The US public debt is rising $1 trillion every 100 days, headlines say. Is the US public debt sustainable?

Well, the US net international investment position is on an unsustainable path and that reflects on the US public debt. The solution is not fiscal contraction but using policy to address the US balance of payments.

According to the Federal Reserve release Z.1, the US net international investment position was −$19.37 trillion at the end of 2023. (Table B.1, line 24), while the Gross Domestic Product for 2023 was $27.36 trillion. (Table F.2, line 1).

Since government deficit is connected to the current account balance by an identity,

NL = DEF + CAB

where NL is the private sector net lending, DEF is the government deficit, CAB is the current account balance, it suggests a connection between the government deficit and current account balance not just as a static identity but behaviourally and there is a connection between the public debt and the net international investment position. In behavioural stock-flow consistent models, this can be seen more clearly.

The US has had high current account deficits and that has put the US economy on an unsustainable path.

And in general, there is no market mechanism to resolve imbalances. Lots of political discourse in the US has been around trade/tariffs etc. Industrial policy has also appeared. Note that many people define industrial policy as government picking winners, but that is misleading/a deceit. The aim of industrial policy is to improve competitiveness of a country and that has to do with exports and imports.

A lot of people complaining about the path of the US public debt seem to suggest that the way to solve it is via fiscal contraction. But that causes a deflation of the US economy and increases unemployment.

But sadly, the other side denies that there is any problem with sustainability/trade etc. So we have crazy politics. An important problem is the lack of understanding how economic forces operate. Or that people’s self-interests stand in the way of understanding.

The resolution of the problem lies in the US asking the rest of the world to increase growth by more fiscal expansion (which would increase US exports and reduce US imports relative to GDP), use protectionist measures and industrial policy and then work toward a system of planned/regulated trade where international trade is generally balanced.

In a recent interview with Larry Kudlow, Donald J. Trump has proposed a 10% tariff on all goods and services produced by nonresident economic units which he calls “a ring around the collar”.

Trump has a chance to be reelected the President of the United States and it’s noteworthy not just because of that but because there is hardly anyone proposing the same. I think that the US balance of payments and hence its financial position is in an unsustainable path and it has to take such measures.

It is important to realise that Trump was using protectionist measures in his Presidency, he faced ridicule from supposed experts. But soon when Joe Biden became the President, Biden not only continued Trump’s policy but also did more to try to improve the US’s net international investment position.

But instead of acknowledging this, the expert class obviously has its narrative. It’s partly to do with the fact that they don’t want to acknowledge that they were wrong and the rest with the fact that they want to return to the old world order of free trade once the US presumably improves its economic/financial position.

Paul Krugman has a Twitter thread and an article in The New York Times on this. It’s a tribe defense, plus a plan to keep this as it is after a small change, with the assumption that it will succeed.

In a recent blog postRevisiting The Euro Crisis, J. W. Mason argues that the current account imbalances in balance of payments isn’t a/the cause of the Euro Area crisis.

This is completely wrong!

Current account deficits have an effect on the government budget balance and a higher current account deficit would lead to a higher budget deficit than otherwise. This is not just a matter of accounting but true behaviourally. The large current account deficits ultimately caused a large public debt and investors in government debt became nervous and there was a crisis in the government bond markets of the Euro Area. Since lot of government debt is held by foreigners, as it is difficult for residents to hold all that debt (when there’s large net international indebtedness), the sale and the movement of funds abroad after the sale also resulted in a banking crisis, as banks went heavily overdraft at their NCBs and didn’t have sufficient collateral.

The crisis in banking and government bond markets caused more crisis in private debt markets and fiscal retrenchment, fall in GDP and that leading to more crisis!

As simple as that!

One of Mason’s arguments is that since lending by foreigners needn’t arise out of prior saving, the result liabilities owed to foreigners isn’t really debt. But how does it follow that one thing implies the other? If foreigners transfer a large amount of funds to accounts in their home countries, there would be a banking crisis as banks would find it difficult to post collateral to their NCB (National Central Bank). The government would have to rescue banks adding to public debt and making investors nervous.

Greek banks endogenously creating money doesn’t mean that a purchase of a German product by Greek residents doesn’t reduce Greek’s net asset position or increase its net indebtedness to Germany.

