveness of firms—not just price competitiveness but also non-price competitiveness.

The Biden administration has also not rolled back the tariffs imposed on China by Trump.

Instead, Paul Krugman has this spin:

In any case, however, we seem to be entering a new era of worries about the role of the United States in the world economy, this time driven by fears of China. And we’re hearing new calls for industrial policy. I have to admit that I’m not entirely persuaded by these calls. But the rationales for government action are a lot smarter this time around than they were in the 1980s — and, of course, immensely smarter than the economic nationalism of the Trump era, which they superficially resemble.

and:

As you might guess, then, a lot of the Biden-Harris report focuses on national security concerns. National security has always been recognized as a legitimate reason to deviate from free trade. It’s even enshrined in international agreements. Donald Trump gave the national security argument a bad name by abusing it. (Seriously, is America threatened by Canadian aluminum?) But you don’t have to be a Trumpist to worry about our dependence on Chinese rare earths.

Donald Trump is a shady person and so it’s ironic that the Democratic Party was behind. Paul Krugman in fact even spent the last 5 years or so denying that US trade is a problem. Now he is making it look like Biden and Co. are doing something original.

Many people present the recent changes as some kind of break from neoliberalism. In a sense it is but that way of presenting is misleading: finally the US policy makers are furthering US interests, which could be at the expense of the rest of the world. The United States needs policies to promote net exports—to make its international investment position sustainable—but there are various ways of doing it, such as moving to a system away from free trade or even expanding domestic demand to the point of full employment which won’t restrict total imports, and hence isn’t beggar-thy-neighbour and which is good for the whole world.

But it’s a bit like recent changes in fiscal policy: once the US is out of the woods, leaders and the academia will again go back to same old policies. So Krugman’s piece has a lot of praise for free trade which allows him to argue in the future that free trade is good. Another reason is while US deviates from free trade, politicians and pundits can continue to impose free trade on other countries. Finally the aim is to promote policies which are beneficial to oligarchies and oligarchs. Whatever works! Just like “liquidity trap” is used to argue that fiscal expansion can be done now but that neoclassical economics works otherwise, “national security” concern is used now in case of trade.

In summary, the United States needs policies to make net exports rise faster over imports, which Post-Keynesians have argued earlier than anyone, but the Democratic Party has only learned it by losing. They will try to spin this, impose more free trade on the world, while taking protectionist measures and running industrial policy themselves and create a narrative which makes it easier for them to go back to their old ideology.