Mason says:

Many people with a Keynesian background talk about endogenous money, but fail to apply it consistently

Perhaps he is the one failing?

Take a simpler example: loans make deposits. But it’s also true that deposits are funding banks. The fact that banks created funds doesn’t imply that the created deposit isn’t a liability or debt.

Mason also discusses how the TARGET2 system works with the ECB/NCBs. The NCBs have unlimited and uncollateralised overdrafts with each other and unlike the arrangements prior the formation of the Euro Area, there isn’t an equivalent worry about central banks running out of reserves. But unlimited overdrafts for the NCBs does not imply unlimited overdrafts for the whole country! It’s just that the crisis is seen elsewhere, like in banking and the government bonds markets.

Mason also takes issue with phrases such as “capital flight”. But investors can sell assets and move funds to another country and that can put pressure on banks. How is the phrase not helpful in describing what is going on?

The problem with the Euro Area is that with exchange rates fixed irrevocably and with governments prevented from making overdrafts at their NCBs, governments cannot devalue their currency or take independent fiscal action than allowed by markets. Fixed or floating, the problem is there, and the Euro Area setup makes it worse. Doesn’t remove the problem altogether!

You can see from the data from Eurostat that Euro Area countries with the worst net international investment position were the ones seeing the worst crisis. The net international investment position is accumulated current account balance plus revaluations/holding gains/”capital gains”.

Of course, the solution of the crisis isn’t wage deflation (sometimes referred to as internal devaluation), but the formation of a central government. With the central government, there are fiscal transfers with some Euro Area countries receiving more from the government than what they send in taxes. This would improve the current account balance of those countries, keeping imbalances in check. A central government would both be able to take independent action and keep imbalances in check.

Marc Lavoie has a new paperMMT, Sovereign Currencies And The Eurozone. It’s based on a lecture he was asked to give in 2021 STOREP conference. In this he analyses what neochartalism (“MMT”) is and what is says about the Euro Area.

Marc Lavoie also discusses Sergio Cesaratto’s work. Sergio had an excellent bookHeterodox Challenges In Economics: Theoretical Issues And The Crisis Of The Eurozone and I somehow missed Marc’s review of it earlier.

My view on these issues—with good grasp of the institutional details—is that countries face a balance-of-payments constraint and the way the Euro Area is set up makes the balance-of-payments constraint stronger. Euro Area countries can no longer devalue their currencies (or hope their currencies depreciate by market forces) and the government can’t make overdrafts on their central banks.

It’s true that the European Central Bank (ECB) can buy government bonds but that it can doesn’t mean it actually will do to the extent needed. Indeed, the ECB has also pushed for tightening of fiscal policy using its powers. Countries face a BOP problem because like in other institutional setups, they’re at the mercy of foreigners. In fact more it’s more than otherwise in case of the Euro Area. And international indebtedness ultimately falls on the shoulders of the governments and hence we saw crisis in the government bond markets.

Countries with a strong international investment position such as Germany do not face this problem.

Ultimately, the problem is that the Euro Area doesn’t have a central government which would be involved in large fiscal transfers and keeping imbalances between countries in check. But as Sergio Cesaratto argues, it was never meant to be that way as the founders of the Euro Area designed it in a way to take away powers from national governments.

I should add one question which arises: the question about the political role of the ECB, which is similar to the role of governments in other places such as the US. There seems to be an inconsistency in the position of people such as Sergio (and I) that we treat the ECB and the US government differently. We say that the US government should be involved in more fiscal stimulus but don’t exactly say that the problems of the Euro Area can be resolved by proposing that the ECB promises to purchase government bonds without limits.

The answer to that is: even outside the Euro Area, rich countries’ central banks can bail out poor countries facing balance-of-payments financing problems. Does that mean that countries outside the Euro Area don’t face a bop-constraint??

It’s a rhetorical question posed as an answer.

Ultimately the balance-of-payments problems in the Euro Area is more severe than otherwise.

Where does neochartalism (“MMT” or “M.M.T.”) fit in my description? The idea that Euro Area governments cannot make overdrafts at their national central banks (NCBs) is something stressed by neochartalists is right but many authors who didn’t call themselves MMTers stressed this such as Wynne Godley in 1992. The idea that current account deficits don’t matter isn’t useful as you still have to explain why Germany didn’t go into a crisis like Greece.

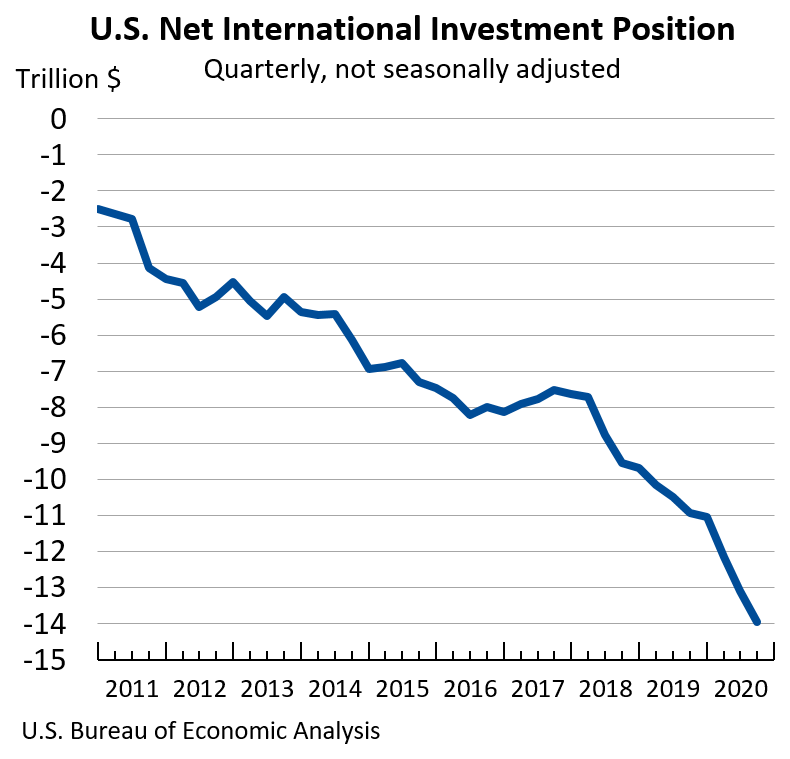

Although the release is more than a month old, I missed the release. The US international investment position is worsening and in unsustainable territory.

Chart from the BEA release dated 29 December, 2020, with last data point from Q3, 2020:

It’s not plotted relative to gdp, but work that out in your head 😉

Wynne Godley’s analysis before 2008 was simple: the US private sector balance—the difference between private expenditure and private income—was negative continuously and was unsustainable. The reversal—private expenditure falling relative to private income—would lead to a large crisis. And meanwhile the US trade was also weak and a large fiscal stimulus would be needed but because of international trade, the fiscal multiplier won’t be large enough and the recovery would be weak. His papers also forecast rising negative net international position mirrored by large rise in public debt relative to gdp, so to keep a sustainable configuration, the US government should directly address international trade, or else face slow growth.

… financial balances (relative to income flows) must stay within certain limits if debts are not to grow excessively, implying that the monitoring of these balances may yield a warning that unsustainable processes are at work.

Also, the “investment income” in balance of payments—the flows—stays positive. A lots has been written on it but on the question of sustainability it’s not too important in my view, although of course, once it turns negative it accelerates the already unsustainable position.

In the last post, I linked to John J. Mearsheimer’s paper Bound To Fail: The Rise And Fall Of The Liberal International Order. The paper was more from a political perspective than from a perspective of political economy, although it did go into the economics of it.

There’s a Post-Keynesian paper by Thomas Palley published last year, I thought I should recommend reading, since it goes into the political economy aspect of it. Also it is rooted more in the heterodox Keynesian perspective, unlike Mearsheimer who although criticises the US establishment, seems to want to propose an order which benefits the United States the most, not a new economic order which benefits the whole world.

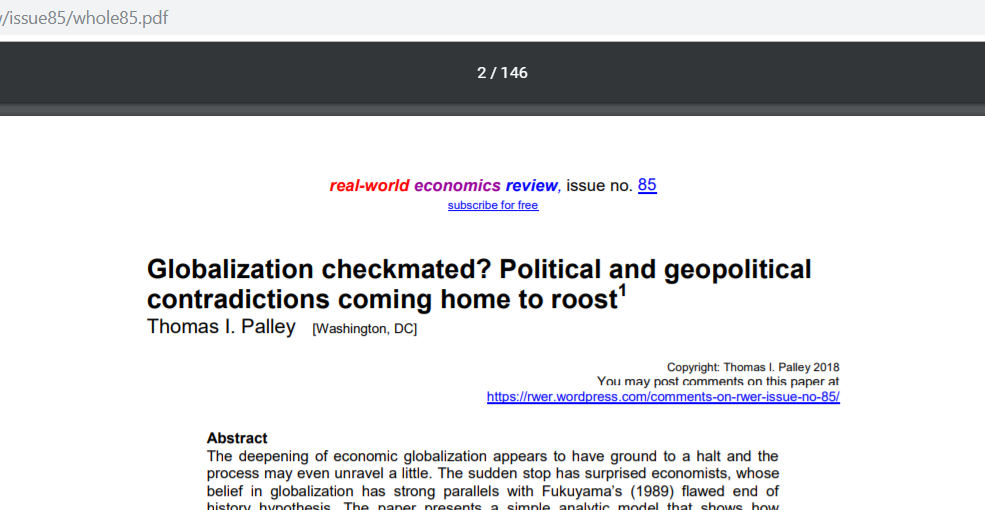

The liberal international economic order benefited the United States, or at least the “top 1” but because of countries gaming the system, started to backfire. The US has large current account deficits as a consequence of which its negative net international investment position grew larger and larger as this BEA chart indicates:

The solution is to dismantle the liberal international economic order in favour of new rules of the game which benefit everyone, not just oligarchs.

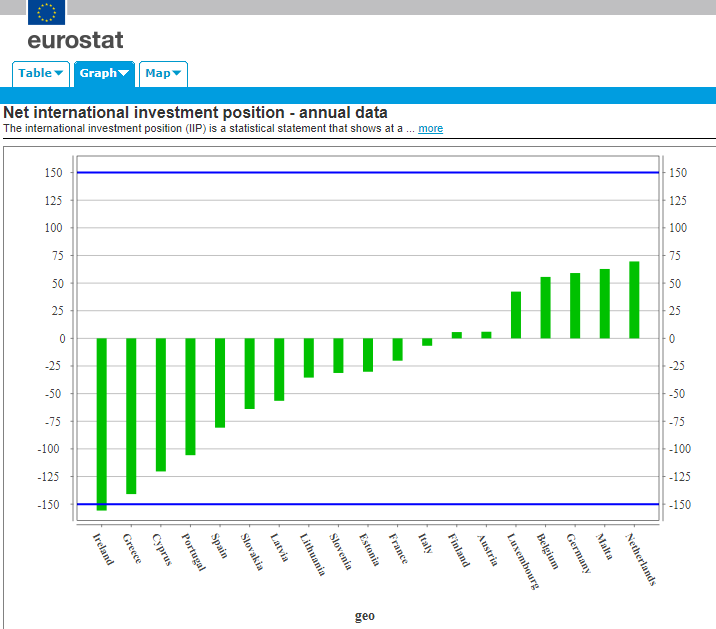

With crisis in Italy, the Euro Area is back in news! But it is not just Italy, the crisis is far from over, as this chart from Eurostat—my favourite—illustrates:

EA19, Net International Investment Position

The Euro Area doesn’t have a central government with large fiscal powers and hence there is nothing to keep imbalances in check. So some countries—with no fault of theirs—accumulated large debts. The net international investment position captures the financial position of a country. If it is positive, it is a creditor to the world, if it is negative it is a debtor of the world. If NIIP/GDP is large negative, then there is a problem. It’s difficult to say how large it can go, since it depends on how long markets and official institutions allow it to go. The need to keep it sustainable puts a downward pressure on GDP.

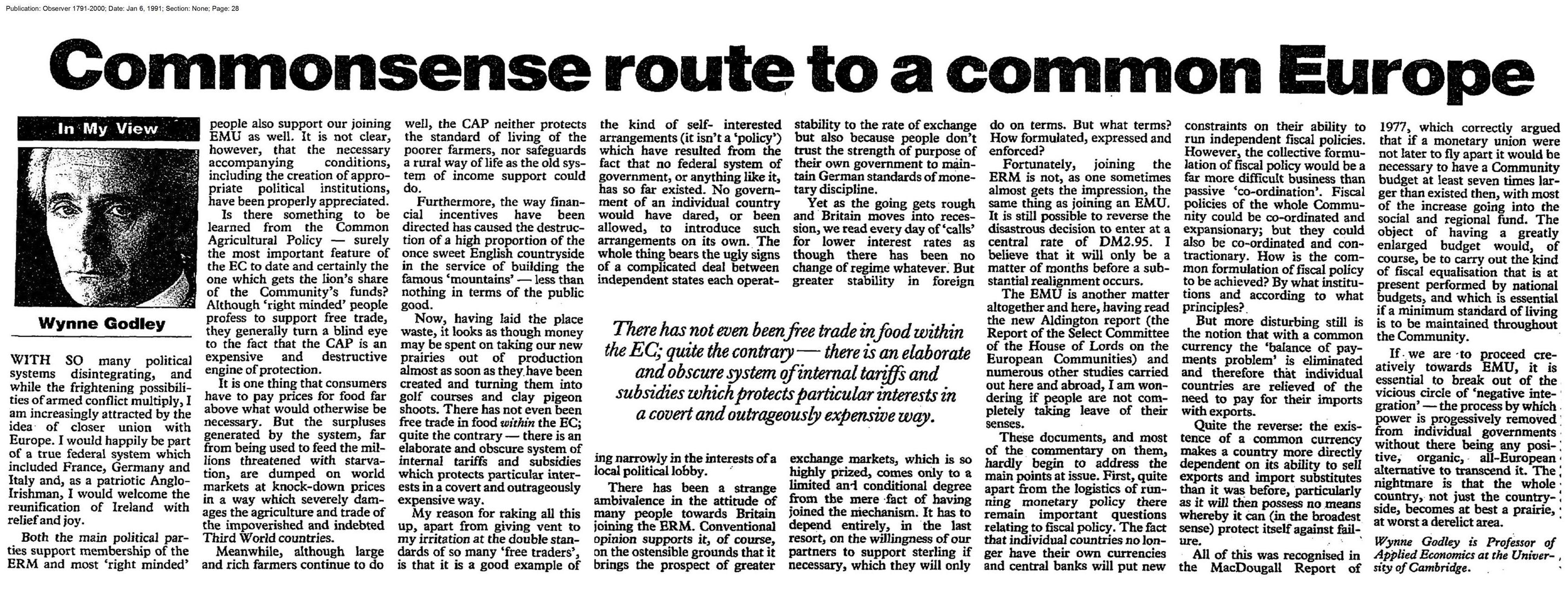

As Nicholas Kaldor wrote in The Dynamic Effects Of The Common Market,in the New Statesman, 12 March 1971:

… the objective of a full monetary and economic union is unattainable without a political union; and the latter pre-supposes fiscal integration, and not just fiscal harmonisation. It requires the creation of a Community Government and Parliament which takes over the responsibility for at least the major part of the expenditure now provided by national governments and finances it by taxes raised at uniform rates throughout the Community. With an integrated system of this kind, the prosperous areas automatically subside the poorer areas; and the areas whose exports are declining obtain automatic relief by paying in less, and receiving more, from the central Exchequer. The cumulative tendencies to progress and decline are thus held in check by a “built-in” fiscal stabiliser which makes the “surplus” areas provide automatic fiscal aid to the “deficit” areas.

… But more disturbing still is the notion that with a common currency the ‘balance or payments problem’ is eliminated and therefore that individual countries are relieved of the need to pay for their imports with exports.

Quite the reverse: the existence or a common currency makes a country more directly dependent on its ability to sell exports and import substitutes than it was before, particularly as it will then possess no means whereby it can (in the broadest sense) protect itself against failure.

– Wynne Godley, Commonsense Route To A Common Europe, inThe Observer, 6 January 1991.

Greece had large negative current account balance of payments and Germany had the opposite over the lifetime of the Euro.

Yet, there are some economists who argue that the Euro Area crisis is not a balance of payment crisis. Of course there are other aspects to the crisis as well but this in my view is the main issue. There was a debate between Sergio Cesaratto and Marc Lavoie on this. Now there is a new paper in the most recent issue of ROKE (Review of Keynesian Economics) by Eladio Febrero, Jorge Uxó and Fernando Bermejo which discusses this. The Wayback Machine/Internet Archive link is here if you are reading it after the journal puts the paywall again.

The authors seem to be against Sergio Cesaratto view. Since I agree with Cesaratto, I thought I should comment on it.

The fundamental problem of the Euro Area is that it doesn’t have a central government. If there had been a central government like the US federal government, with large fiscal powers, the Euro Area crisis would have been far less deeper. This is because weaker regions would have been recipients of “fiscal transfers”, i.e., receive more government expenditure than what they send in taxes.

Fiscal transfers can be seen transactions in the balance of payments of Euro Area countries if the EA had a central government. The way to do balance of payments for monetary and political unions is explained in the IMF Balance of Payments and International Investment Position manual. Take a country like Greece. The Euro Area government would be considered external to Greece. Same for other countries. But for the Euro Area as a whole, the central government would be considered inside the Euro Area.

So government expenditure would appear in Greek exports in the goods and services account and transfers in the secondary income account. Taxes would appear only in the latter.

So there is an improvement in the current account balance of payments for regions compared to the case when there is no central government. Current account balances accumulate to the net international investment of the whole country. A country which has persistent imbalances would have negative net international investment position, i.e., indebtedness to other countries.

So fiscal transfers keep all this in check by improving the current account balance. So if the Euro Area had a central government, debts of a country like Greece would be in check.

By joining the half-baked half-way house, Greece got an overvalued exchange rate and easier access for other Euro Area countries into its markets and its external imbalances worsened in its lifetime inside the monetary union.

Nations with high current account deficits will also have higher public debt than otherwise and would need international investors to buy the debt which residents won’t. Normally the price would adjust to bring international investors but as we have seen, sometimes there is no price and a fall in bond prices might lead to expectations of further fall leading external investors to dump the bonds instead of finding them attractive.

The trouble with Febrero et al. is that they seem to think that the European central bank can purchase all government debt of nation. Certainly, the European Central Bank (ECB) has stepped in at various times to ease the pressure on government bond markets. But the trouble with this is that there are under some conditions such as assuming it can impose tight fiscal policy on the governments it is helping.

If the Euro Area treaty is modified to allow countries to have independent fiscal policies, then for stability, the ECB has to buy bonds without limits and can keep accumulating. It is a political mess. A country like Germany could argue that it is writing an open cheque to Greece.

A political union wouldn’t have such problems. National level governments such as the Greek government would have fiscal rules on them, and hopefully not the supranational government. This is like the United States where state governments have rules on their budgets.

In contrast, if the ECB guarantees Greece’s debt, it has to impose some rules and since Greece is not recipient of any equalisation payments—the fiscal transfers—its performance is still dependent on its competitiveness. This is because competitiveness would affect the Greece government’s fiscal balance and hence put a deflationary pressure on Greece’s fiscal stance.

On the other hand, a Euro Area with a central government would imply Greece is recipient of substantial equalisation payments and its competitiveness isn’t so binding.

An argument of the economists arguing that the European monetary system has this thing called TARGET2 and that the intra-Eurosystem balances (i.e., automatic credits offered by one national central bank to another) can rise without limit is used in this paper. This is highly misleading. It is true but one should look at the changes in debits and credits elsewhere. Suppose a country like Greece sees a large private financial outflow. While T2 can absorb a lot of this—much more than anyone imagined—in the late stages, Greece banks become heavily indebted to their national central bank, The Bank of Greece. When they run out of collateral, the rules under ELA, Emergency Liquidity Assistance, is triggered. So TARGET2 or more accurately the Eurosystem cannot absorb everything.

In summary, the Euro Area cannot do without a central government in the long run. Anyone who thinks that the ECB or the Eurosystem can buy whatever residual debt private investors doesn’t understand that in such a system, Euro Area governments are given an open cheque.

The difference between not having a central government and a central government is that in the former, there is no equivalent income flow as in the latter. The Eurosystem purchases would affect the financial account of balance of payments, not the current account.

One of the noticeable assertions of the paper is:

With T2, there is just one currency. This means that if foreign exchange markets did not exist, there could not be a BoP crisis, so that the cause of the crisis should be found elsewhere.

The trouble with this is that it sees it only as a currency crisis. But the fact is that countries whose external position were weak were the ones running into trouble in the Euro Area. Had current account deficits not blown up, countries would have had better fiscal balance since the current account balance and the budget balance are related by an identity and even behaviourally as can be seen in stock-flow consistent models. In crisis times, foreign investors are more likely to shift their funds in their home countries. With better balance of payments, public debt would be held more internally and there would have been less pressure on government bonds.

There are comments in the paper about too much credit etc. This is true, but then the Euro Area crisis would have looked more like the economic and financial crisis affected the United States.

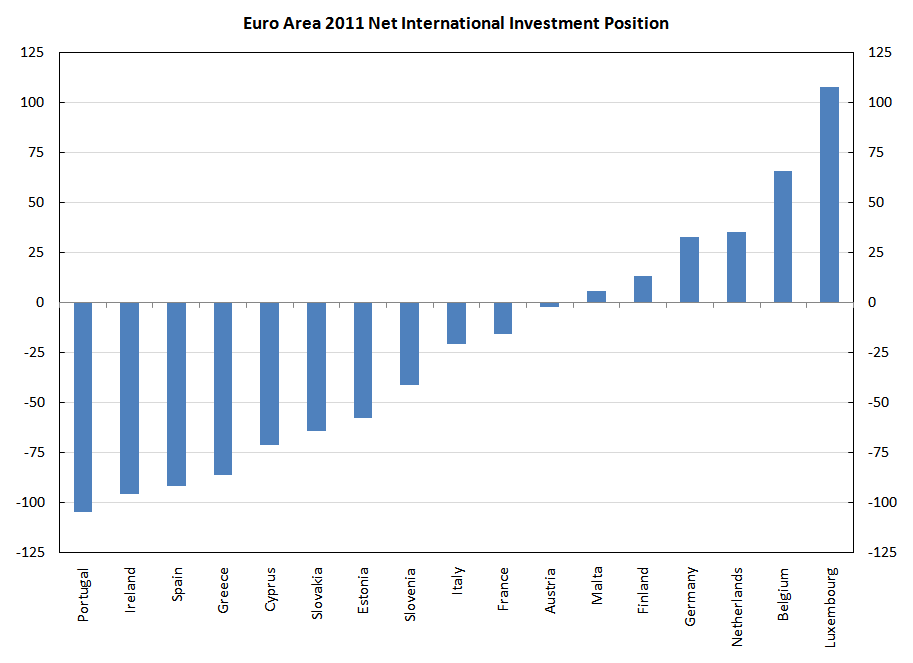

Here’s the the NIIP of Euro Area countries in 2011.

Doesn’t this explain why Germany was in a better position than Greece when the crisis started heating up? Or that Netherlands was in a better position than Portugal?

The recent cover story of The Economist on Germany’s trade surpluses—titled The German Problem: Why Germany’s Current-Account Surplus Is Bad For The World Economy— is the biggest concession the magazine has made to Keynesianism. Of course, it’s not as if the publication is now a full Keynesian but still, it’s a large admission.

So it was expected that The Economist‘s story was going to be opposed by other publications pandering to the establishment. For example, FT‘s Martin Sandbu who wrote a piece, Germany Bashing Falls Flat.

That means the accusation against Germany comes about five years too late. There was indeed a strong jump in the nation’s trade surplus half a decade ago, at a time when the world was still struggling to come out of recession. But that surplus has not changed much since.

He also says:

[the] claim [that Germany’s penchant for high saving … is a drag on global growth] trips up both analytically and contextually. Analytically, because the impulse from net trade on aggregate demand is the change in the external balance, rather than its level — much like the impulse from a fiscal deficit is the change in public borrowing as a share of economic output. So long as imports, exports and other macroeconomic aggregates grow at the same rate, a stable external balance goes along with the same steady growth of aggregate demand.

This claim has a pretense to be analytical but it’s hardly the case. This can be seen in stock-flow consistent models but it’s not the easiest to show that in a blog post, so here’s an attempt:

Divide the world into Germany (and other surplus countries) and the rest of the world. The rest of the world’s current account deficit means (without minor qualifications about “revaluations”) that its net international investment position is deteriorating by the amount of its current account deficit. So it’s not the case that if some aggregates grow at some rate, everything is fine because others—such as NIIP/GDP—aren’t.

There are many debt sustainability conditions and each should be used with care. One condition is that

cad(g) < g

where the lowercase cad is the ratio CAD/GDP, CAD is the current account deficit and g is the growth rate of GDP. It’s not as simple as it looks, because growth rate of GDP also affects the current account balance or deficit. The notation cad(g) is to indicate that it is so.

For high growth rates, cad(g) is larger than g.

In other words, sustainability implies that growth is restricted to be low.

Similarly, on the creditor’s side, an economy (i.e., Germany) growing at about 2.2% (nominal) and current account balance of 8.3%, that implies that its NIIP/GDP is rising fast (and hence deteriorating the ratio of others).

So Sandbu’s claim that those asking Germany to expand domestic demand aren’t analytical itself falls flat. His analysis just does a chart eyeballing of some numbers. Just because a few things aren’t worsening, doesn’t mean things are fine. Other metrics may be worsening.

Handelsblatt‘s analysis doesn’t really say much except claiming that Germany’s trade surplus just means its expenditure is less than its income and nothing more. It also errs on endorsing the claim that, “that national economies cannot be managed like large firms.”, which the crisis taught us is highly incorrect.

This is a continuation of a recent post at this blog, Public Debt And Current Account Deficits, in which I argued that the current account balance of payments affects the public debt.

A usual objection to the connection is that the two deficits—current account deficit and the budget deficit—although connected by an identity, don’t move together and in fact move in the opposite direction frequently. This point was raised by the blog Econbrower, yesterday.

The identity in question is:

NL = DEF + CAB

where, NL is the private sector net lending, DEF is the government’s deficit and CAB is the current account balance of payments (and is to a zeroth order approximation, exports less imports).

This is not a behavioural hypothesis but still a useful tool to build a narrative. Also, the causality connecting the identities is domestic demand and output at home and abroad.

Imagine, initially that NL is a small positive relative to GDP (for example, NL/GDP = 2%), Also remember that,

NL = Private Income − Private Expenditure

Now assume that private expenditure rises relative to private income. This will lead to higher GDP, a higher national income and a rise in imports because of income effects and hence a lower CAB. It will also lead to higher taxes because of higher income and hence will reduce the budget deficit, DEF, ceteris paribus.

So if the current account balance is in deficit, it would mean that the budget deficit and the current account deficit move in opposite directions.

That’s the theoretical basis for the empirical relationship. But that in itself isn’t the whole story. This is because the other balance—net lending, NL—has a life of its own. As is the case in the United States and several western countries, it turned negative once or twice in the 1990s the 2000s, and when the private sector’s debt rose, it made a sharp U-turn into the positive territory. The blue line in this graph:

Click the graph to see it on FRED.

So, if net lending reverts to its mean of staying positive, one can then conclude that the cumulative budget deficit, or the public debt is affected by cumulative current account deficits.

At any rate, the public debt shouldn’t be the main object of study. What’s more important is the international investment position. And it’s an identity that:

NIIP = cumulative CAB + Revaluations

where, NIIP, is the net international investment position.

A nation which runs current account deficits can become indebted to the rest of the world. IIP is the position of assets and liabilities of resident sectors of a nation. So, the net debt (the negative of NIIP) is the nation’s debt.

The above linked Econbrowser post brings in the complication of revaluations to deny the relationship between CAB and NIIP. But revaluations can’t save you for long.

In short, both public debt and NIIP depend on current account deficits.

Finally a weak analogy: if you play in the rain, you might enjoy it as well. But then if you get sick, you can’t say, “I felt so good playing in rains, so playing in the rain didn’t make me sick”. Saying the two deficits (current account and budget) move in opposite directions is an argument like that.

{kind=link}